Most financial advice about building an emergency fund living paycheck to paycheck starts with the same useless line: save three to six months of expenses. If you are reading this, that advice has never once helped you. Not because you are doing something wrong. Because your money is already gone before the month ends. You cannot save what you do not have left over. So this is not that article. This one starts with ten dollars.

Why the Standard Emergency Fund Advice Fails People Living Paycheck to Paycheck

The three-to-six-month rule comes from a world where money is left over after the bills are paid. A lot of personal finance is built for that world. This is not.

When you are stretched thin, the standard advice fails in two specific ways. The target number is so large it feels like a joke, so nothing gets started. And even when something does get started, the next emergency wipes it out before it gets anywhere, and the whole thing feels pointless.

Neither of those things means the goal is wrong. The starting point has to be different. The target has to be different. And what you understand this money to be for has to be different.

Why Having No Savings Makes Everything Cost More

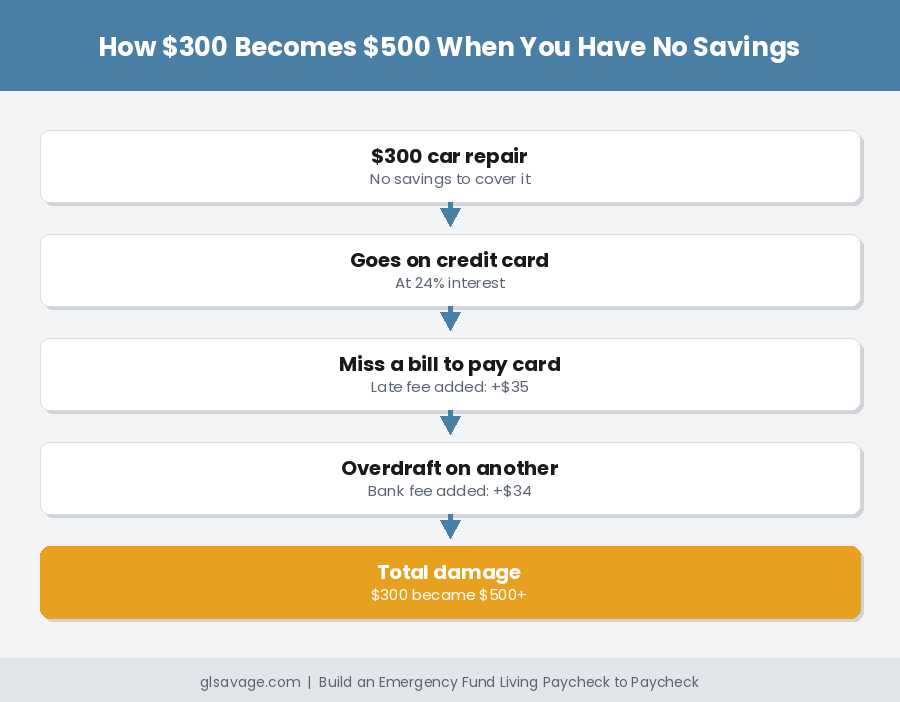

Being short on cash does not just mean you have less money. It means every small problem costs more than it would cost someone with a cushion. A $20 shortfall triggers the same overdraft fee as a $200 shortfall. A bill paid one day late costs the same late fee as one paid two weeks late. A car repair you cannot cover in cash gets put on a payment plan at whatever rate they put in front of you, and those rates can reach triple digits. If you want to see exactly how that trap works, The Real Cost of an Unreliable Car And How to Escape it lays it out in full.

The result is a chain reaction most people recognize immediately. One unexpected cost triggers a late payment. The late payment triggers a fee. The fee creates another shortfall. The shortfall triggers another overdraft. By the time it stops, a $300 problem has cost $600. That is not bad luck and it is not bad money management. It is the predictable math of having nothing between you and the next hit. The Poverty Premium Explained: How to Fight Back names the full system behind why this keeps happening to the same people.

An emergency fund interrupts that chain. Even a small one. Even $100. The goal is not comfort or security in any big sense. The goal is to stop being the person the penalty machine hits first.

Getting Off Zero: The Only Goal That Matters Right Now for an Emergency Fund

Zero is where the chain reaction starts. Zero is where a $40 timing problem becomes a $75 problem. Getting off zero is the entire first job, and the amount matters less than the fact of it.

Ten dollars is stronger than zero. Twenty-five dollars is stronger than zero. Fifty dollars prevents one overdraft. One hundred dollars covers a copay or a utility bill that came in higher than expected. None of those numbers sound like financial security. That is fine. Financial security is not the goal today. Stopping the bleeding is.

If $50 feels impossible right now, that is real information, not a personal failing. Start with $10. Start with $5. The amount is almost beside the point at first. The habit and the separation are what matter.

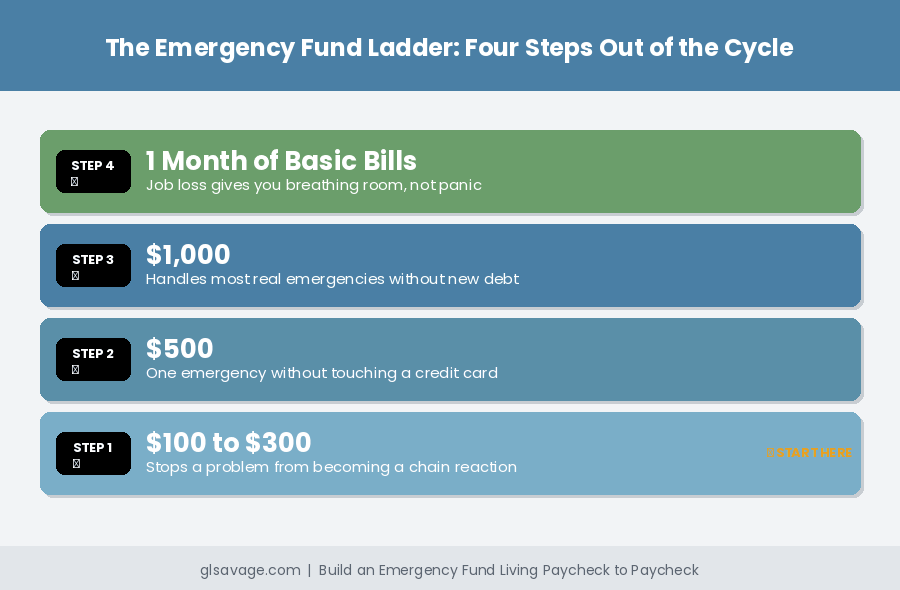

The Emergency Fund Ladder

Once you are off zero, build upward one step at a time. Do not think about the top. Think about the next step. Each one changes your situation in a specific, concrete way.

Step one: $100 to $300. This covers one overdraft, one copay, one utility bill that came in high. It is the difference between a problem and a chain reaction. Most people who get to $300 and hold it notice immediately that certain months feel different. Smaller problems stop turning into bigger ones.

Step two: $500. This covers most towing bills, most minor car repairs, most urgent care visits. At $500 you can handle one real emergency without touching a credit card. This is the first number that starts to feel like something.

Step three: $1,000. This is the number the financial world should have been telling people to start with instead of three months. A thousand dollars handles the majority of real emergencies most people run into in a given year. It does not make life easy. But it absorbs the hit without creating new debt most of the time.

Step four: One month of basic bills. Rent, utilities, food, transportation. Just one month. This is the point where a job loss or a cut in hours gives you actual breathing room instead of immediate panic. Most people reading this will not reach step four for a while. That is fine. The steps below it are not consolation prizes. They are real protection.

How Long It Actually Takes to Build an Emergency Fund Living Paycheck to Paycheck

Most people underestimate how fast small consistent amounts add up, and overestimate how much they need to save per paycheck to get somewhere real. Here is the actual math, based on saving the same amount every two weeks automatically without touching it.

| Saved per paycheck | Reach $300 | Reach $500 | Reach $1,000 |

|---|---|---|---|

| $5 | 30 months | 50 months | 100 months |

| $10 | 15 months | 25 months | 50 months |

| $20 | 8 months | 13 months | 25 months |

| $25 | 6 months | 10 months | 20 months |

| $50 | 3 months | 5 months | 10 months |

That table shows the floor. Regular paychecks only, no extras. One tax refund, one sold item, one overtime check on top of any of those amounts changes every timeline on it. The point is not that $5 per paycheck gets you there slowly. The point is that $20 per paycheck, which most people can find when they look honestly at one subscription or one spending habit, gets a person living paycheck to paycheck to $1,000 in two years from paychecks alone, faster with anything else added.

How to Save When There Is No Money Left: Real Strategies for Building an Emergency Fund

Waiting for extra money to appear means waiting forever. The approach has to work inside the actual month, not the ideal month.

Move money automatically on payday. Set up an automatic transfer from your regular bank account to a separate savings account on the same day your paycheck hits. Five dollars. Ten dollars. Whatever does not break your budget. The automation is the whole trick. The moment saving becomes a decision you make while exhausted after the bills are paid, it loses to the bills every time. Take the decision out of it entirely.

Use windfalls on purpose. A tax refund, an overtime check, a sold item, a birthday gift from a relative. These moments are the fastest way to the next step and most people spend them before they have a plan. The plan needs to exist before the money arrives. Decide in advance what dollar amount goes to savings the day any windfall hits. Even 30 percent of a $400 tax refund is $120, which gets you to step one in a single move.

Find one leak, not your whole budget. Trying to go through everything you spend is exhausting and usually falls apart after one hard week. Find one thing. A subscription you forgot about. Takeout that stacks up because you are too tired to cook. One thing, redirected automatically into savings, does more than a complete budget overhaul that collapses by week two.

Round-up programs. Some banks and apps round every purchase up to the nearest dollar and move the difference into savings without you doing anything. On a normal month of spending this adds $15 to $40 to your fund with zero effort after setup. It is not fast. But it runs in the background while everything else is happening, and it never requires a decision.

The Tax Refund Move Most People Miss When Building Emergency Savings

For people working on an emergency fund while living paycheck to paycheck, the tax refund is often the single largest chunk of money that shows up in a given year. Most of it is gone within two weeks. Not because people are reckless. Because there is a list of things that have been waiting for it. The car repair. The overdue bill. The thing the kids needed. That list is real. Those needs are real.

But here is the move. Before that refund arrives, pick a specific dollar amount that goes straight to savings the same day the deposit hits. Not what is left over after the list gets handled. A specific amount, moved first, before anything else touches it.

Even $200 out of a $1,200 refund changes your whole starting position for the year. You are at step one or step two before the month is over. The rest handles the list. Nothing is being taken away. The order is just different, and that order is everything.

If you want to make sure that money never has a chance to disappear into everyday spending, the IRS lets you split your refund into more than one account at tax time. You can send a set amount straight to savings without it ever landing in your regular account. That removes the temptation entirely because the money is never there to spend in the first place.

Where to Keep Your Emergency Fund

Keep it completely separate from the account you use every day. If it sits next to your regular spending money, it will get spent. Not because you have no self-control. Because when money is in one place, your brain cannot reliably tell the difference between money that is free to use and money being held for something else. Separation solves this without requiring willpower.

A basic savings account at a different bank works well. Moving money between banks takes about a day, which creates just enough of a pause to stop impulse spending while still being fast enough to use in a real emergency. That is the right balance for most people getting started.

Once you have $500 or more saved, look at a high-interest savings account. These pay more on the money sitting there than a regular savings account does. The difference is small when the balance is small. It gets more real at $500, $1,000, and above. The rules for getting your money out are basically the same. There is no real downside to switching once you have enough to make it worth the move.

Do not put this money in stocks, crypto, or anything that can go down in value. This is not money you are trying to grow. It is money you need to be there when something goes wrong. The week you need it most could easily be the week the market is down 20 percent. Keep it boring. Keep it somewhere you can get to it in a day. Keep it separate.

What Actually Counts as an Emergency When You Have an Emergency Fund

This is where most emergency funds quietly disappear. Not from one big bad decision. From a dozen small ones that each felt reasonable at the time.

Before you spend from the fund, ask two questions. Is this unexpected? If you knew it was coming, it was not an emergency. It was a planning gap, which is a different problem. And does this have a real, immediate consequence if it does not get paid right now? A shutoff notice on your power bill is an emergency. A sale on something you actually need is not.

Real emergencies: a car repair you need to keep your job, a medical bill that cannot be delayed, a utility about to be shut off, a rent shortfall from a lost shift or a job loss, a prescription you cannot skip.

Not emergencies: a sale, something you want, a planned purchase that came up sooner than expected, a bill where you can call and arrange a payment plan, anything that can wait 30 days without something actually bad happening.

The fund only does its job if it is still there when something real hits. Every time you protect it from a non-emergency, you are protecting yourself from the next actual crisis.

What to Do After You Use Your Emergency Fund

This is the part almost nobody writes about. It is also where most people get discouraged and stop.

You saved $400. Something real happened and you had to spend it. Now you are back at zero and it feels like it was pointless. Like saving is just not possible for people in your situation.

It was not pointless. That $400 did its job. It covered a hit that would have otherwise gone on a credit card at high interest, or caused a late payment, or cost you a paycheck. The fund worked exactly the way it was supposed to. Now you rebuild it.

Rebuilding is faster the second time because the hard part is already done. The separate account already exists. The automatic transfer is already set up. You know the steps because you have been through them. You are not starting over. You are refilling something that already works.

Restart the automatic transfer immediately, even if you drop the amount for a while. If you were saving $20 per paycheck and the emergency cleared it out, drop to $10 if you need to, but turn the transfer back on the same week. Do not wait until the money feels more comfortable. It almost never feels more comfortable on its own. The transfer is what creates the cushion, and the cushion is what eventually makes things feel more manageable.

If the thing that drained the fund is a category that keeps coming up, car repairs, medical costs, school expenses, think about whether a second savings account for that specific category makes sense once the emergency fund is back up. Some people do better keeping true unexpected emergencies separate from expenses that are irregular but not really a surprise. That separation keeps the emergency fund from being slowly used up by things that could have been planned for.

How an Emergency Fund Helps Your Credit Score Over Time

When you have no savings, any unexpected cost either goes on a credit card or causes a missed payment somewhere. Both of those things hurt your credit score. Putting more on a credit card raises how much of your available credit you are using at any given time, and that is one of the biggest pieces of how your score is calculated. A missed payment goes on your record and stays there for years.

When you have a cushion and can cover an unexpected cost without adding to your card balance and without missing a bill, your record stays clean. Over 12 to 18 months of that, scores go up. And a better score means every future loan, car payment, or apartment application gets cheaper or easier. The emergency fund is not just about emergencies. It is about what the absence of emergencies does to the rest of your financial life over time. That is exactly why building an emergency fund while living paycheck to paycheck is not just about having a backup plan. It is about changing what everything else costs you going forward.

If you want to understand how your score controls what everything costs you, Why Your Credit Score Exists and Who It Actually Serves covers it in full. And if you are carrying credit card debt while trying to build this fund, Minimum Payments Keep You in Debt. That Is Not an Accident. explains exactly why the minimum payment is designed to keep you paying forever.

When Payday Loans Are Filling the Gap Your Emergency Fund Should Fill

If you have been using payday loans or cash advances to cover gaps between paychecks, this is for you specifically.

Those products exist because the savings account does not. They are expensive because people who have no cushion and nowhere else to go have no leverage to demand better terms. The yearly interest rate on a typical payday loan is over 300 percent. A $300 loan costs $345 two weeks later. If you cannot cover the $345, the cycle starts again. How Payday Loans Are Legal and What to Do Instead explains exactly how that system works and what the real alternatives are.

The emergency fund is the way out of that cycle. Not this week, not next month, but over 12 to 18 months of building one step at a time, the gaps that payday loans currently fill start getting covered by your own savings instead. The savings account costs you nothing. The payday loan costs you hundreds of dollars a year. Both are solving the same problem. Only one of them gets you out.

Building an Emergency Fund When You Have Debt Collectors, Bad Credit, or No Bank Account

None of those things stops you from saving. But each one creates a different problem worth sorting out.

If you have no bank account, a prepaid debit card that has a savings option works as a starting point. Some credit unions also offer basic accounts for people who have been turned down by regular banks. The goal is to keep your savings money somewhere physically separate from what you spend day to day. You do not need a traditional bank to do that.

If debt collectors are coming after you and there is a risk they could take money from your account, that is a real threat to anything you manage to save. How Collection Accounts Affect Your Credit Report explains what they can and cannot actually do, and what your options are. Protecting your money and understanding what collectors are legally allowed to do belong in the same conversation.

If you have bad credit or no credit history, the savings and the credit rebuild happen at the same time, not one after the other. You do not need to fix your credit before you start saving, and you do not need to finish saving before you start working on your credit. A secured credit card used lightly and paid off every single month builds your credit history while the savings account builds your cushion. Both move forward at the same time.

The Real Reason It Feels Impossible to Save

Most people who cannot seem to build an emergency fund are not failing because they lack discipline. They are failing because every time they get close to a number that feels meaningful, something takes it back. That happens enough times and it starts to feel like proof that saving is just not something that works for people in their situation.

It is not proof of that. It is proof that the cushion was not yet large enough to absorb the hit. The answer is not to stop trying. The answer is to get further before the next hit comes.

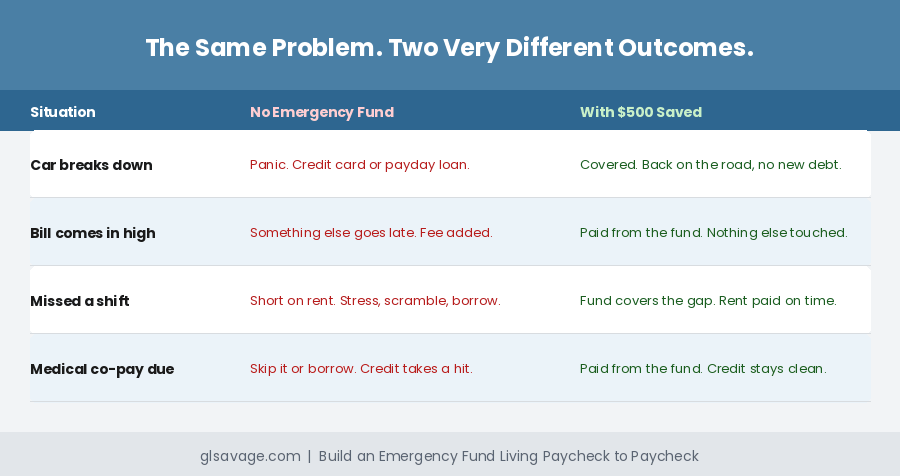

You save $200. You are starting to feel like something is changing. Then the car needs a repair and it is gone. Back at zero. It feels like confirmation that this does not work for you. But here is what actually happened: you covered a $200 problem without going into debt. The fund worked. The problem is that $200 was not yet enough to survive the hit and keep some left over. That is a target problem, not a you problem. Get to $300. Then $500. The hits do not stop. But at some point the cushion is large enough to take the hit and still have something left. That is when things start to feel different.

The other thing that kills motivation is staring at the full target while you have almost nothing saved. Three to six months of expenses looks impossible when you have $47. Stop looking at the full target. The only number that matters right now is the next step. What does it take to get from where you are to $100? From $100 to $300? One step at a time, all the way up. That is how an emergency fund living paycheck to paycheck actually gets built. Not in one move. One step at a time until the steps are behind you.

Bottom Line: Building an Emergency Fund Living Paycheck to Paycheck Starts with One Step

The three-to-six-month number is real and it matters eventually. But it is not where you start. You start by getting off zero. You start by automating $5 or $10 or $20 into a separate account on payday. You start by knowing that $100 is not nothing. It is the difference between a problem and a chain reaction.

Build the ladder one step at a time. Protect the fund from things that are not real emergencies. Rebuild it immediately after you use it, even at a smaller amount. Use every windfall with a plan before the list takes all of it.

The penalty machine runs on the absence of any cushion between a problem and its consequences. Every dollar in that account is a dollar it does not get.

Frequently Asked Questions

Start smaller than any advice column will tell you. Five dollars per paycheck, moved automatically on payday into a separate account. The amount matters less than doing it automatically every time. Even $25 can prevent one overdraft fee. Getting off zero is the only goal at first. The amount grows from there.

The realistic first target is $100 to $300, not three to six months. That amount covers one small emergency without triggering a chain reaction of fees. From there the next target is $500, then $1,000, then eventually one month of basic bills. Each step changes your situation in a real way. You do not need to see the top to take the first step.

In a separate account at a different bank than the one you use every day. The extra step of moving money between banks creates just enough of a pause to stop impulse spending while still being fast enough to use in a real emergency. Once you have $500 or more saved, a high-interest savings account pays more on the money sitting there with essentially the same ease of access.

Build a small emergency fund first, then work on the debt. Without any cushion, every unexpected expense goes right back onto the credit card and undoes whatever you paid down. A $500 to $1,000 emergency fund keeps new debt from being added while you pay off the old debt. The two goals are not fighting each other. They are just ordered.

Something unexpected, necessary, and with a real immediate consequence if it does not get handled right now. A car repair you need to get to work. A medical bill that cannot be put off. A utility about to be shut off. A rent shortfall from a lost job or cut hours. What does not count: a sale, something you want, a planned purchase that showed up sooner than expected, or anything that can wait 30 days without something actually bad happening.

Restart the automatic transfer immediately, even at a lower amount. The account is already there. The transfer is already set up. You are refilling something that works, not building from scratch. Drop the transfer amount if you need to, but turn it back on the same week. Do not wait for things to feel easier. The transfer is what makes them easier over time.

Yes. Bad credit does not prevent you from saving. The savings and the credit rebuild happen at the same time, not one after the other. A savings account does not require good credit to open. Start putting money away while you also work on the credit side through other means, like a secured credit card paid off in full every month or a credit-building loan from a credit union.

The emergency fund is how you eventually stop needing them. Payday loans exist because there is nothing else to cover the gap. Over 12 to 18 months of building your savings one step at a time, those gaps start getting covered by your own money instead of a loan. The savings account costs you nothing. The payday loan costs you hundreds of dollars a year in fees and interest. Both solve the same problem in the short term. Only one of them gets you out.

Whatever does not break your budget, moved automatically on payday before anything else touches it. For some people that is $5. For others it is $25. The amount matters less than doing it every single time without making it a decision. A $10 automatic transfer every two weeks adds up to $260 in a year. That is step two on the ladder. It does not feel like much per paycheck. Over a year it is real money.