Is it better to own or rent? The debate has been producing mostly slogans for decades. One side says renting is throwing money away. The other says a house is a trap. Neither version is the full picture. Both are designed to sound clean enough that you stop asking questions and just pick a side. The truth is that whether it is better to own or rent depends on numbers that vary by market, by timeline, by how much cash you have, and by what you are willing to take on. And the housing industry, on both sides, has a financial interest in telling you a version of this story that ends with a transaction. Real estate agents make money when you buy. Landlords make money when you rent. Almost nobody in the room is getting paid to tell you the full picture.

This article is going to be the room where nobody is getting paid. Is it better to own or rent? You need both sides of the ledger to answer that honestly. Here they are.

The Mortgage Is Not the Cost of Owning a Home. It Is the Entry Fee.

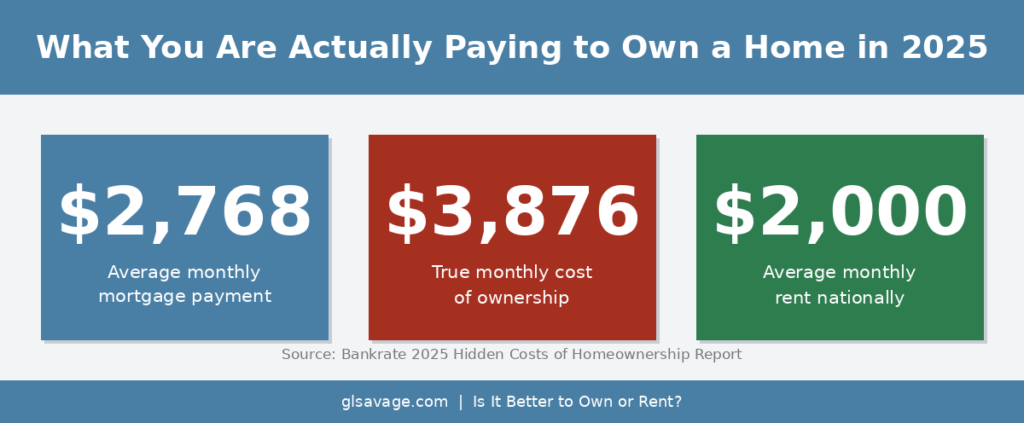

Here is what the comparison looks like right now. The average monthly mortgage payment on a median-priced home, $435,300 as of mid-2025, comes to $2,768 a month including property taxes and insurance. The average monthly rent nationally is $2,000. That is a 38 percent gap in favor of renting, and it exists in all 50 of the largest US metros.

And that figure is just the starting line. It is one of the least complete numbers in the whole calculation. The mortgage gets you through the door. Once you are inside, the actual costs begin.

Bankrate’s 2025 Hidden Costs of Homeownership report found that the average annual cost of owning and maintaining a single-family home in the United States comes to $21,400 a year, not counting the mortgage. That is property taxes, homeowners insurance, utilities, and maintenance. Home maintenance alone averages more than $8,800 annually on a national basis. In high-cost states like Hawaii, California, and New Jersey, total hidden annual ownership costs exceed $30,000. None of those numbers appear in the mortgage payment that people compare to rent.

Then there are the upfront costs. Closing costs when buying typically run 2 to 5 percent of the purchase price. On a $400,000 home that is $8,000 to $20,000 out of pocket before you own a single square foot. Put down less than 20 percent and you also owe private mortgage insurance, which protects the lender, not you, at $100 to $300 or more per month until you reach 20 percent equity. And 83 percent of homeowners experienced at least one unexpected maintenance issue in 2024 according to survey data. Forty-four percent of new homeowners hit their first surprise repair in year one. Twelve percent within the first month.

None of that is a reason not to buy. It is a reason to know what you are walking into before you sign.

A House Is a Physical Machine That Slowly Breaks, and That Is Your Problem Now

When people are deciding whether it is better to own or rent, here is the number that almost never shows up in the conversation: one to four percent of your home’s value every year in maintenance and repairs. Fannie Mae uses two percent as its standard measure. On a $400,000 home that is $4,000 to $16,000 a year, every year, just to keep the building functional. Not to renovate. Not to improve. Just to not fall apart.

Roofs have lifespans. Furnaces die. Water heaters quit. Windows leak. Sewer lines crack. Foundations settle. None of it announces when it is coming. A water heater replacement runs $1,000 to $1,800. A furnace replacement runs $2,500 to $7,500. A roof on a median-sized home runs $8,000 to $20,000. A sewer line repair from the house to the street can run $3,000 to $25,000 depending on how deep the problem goes.

When you rent and the hot water heater breaks, you call the landlord. When you own and the hot water heater breaks, you are the landlord. For a clear-eyed answer to is it better to own or rent, that difference matters enormously. The rent you pay is partly paying for the structural risk of the building. That protection has real dollar value, and it disappears the moment you buy.

Transaction Costs Are the Trap Nobody Explains Until You Are Already In It

Buying and selling a house is expensive in ways that only hurt you if you leave too soon, and the people getting paid to help you buy have no incentive to explain the math clearly.

Closing costs buying run 2 to 5 percent of the purchase price. Real estate commissions on the sale side have historically consumed 5 to 6 percent, though the structure has been shifting since the 2024 NAR settlement. A reasonable estimate for total transaction costs across one purchase and one sale is 8 to 10 percent of the home’s value. On a $400,000 house that is $32,000 to $40,000 in friction, paid coming in and going out, before the other numbers matter.

And a mortgage is structured so that your early payments go almost entirely toward interest, not toward owning more of your house. Lenders call this amortization. In year one of a 30-year mortgage at 6.5 percent on a $350,000 loan, roughly 80 percent of each payment goes toward interest. You are building equity, but slowly. The acceleration comes with time. Leaving early costs you that compounding and hands the transaction costs to a market that does not care about your schedule.

Whether it is better to own or rent often hinges entirely on how long you plan to stay. The general guidance from housing economists is that staying a minimum of five years gives appreciation and equity buildup enough time to overcome transaction costs. In high-cost markets, seven years is safer. Buy and sell in two or three years and there is a real chance you come out behind financially even if the home appreciated, because the appreciation gets consumed by the friction on both ends.

The People Who Bought in 2020 and 2021 Built a Wall That You Are Now Paying For

This is the piece of the housing picture that most directly affects whether it is better to own or rent right now, and almost nobody is explaining it clearly to people on the outside looking in. It is one of the most consequential things happening in American housing.

During the pandemic, mortgage rates fell to historic lows. In early 2021, the average 30-year fixed rate hit 2.93 percent. Millions of people bought or refinanced at those rates. Then in 2022, the Federal Reserve raised rates aggressively to fight inflation. By late 2023, the average 30-year rate had crossed 8 percent. Today it sits around 6.5 to 7 percent.

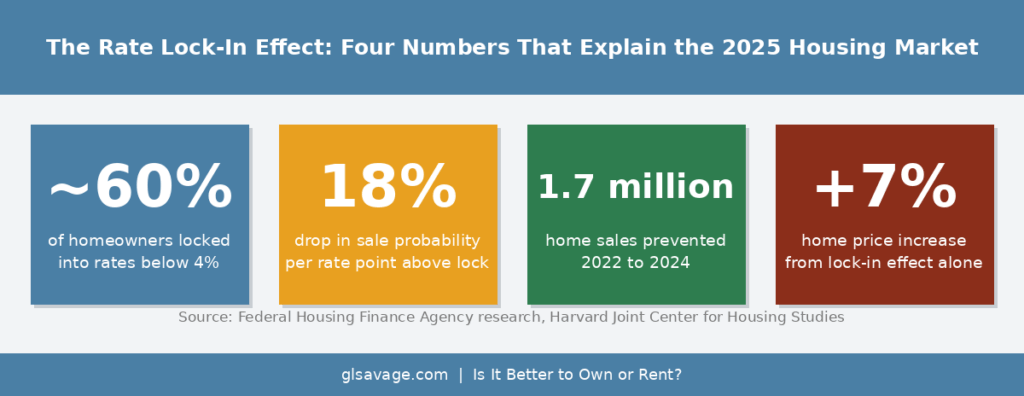

The result: roughly 60 percent of current homeowners with mortgages are locked into rates below 4 percent. Almost 70 percent have rates more than three percentage points below the current market rate. Federal Housing Finance Agency research found that each percentage point by which the current rate exceeds a homeowner’s locked-in rate reduces that owner’s probability of selling by 18 percent. The FHFA estimates that this rate lock-in effect reduced home sales nationally by 1.7 million between 2022 and 2024. The Harvard Joint Center for Housing Studies found that a single percentage-point decrease in average outstanding mortgage rates in 2021 increased home price growth by 8 percentage points between 2021 and 2023.

Here is what that means in plain language. The people who bought cheap are trapped in their houses because selling means trading a 3 percent mortgage for a 7 percent one. On a $300,000 balance that is a difference of nearly $800 a month. So they stay. They do not list. Inventory stays low. And prices stay elevated not because demand is surging but because supply is frozen by financial self-interest. The lock-in effect increased prices by 7 percent, according to the FHFA, on top of the rate increases that were already supposed to cool prices. It is a structural distortion that is actively making housing less affordable for people who do not already own, and it was created by the exact conditions that seemed to make home-ownership such a great deal for the people who got in early.

Inventory is beginning to recover in 2025 and 2026 as more homeowners reach life stages, financial pressures, or fading rate advantages that force or incentivize a sale. But the damage to affordability from those years is not fully unwinding. The people who benefited from the system being designed around their timing are largely still sitting on their gains. The people who were not ready to buy during the pandemic window are still paying for it every month in higher prices and higher rates.

The Tax Deduction That Is Less Useful Than You Were Told

One of the most-cited financial arguments for buying when people debate whether it is better to own or rent is the mortgage interest deduction. It is real for some people. It is largely theoretical for many first-time buyers, and the industry does not explain why.

To claim the mortgage interest deduction, you have to itemize your federal deductions. The 2025 standard deduction is $15,750 for single filers and $31,500 for married filing jointly. A moderate mortgage at current rates might generate $18,000 to $22,000 in annual interest. Add property taxes up to the $10,000 SALT cap, maybe some charitable contributions, and many households sit right at the edge of whether itemizing even beats the standard deduction. For a significant number of moderate-income first-time buyers, the deduction provides little or no actual tax benefit. The home-ownership tax advantage is real and meaningful for high-income households with large mortgages. For many people it is a talking point dressed up as math. Before counting the deduction as a benefit, run the actual numbers: add up your mortgage interest, property taxes, and any other deductions. If they do not clearly exceed the standard deduction for your filing status, the tax benefit is not real for your situation.

The $80,000 That Is Not Invested Anywhere Else

Another number that rarely enters the conversation about whether it is better to own or rent: the opportunity cost of the down payment. A 20 percent down payment on a $400,000 home is $80,000. Once it goes into the house, it is locked into one illiquid, undiversifiable asset in one location. It cannot sit in a high-yield savings account. It cannot compound in an index fund. It earns whatever the local housing market earns, minus all the costs described above.

If that $80,000 were invested in a diversified index fund at a historical average of 7 percent annually after inflation, it would be worth roughly $157,000 in ten years without a single additional contribution. That is not an argument against buying. Home appreciation is real and in some markets has been extraordinary. But the opportunity cost of the down payment is a real number that belongs in an honest comparison. It almost never appears in one, because nobody selling you a house has an incentive to put it there.

The Wealth Gap Is Real and It Only Runs One Direction

Here is the counterargument, stated plainly, because all the criticisms above do not erase it.

The median net worth of a homeowner in the United States is approximately $400,000. The median net worth of a renter is approximately $10,400. That is a ratio of nearly 40 to 1. That gap does not exist purely because wealthier people buy, though that is part of it. It also exists because home-ownership forces a savings discipline that most people do not replicate voluntarily as renters. Every mortgage payment builds equity. The equity compounds over decades. The house, imperfect financial instrument that it is, creates a forced wealth-building mechanism that a lease does not.

The wealth gap also compounds inter-generationally. Homeowners pass on assets. Renters generally do not. That dynamic is a meaningful driver of the widening wealth divide in this country, and it runs in one direction. Knowing that does not tell you that buying is right for your situation today. It tells you that the decision you are making has stakes that extend further than the monthly payment comparison. If you are working on building financial stability while figuring this out, Build an Emergency Fund Living Paycheck to Paycheck covers the foundation that makes either option more survivable.

What Renting Actually Costs That Nobody Says Out Loud

Renting gets an easier ride in the rent-vs-buy debate than it deserves.

Renters face rent increases that compound over time with no ceiling. Someone paying $1,800 a month in 2019 and still in the same unit in 2025 may be paying $2,400 or more. There is no fixed-rate equivalent of a 30-year lease. The payment stability of a fixed mortgage over a long time horizon is real and should not be dismissed. The renter who feels confident today because rent is lower than the mortgage on an equivalent house is making a short-term comparison that becomes less favorable with every passing year if rents keep climbing.

Renters can also be displaced without meaningful control over the timing. A landlord can sell. A landlord can convert to condominiums. A landlord can decline to renew a lease. Tenant protections vary enormously by state and city. In many markets, a renter has very limited recourse when the building changes ownership or the landlord simply wants the unit back. The stability of home-ownership is not just psychological. It has real practical value that is hardest to quantify and easiest to miss until it is gone.

And cheap rent is not the same as cheap housing. Poor insulation, aging appliances, paid parking, coin-operated laundry, a long commute, or frequent forced moves because the landlord raises rent or fails the building can make a lower-rent unit genuinely more expensive in total cost than a higher-rent unit that includes those things.

The Home-ownership Identity Trap Costs Real Money

This is the part that almost never appears in financial analysis of whether it is better to own or rent, and it is one of the most expensive traps in the whole picture.

Buying a house becomes part of a person’s identity in a way that few other financial decisions do. It is a social signal. It communicates stability, adulthood, arrival. Once someone owns, selling the house or acknowledging that the financial reality does not match the expectation can feel like admitting failure in a very public way. People stay in financially stressful situations, refinance repeatedly to extract equity and reset the clock, delay other life decisions, or absorb years of budget strain rather than admit the house was the wrong call at the wrong time.

This dynamic keeps people in situations that no spreadsheet would recommend. It is not weakness. It is how identity works under social pressure. But the house you cannot admit was a mistake is the most expensive house you own, and naming that trap before you close is worth whatever discomfort it requires.

How to Actually Make This Decision for Your Specific Situation

Here is the framework that cuts through the slogans and gives you a real answer for your specific situation.

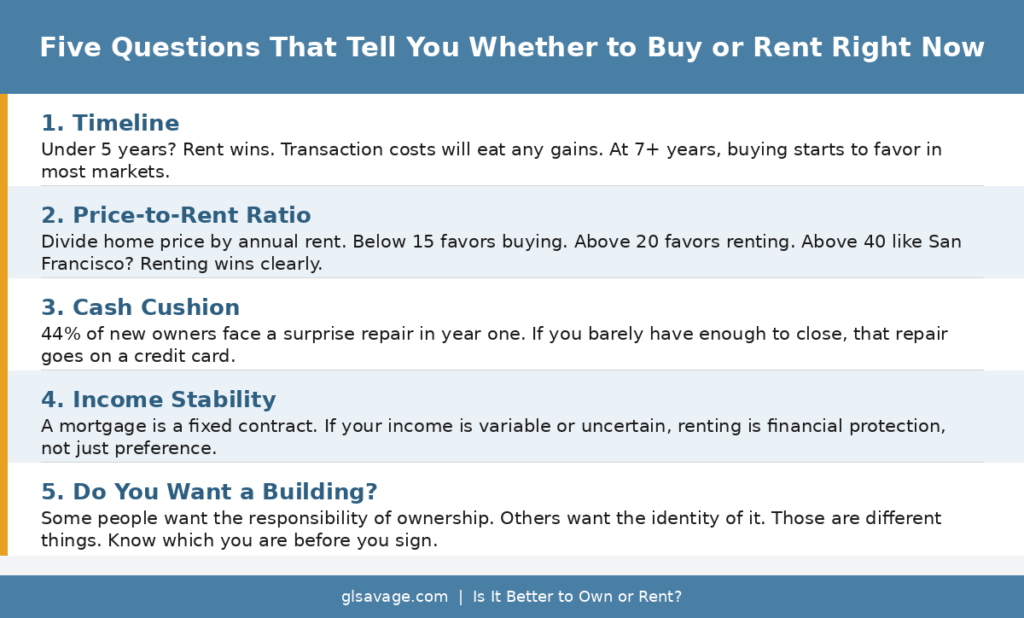

The first question is timeline. If you are staying fewer than five years, renting wins in almost every market because transaction costs will consume any appreciation and early-year equity gain. If you are staying seven or more years, ownership starts to favor in most markets assuming the other numbers work. This variable matters more than any other and gets the least attention.

The second question is the price-to-rent ratio in your specific market, not the national average. Divide the purchase price of a comparable property by its annual rent. Below 15 generally favors buying. Between 15 and 20 is market-dependent. Above 20 generally favors renting on a pure cost basis. In San Francisco, the ratio exceeds 40 in many neighborhoods. In parts of the Midwest, it sits below 10. The same logic does not apply in both markets and national-level advice is largely useless for making a real decision about a specific property in a specific city.

The third question is cash cushion. Do you have enough beyond the down payment and closing costs to absorb a first-year repair without going into debt? Forty-four percent of new homeowners face a surprise repair in year one. Buying with exactly enough to close means the first broken furnace or failed water heater lands on a credit card. The cushion is not optional. It is part of the real cost of being ready to own.

The fourth question is income stability. A mortgage is a fixed contractual obligation. Missing it has consequences that rent arrears typically do not carry in the short term. If your income is variable, contract-based, or uncertain in the near term, the flexibility of renting is not just preference. It is financial protection from a commitment that does not flex when your income does. Why a Second Job Often Costs More Than It Pays is worth reading before assuming income can be supplemented easily if the mortgage gets tight.

The fifth question is the one nobody asks out loud: do you actually want to own a building? The maintenance, the repairs, the systems that fail on their own schedule, the calls to the plumber, the bills that follow. Some people want this and find real satisfaction in it. Others discover after closing that they wanted the identity of home-ownership, not the responsibility. Those are different things. Knowing which you are before you sign is worth whatever self-examination it takes.

If you want a free tool to run the actual numbers for your specific situation, the New York Times Rent vs Buy Calculator is the most honest one publicly available. It lets you adjust timeline, local market appreciation assumptions, investment return assumptions on the down payment alternative, and the full range of ownership costs. Run it with honest numbers, not optimistic ones.

Both Slogans Are Wrong. Here Is What Is Actually True.

Is it better to own or rent? Neither slogan gets you there. Renting is not throwing money away. Every month of rent buys housing, flexibility, and protection from structural risk. That is not nothing. It is a service with real value.

Buying is not automatically building wealth. It is potentially building wealth, subject to market conditions, maintenance costs, transaction timing, how long you stay, how honestly you count the costs, and whether you bought at a price that reality can support.

The housing industry, on both sides, profits from your transaction. The agent who tells you that renting is throwing money away makes a commission when you buy. The financial content that tells you buying is a trap often sells you something else. Almost nobody in the conventional housing conversation is paid to tell you that whether it is better to own or rent is genuinely conditional and depends on variables specific to your life.

Now you have those variables. Is it better to own or rent? The answer is specific to your market, your timeline, and what you are actually willing to take on. Run the numbers honestly. The decision is yours to make with real information instead of a slogan.

Frequently Asked Questions About Renting vs Buying

Is renting really throwing money away?

No, and this is one of the most persistent myths in housing. Rent pays for housing, flexibility, maintenance protection, and the ability to move without a transaction that costs 8 to 10 percent of a home’s value. Whether renting or buying is financially superior depends entirely on your market, your timeline, and whether you count all the costs on both sides honestly. In 2025, the average mortgage payment on a median-priced home runs $2,768 versus $2,000 in average monthly rent nationally , a 38 percent gap. Renting is cheaper on a monthly basis in all 50 of the largest US metros.

What do most people forget to count when comparing renting vs buying?

On the ownership side: closing costs, property taxes, homeowners insurance, PMI if down payment is below 20 percent, annual maintenance and repairs at 1 to 4 percent of home value, and transaction costs of 8 to 10 percent of home value when selling. On the renting side: annual rent increases that compound over years, displacement risk when leases end, and the absence of forced equity accumulation. Both sides have costs that disappear from the monthly payment comparison most people stop at.

What is the rate lock-in effect and why does it matter to people trying to buy right now?

The rate lock-in effect is what happens when a large share of existing homeowners hold mortgages at rates far below the current market rate and are financially disincentivized to sell. Federal Housing Finance Agency research found that each percentage point by which market rates exceed a homeowner’s locked-in rate reduces their sale probability by 18 percent. The FHFA estimates this reduced home sales by 1.7 million between 2022 and 2024 and increased home prices by 7 percent as a result. For people trying to buy in 2025, this means they are competing in a market where supply is artificially constrained by the financial self-interest of people who got lucky on timing. That is not a market failure in the technical sense. It is just how the incentives landed.

How long do you need to stay in a home for buying to make financial sense?

Timeline is the single variable that most directly determines the answer for your situation. Most housing economists recommend a minimum of five years, with seven or more being more appropriate in high-cost markets. Transaction costs of 8 to 10 percent of the home’s value have to be overcome by appreciation and equity buildup before buying comes out ahead. In the early years of a mortgage, most of each payment goes toward interest rather than principal, which slows equity accumulation significantly. Buying and selling within two or three years makes it genuinely likely that you will come out behind financially even if the home appreciated.

What is the price-to-rent ratio and how do I use it?

The price-to-rent ratio is the single most useful local data point when working out is it better to own or rent in your specific market. Divide the purchase price of a home by its annual rent for a comparable property. A ratio below 15 generally favors buying. Between 15 and 20 is market-dependent. Above 20 generally favors renting on a pure cost basis. In San Francisco and other expensive coastal markets, the ratio often exceeds 40. In many Midwest and Rust Belt cities it falls below 10. National rent-versus-buy advice is largely useless because the correct answer differs that dramatically between markets. Run the ratio for your specific city and neighborhood before making any decision. The ratio is the fastest shortcut to knowing whether it is better to own or rent where you actually live.

What is the opportunity cost of a down payment?

One number that most rent-vs-buy analyses skip entirely: the opportunity cost of the down payment, meaning what that money could have earned if it went somewhere else instead. An $80,000 down payment invested in a diversified index fund at a historical average return of 7 percent annually would be worth roughly $157,000 after 10 years. That does not make renting automatically better than buying. But it means the down payment is not free money sitting idle. It has an alternative use with a real expected return, and that return belongs in an honest comparison between the two options. Most buy-versus-rent analyses omit it or bury it in assumptions the reader never sees.

Does the mortgage interest deduction make buying more affordable?

For some buyers, meaningfully. For many moderate-income first-time buyers, less than expected. Claiming the deduction requires itemizing, which only makes sense if total itemized deductions exceed the $30,000 standard deduction for married filers in 2025. Many households with moderate mortgages, even including property taxes at the $10,000 SALT cap, do not significantly exceed the standard deduction. For those households, the tax benefit of the mortgage is largely theoretical. The deduction matters most for high-income buyers with large loans.

When does renting make more financial sense than buying?

Renting wins when you plan to stay fewer than five years, when the local price-to-rent ratio is above 20, when your income is variable or uncertain, when you do not have enough savings beyond the down payment to absorb first-year repairs without going into debt, or when the monthly cost difference between renting and owning is large enough that investing the difference produces competitive long-term returns. In 2025, in high-cost coastal markets, most of these conditions are simultaneously true. In those situations, renting is not a consolation prize. It is the correct answer to whether it is better to own or rent given your actual circumstances. The break-even point for buying in those markets requires long holding periods and appreciation assumptions that the current rate environment does not obviously support.

Is there a free tool to run the actual numbers for my specific situation?

Yes. The New York Times Rent vs Buy Calculator is the most honest publicly available tool for this calculation. It lets you adjust timeline, local appreciation assumptions, investment return assumptions on the down payment alternative, and the full range of ownership costs including maintenance, taxes, and insurance. Run it with honest numbers, not the optimistic version. The result will tell you more than any slogan about this decision ever has.