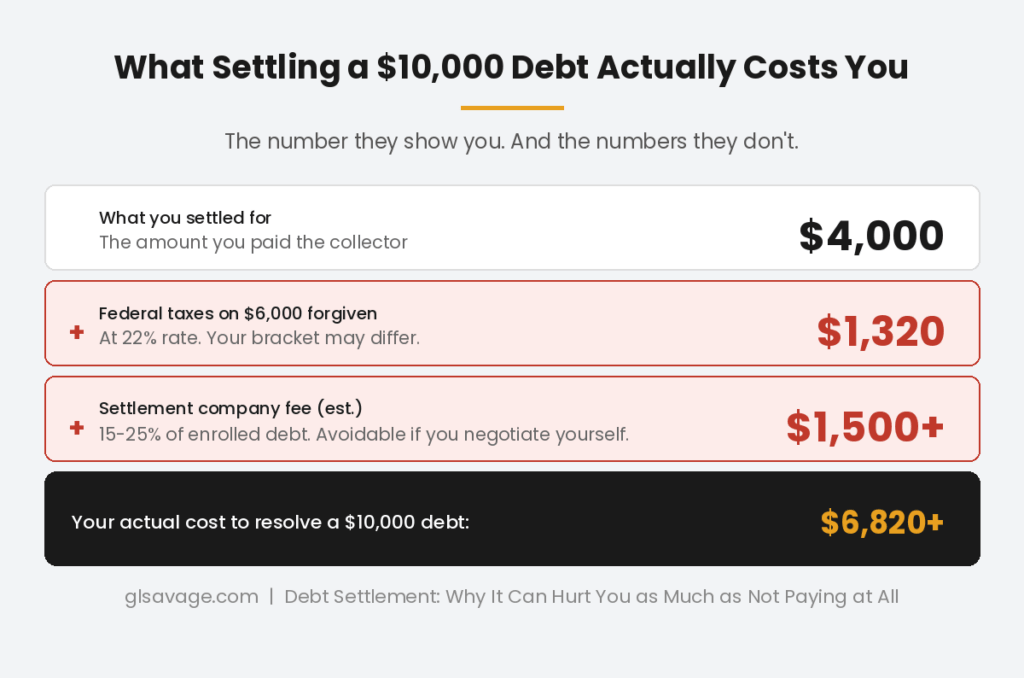

Debt settlement sounds like the best deal you never knew you could ask for. You owe $10,000. The collector agrees to take $4,000. You pay it, they mark it resolved, and you save $6,000. What is not to like? The answer is that the $6,000 you did not pay is now considered income by the IRS, and you will owe taxes on it. The credit damage from the missed payments required to reach settlement stays on your report for seven years. And if you used a debt settlement company to negotiate, you paid them fees out of the money you thought you were saving. Debt settlement is sometimes the right move. It is never the free win it is sold as.

What Debt Settlement Actually Is

Debt settlement is an agreement between you and a creditor where you pay less than the full amount owed and the creditor agrees to consider the debt resolved. It typically only happens on accounts that are already significantly delinquent. A creditor with a current account, receiving regular payments, has no reason to accept less than the full balance. Settlement is for accounts where the creditor has concluded that the full amount is unlikely to be recovered and something is better than nothing.

This is the first thing the industry glosses over. To settle a debt, you usually have to stop paying it first. Settlement companies routinely instruct clients to stop making payments and redirect that money into a dedicated account. The idea is that once the account is sufficiently delinquent, the creditor will be more motivated to accept a reduced lump sum. That logic is not wrong. The problem is what happens to your credit in the meantime.

The Damage Starts Before the Settlement Does

Every month you do not pay a debt, your credit report records a missed payment. One missed payment can drop a credit score significantly. Six to twelve months of missed payments, which is often how long it takes to accumulate enough in a settlement account to make an offer, creates a trail of delinquencies that stays on your credit report for seven years from the date of the first missed payment.

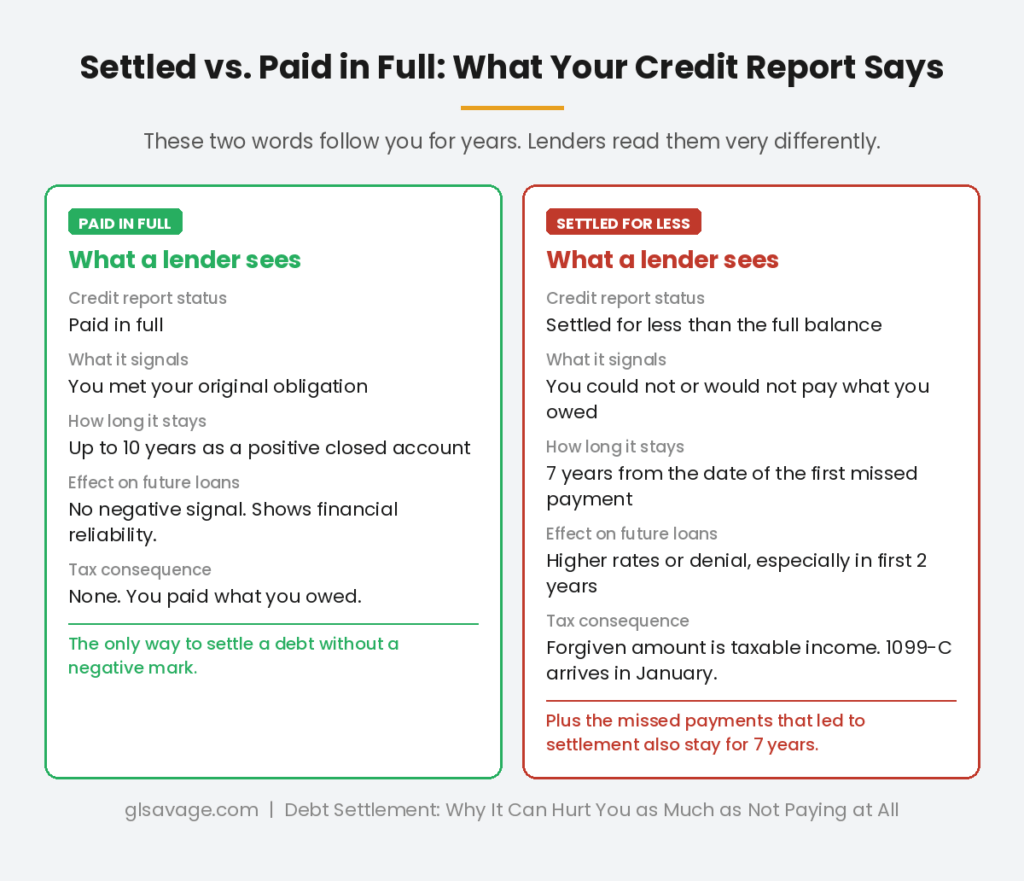

By the time the settlement is reached and the account is marked resolved, the credit damage is already done. The settlement notation itself, “settled for less than the full balance,” adds another negative mark on top of the missed payments. Both stay on your report. Lenders reviewing your file do not see a clean resolution. They see months of missed payments followed by a creditor accepting less than they were owed. That tells them you could not or would not meet your original obligation, which is exactly the signal that makes future lenders charge higher rates or decline the application entirely.

Settlement is better for your credit than an account that sits unresolved and in collections forever. But the gap between settlement and “paid in full” is significant, and the gap between settlement and never missing a payment is enormous. If your credit is already severely damaged before settlement begins, the additional hit is smaller. If you still have reasonable credit and are considering settlement as a proactive strategy, you should understand that the process of reaching settlement will likely cause more damage than the settlement itself.

The Tax Bill Nobody Mentions Until January

The settlement feels finished when you pay the reduced amount. Then January arrives and a Form 1099-C shows up in your mailbox.

When a creditor forgives $600 or more of debt, they are required by law to report that amount to the IRS on a Form 1099-C, Cancellation of Debt. The IRS treats forgiven debt as ordinary income. In the example above, if you settled a $10,000 debt for $4,000, the $6,000 that was forgiven is taxable income in the year the settlement occurred. Your creditor reports it. The IRS already has the form. If you do not report it and pay the resulting taxes, you will hear about it.

This is money you never received. You did not earn $6,000. You simply stopped owing it. But the IRS views canceled debt as equivalent to receiving the money, because when you borrowed it you were not taxed on it, and now that you no longer have to pay it back, the original tax exclusion no longer applies. The tax on $6,000 of additional income depends on your bracket, but at a 22 percent federal rate that is $1,320 owed to the IRS on top of the $4,000 you already paid. Your total cost of resolving a $10,000 debt was not $4,000. It was $5,320, plus any state income tax, plus any fees paid to a settlement company.

There is an exception worth knowing. If you were insolvent at the time the debt was forgiven, meaning your total debts exceeded the fair market value of everything you owned, you may be able to exclude some or all of the forgiven amount from taxable income. Insolvency is a specific financial calculation, not a general sense of being broke. You would need to file IRS Form 982 and document your assets and liabilities at the moment of cancellation. If you qualify, the insolvency exclusion can significantly reduce or eliminate the tax on forgiven debt. A tax professional can walk through whether you qualify. But this requires planning and documentation, and most people sitting with a 1099-C in January had no idea the form was coming.

What Debt Settlement Companies Cost You

If you hire a for-profit debt settlement company to negotiate on your behalf, you are paying for a service that you could in most cases do yourself for free. And the fee structure is designed to ensure the company gets paid regardless of what you save.

Settlement companies typically charge between 15 and 25 percent of the enrolled debt or of the amount settled, depending on how the contract is written. On a $10,000 debt, that is $1,500 to $2,500 in fees on top of the settlement amount. The FTC’s Telemarketing Sales Rule prohibits settlement companies from collecting any fees until three conditions are met: at least one debt has been settled, there is a written agreement between the consumer and the creditor, and the consumer has made at least one payment on that settlement. But the fee still comes out of the money you were setting aside, reducing what you have available to offer creditors and extending the timeline.

During the period you are enrolled in a settlement program and not paying creditors, interest and fees continue to accrue on the accounts. Depending on how long the process takes, the balance you eventually settle may be significantly higher than when you enrolled. The settlement percentage might look impressive on paper while the actual dollar amount you owe has grown.

You do not need a settlement company to settle a debt. Creditors negotiate directly with consumers. The process is not complicated: you contact the creditor or collector, you explain your situation, and you make an offer. Many collectors have internal settlement programs and pre-approved offer thresholds. You can do this yourself, keep the fees, and achieve the same result.

When Settlement Makes Sense Anyway

None of this means settlement is never the right choice. For some people in some situations, it is the best available option. The point is to make that choice with full information rather than the version sold by companies who profit from your enrollment.

Settlement makes more sense when the account is already in collections, because the original creditor has already written off the debt and the collector paid pennies for it. Your missed payments are already on your report. The credit damage has already been done. In that situation, the additional negative mark from a settlement notation is marginal, the collector has significant room to negotiate, and the tax bill may be manageable or excluded under insolvency.

Settlement makes less sense when the account is still with the original creditor and in reasonable standing. In that case, reaching settlement requires manufacturing the delinquencies that make the creditor willing to negotiate. You are creating the damage in order to fix the problem. There are usually better alternatives, including negotiating a hardship payment plan directly with the creditor, working with a nonprofit credit counseling agency on a debt management plan, or in more extreme situations, exploring bankruptcy, which has its own consequences but discharges debt without a tax bill.

The debt payoff order matters as much as the method. Understanding which debts to address first and which pose the most risk to your financial stability is the foundation of any debt strategy. Minimum Payments Keep You in Debt. That Is Not an Accident. covers how the math on revolving debt is designed to keep balances alive, and How Collection Accounts Affect Your Credit Report explains what collection accounts actually do to your credit and for how long.

What to Do Before You Agree to Anything

If a collector is offering a settlement, or if you are considering initiating one, these are the things to work out before you agree.

Get the settlement agreement in writing before you pay anything. An oral agreement to settle for a reduced amount is not enforceable. The written agreement should specify the exact amount you are paying, that this payment satisfies the debt in full, and how the account will be reported to the credit bureaus. Do not pay until that document is in your hands.

Ask how the account will be reported. Some creditors will agree to report the account as “paid in full” rather than “settled for less than the full balance” as part of the negotiation. This is not guaranteed and not all creditors will agree, but it costs nothing to ask and the difference on your credit report is significant.

Calculate the tax bill before you finalize the offer. If you settle $8,000 of debt for $3,000, the $5,000 forgiven is likely taxable. Know your tax bracket and estimate what you will owe before you commit to an amount. Include that in your calculation of what the settlement actually costs.

Check whether you qualify for the insolvency exclusion. If your liabilities exceeded your assets at the time of settlement, you may be able to exclude some or all of the forgiven amount from taxable income. Talk to a tax professional before the settlement is finalized if this is in question.

If a collector contacts you about a debt before any of this, sending a debt validation request first forces them to confirm the debt is real, the amount is accurate, and they have the legal right to collect it. That baseline verification changes what you know going into any negotiation. For how that process works, read How Debt Validation Works and Why You Should Always Use It. Going in with open eyes is what separates debt settlement as a strategy from debt settlement as a trap.

Frequently Asked Questions

Does debt settlement hurt your credit?

Yes, in multiple ways. To settle most debts you need to stop paying first, creating months of missed payment entries on your credit report. The settlement itself is then reported as “settled for less than the full balance,” which is a separate negative mark. Both the missed payments and the settlement notation stay on your report for seven years from the date of the first missed payment. The total damage is typically greater than people expect when they agree to settle.

Do you pay taxes on settled debt?

Yes, in most cases. When a creditor forgives $600 or more of debt, they report the forgiven amount to the IRS on a Form 1099-C. The IRS treats that amount as ordinary taxable income in the year the debt was forgiven. You pay taxes on money you never received. There is an exception if you were insolvent at the time of settlement, meaning your total debts exceeded your total assets. If you qualify, you can exclude some or all of the forgiven debt from taxable income by filing IRS Form 982.

Can you settle a debt without a settlement company?

Yes. Settlement companies negotiate on your behalf, but creditors and collectors negotiate directly with consumers. You can contact the collector yourself, explain your situation, and make an offer. Settlement companies typically charge 15 to 25 percent of the debt enrolled or settled. Doing it yourself keeps those fees and gives you direct control over the terms, including how the account is reported.

What is the difference between settled and paid in full on a credit report?

“Paid in full” means you met the original terms of the debt. “Settled for less than the full balance” means a creditor accepted less than what you owed. Both appear on your credit report, but paid in full signals you honored your obligation while settled signals you did not. Lenders reviewing your file treat them differently. In some negotiations, you can ask the creditor to report the account as paid in full as part of the settlement terms, but not all creditors will agree.

How long does debt settlement stay on your credit report?

Seven years from the date of the first missed payment that led to the settlement. The clock starts at the beginning of the delinquency, not when the settlement was finalized. If you missed payments for a year before settling, you still have six more years before the entries drop off. The missed payments and the settlement notation both remain for that full seven-year period, though their negative impact on your score decreases over time.

What is insolvency and how does it affect debt settlement taxes?

Insolvency means your total liabilities exceeded the fair market value of your total assets at the moment the debt was canceled. If you were insolvent, you can exclude forgiven debt from taxable income up to the amount of your insolvency. This is not a general feeling of financial stress. It is a specific calculation documented on IRS Form 982. For example, if you owed $30,000 more than you owned when the debt was settled, and $10,000 was forgiven, the full $10,000 could potentially be excluded from income. A tax professional should review whether you qualify before you file.

Is debt settlement better than bankruptcy?

It depends on the amount of debt, the types of debt, and your overall financial picture. Debt settlement resolves specific debts for less than owed but leaves a negative mark on your credit for seven years and typically triggers a tax bill. Bankruptcy can discharge a wider range of debt without a tax bill, but Chapter 7 stays on your credit report for ten years and has other eligibility requirements. Neither is inherently better. They are different tools for different situations. A nonprofit credit counselor or a bankruptcy attorney can help you compare the actual costs and consequences for your specific circumstances before you commit to either.