About 45 percent of renters in the United States have no renters insurance at all. That number is easy to criticize until you look at what the other 55 percent actually bought. Most people who have renters insurance do not understand what renters insurance covers, what it excludes, or the one decision that determines whether their payout after a loss will cover their actual costs or fall thousands of dollars short. The policy costs between $15 and $30 a month. The gap between the right policy and the wrong one can be the difference between replacing everything you own and replacing about half of it.

This article covers what renters insurance covers, what it does not, the traps built into most standard policies that nobody explains at the point of sale, and what to check before you assume you are protected.

What Renters Insurance Actually Covers

A standard renters insurance policy covers three things: your personal belongings, your liability if someone is hurt in your home, and your living expenses if you are temporarily displaced because of a covered loss. That is the framework. The details inside each category are where it gets complicated.

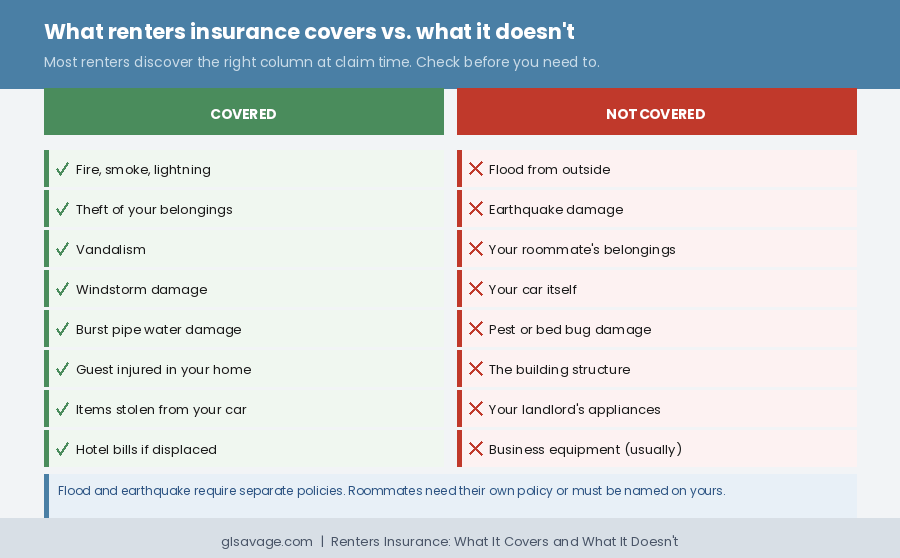

Personal property coverage pays to replace or repair your belongings if they are damaged or destroyed by a covered event. Covered events, called named perils in insurance language, meaning specific events the policy names and covers, typically include fire, smoke, lightning, theft, vandalism, windstorms, and water damage from internal sources like a burst pipe. The key word is internal. A burst pipe is covered. A flood from outside is not. That distinction has cost people everything, and most renters only find out about it when it is too late.

Liability coverage protects you if someone is injured in your home and you are held legally responsible. If a guest trips and breaks their wrist, or if your dog bites someone, liability coverage can pay their medical bills and cover your legal costs if they sue. Most standard policies include $100,000 in liability coverage, with options to increase that amount. This part of the policy also covers certain accidents you cause away from your home. If you accidentally break a friend’s television, for example, your liability coverage can step in.

Additional living expenses coverage, sometimes called loss of use coverage, pays for the cost of living somewhere else if your rental becomes uninhabitable due to a covered loss. Hotel bills, restaurant meals, and other costs above your normal spending are covered up to a limit while your unit is being repaired or until you find a new place. This coverage does not kick in for every reason you might need to leave. Only covered perils trigger it. Knowing what those perils are before you need to file a claim is how you avoid surprises.

The Trap Most People Fall Into Before They Even File a Claim

There is a decision embedded in every renters insurance policy that most people never notice when they sign up. It determines how much you get paid when you file a claim. It is called the valuation method, and it comes in two forms: actual cash value and replacement cost coverage.

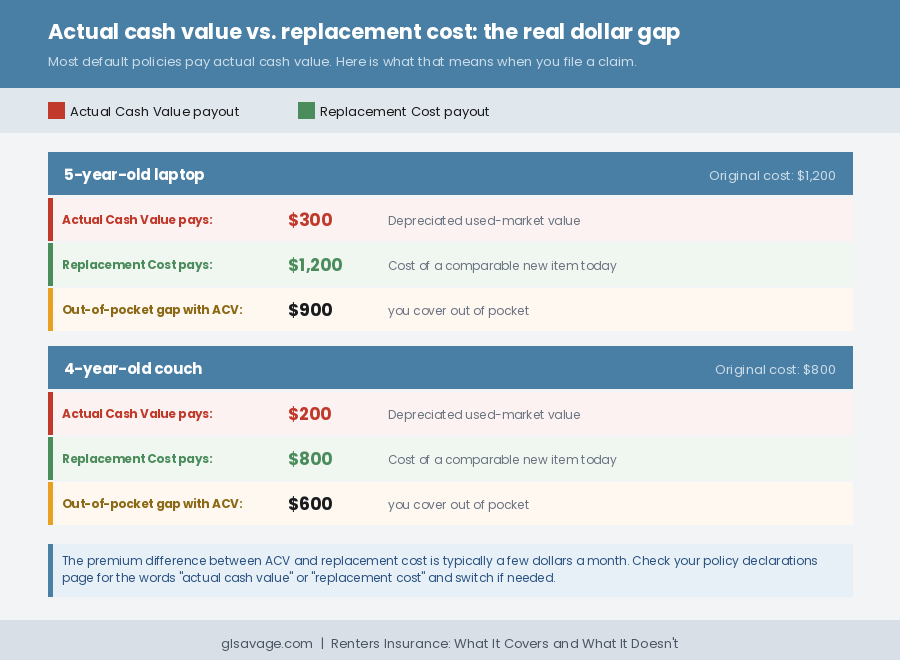

Actual cash value, which is how most default policies work unless you specifically choose otherwise, pays you what your belongings were worth at the time of the loss, not what it costs to replace them. Insurance companies calculate this by taking the original purchase price and subtracting depreciation based on age and condition. Your five-year-old laptop that cost $1,200 might be worth $300 in actual cash value by the time you file a claim. Your four-year-old couch that cost $800 might pay out $200. You pocket the depreciated amount and pay the rest yourself when you go to replace what you lost.

Replacement cost coverage pays what it actually costs to buy a comparable new item at today’s prices, regardless of how old the original was. The same five-year-old laptop gets replaced with a comparable new one. The difference in premium between actual cash value and replacement cost is typically only a few dollars a month. The difference in payout after a significant loss can be thousands of dollars. Read The Poverty Premium Explained: How to Fight Back for broader context on how financial products sold to people with fewer resources are routinely structured to pay out less than people expect.

If you have renters insurance right now and have never checked which type you have, check today. Look at your policy declarations page, the summary page at the front of your policy, and look for the words “actual cash value” or “replacement cost.” If it says actual cash value and you cannot easily afford to cover the depreciation gap yourself in the event of a major loss, switch to replacement cost coverage. The price difference is small. The protection difference is not.

Renters Insurance Exclusions: What the Policy Does Not Cover

The exclusions are where most people discover that renters insurance what it covers is not the same as what they assumed it covered. Understanding renters insurance coverage means knowing these limits as well as you know the benefits.

Floods are not covered. This is the single most misunderstood exclusion in renters insurance. A burst pipe that sends water through your ceiling is covered. That is internal water damage from a named peril. Rain or floodwater coming in from outside, a river overflowing, storm surge: none of that is covered by a standard policy. Flood insurance is a separate product, available through private insurers or through the federal National Flood Insurance Program. If you live in a flood-prone area or even in a building that has flooded before, your renters insurance will not protect you unless you buy flood coverage separately.

Earthquakes are not covered. Like floods, earthquake damage requires a separate policy or an add-on rider. Most renters never buy it unless they live in a known seismic zone, and even then, many do not.

Your roommate’s belongings are not covered. Unless your roommate is specifically named on your policy, their possessions are excluded. This surprises a lot of renters who assume sharing a policy means sharing coverage. Most insurers will allow a roommate to be added to a policy, but it requires explicitly doing so. Otherwise each person in the unit needs their own policy.

Your car is not covered. Renters insurance covers items stolen from your car, but it does not cover the vehicle itself. If your car is stolen or damaged in a storm, that is an auto insurance claim, not a renters insurance claim.

Pest damage is not covered. Bed bugs, rodents, insects: any damage caused by pests is excluded from standard renters insurance because insurers treat it as a maintenance issue, not a sudden loss event. If you have to throw out a mattress and half your furniture because of a bed bug infestation, renters insurance will not pay for it.

Your landlord’s property is not covered. The appliances that came with the unit, the fixtures, the structure of the building: all of that falls under your landlord’s insurance. Your renters insurance covers what you own, not what they own. See What Your Landlord Is Not Required to Tell You for more on where your landlord’s responsibility ends and yours begins.

The Sublimit Problem Nobody Tells You About

Even when a loss is covered, renters insurance does not always pay what you expect. This is the part of renters insurance what it covers that the insurance company does not lead with. Most standard policies contain sublimits, which are caps on specific categories of belongings that apply even when the total damage is well within your overall coverage limit.

Jewelry is the most common sublimit trap. A typical standard renters insurance policy covers jewelry theft up to $1,500 regardless of what you actually own. If your overall personal property coverage is $30,000, and a burglar takes your engagement ring, your grandmother’s earrings, and everything else in your jewelry box, the most you will see is $1,500. Not $30,000. Not the actual value of what was taken. Fifteen hundred dollars. The average engagement ring alone costs around $6,500. If yours is worth more than $1,500, the gap is your problem unless you scheduled the item, meaning you specifically listed it on the policy with its appraised value and paid a small additional premium to cover it at full value.

Cash is typically capped at $200 under most standard policies. Electronics often have sublimits as well, depending on the policy and the state. Business property, meaning equipment, inventory, or tools you use for work, is usually capped at $2,500 or less under a standard policy, and often excluded entirely for any business-related loss. If you work from home and your work laptop is stolen, you may find it falls under the business property limit rather than the standard electronics coverage.

The fix for sublimits is scheduled personal property coverage, sometimes called a floater or an endorsement. You list the specific items by name, have them appraised, and pay a small additional premium to insure them at their actual value. A $6,500 engagement ring typically costs around $1 to $2 per month to schedule. Most people never do it because nobody tells them the sublimit exists.

How Much Coverage Do You Actually Need

Most renters dramatically underestimate the value of what they own. The average renter has somewhere between $20,000 and $30,000 worth of personal property when they add up furniture, electronics, clothing, kitchen items, books, bikes, and everything else. Most people buying renters insurance pick a number that sounds reasonable without doing the math.

The right way to determine how much coverage you need is to do a home inventory. Walk through every room and estimate what it would cost to replace everything you see at today’s prices, not what you paid for it. Start with your electronics. Add your furniture. Add your clothing. An entire wardrobe of adult clothing costs more than most people think when they price it out item by item. Add your kitchen equipment, your bike, your musical instruments, your books. Add anything in storage. The total will likely surprise you.

Set your personal property coverage limit at or above that number. Then look at your liability coverage. A standard $100,000 limit is a reasonable starting point, but if you have significant assets or a situation that creates elevated liability risk, such as a dog or regular guests, consider increasing it. Liability coverage is cheap relative to what it protects.

Your deductible is the amount you pay out of pocket before insurance kicks in. A higher deductible means a lower monthly premium but more out-of-pocket cost at claim time. A lower deductible means a slightly higher premium but less friction if something actually happens. For most renters, a deductible between $500 and $1,000 strikes a reasonable balance. Read Build an Emergency Fund Living Paycheck to Paycheck to understand why having that deductible amount accessible before you need it matters as much as having the policy itself.

The Four Things to Check on Your Policy Right Now

If you already have renters insurance and want to check whether renters insurance what it covers matches what you actually own, these are the four things worth verifying today.

First, confirm you have replacement cost coverage, not actual cash value. If you have actual cash value, price out the upgrade. It is almost always worth it.

Second, check your sublimits for jewelry, electronics, and cash. If you own anything in those categories worth more than the sublimit, schedule the specific items. Contact your insurer and ask what it costs to add scheduled coverage for the items that matter.

Third, check whether flood coverage is relevant for where you live. If you are in a flood-prone area or in a building that has experienced flooding, look into standalone flood insurance. Your renters policy will not help you if the water comes from outside.

Fourth, confirm whether your roommate is named on your policy. If they are not, their belongings are not covered. If they think they are covered because you have a policy, they are wrong. Each person needs their own policy or needs to be explicitly named on yours.

The Honest Takeaway

Renters insurance is one of the least expensive and most overlooked forms of financial protection available to people who rent. At $15 to $30 a month, even a well-structured policy with replacement cost coverage and properly scheduled valuables costs less than most streaming subscriptions. The reason so many renters either skip it entirely or buy the wrong version is that nobody walks them through what renters insurance covers and what it does not before they make the decision. Understanding renters insurance what it covers, and what it does not, is how you buy the right one. Knowing the difference means you can fix it before the loss, not after.

Frequently Asked Questions

What does renters insurance cover?

A standard renters insurance policy covers three things: your personal belongings against named perils like fire, theft, and vandalism; personal liability if someone is injured in your home or you accidentally damage someone else’s property; and additional living expenses if you are temporarily displaced because of a covered loss. It does not cover the structure of the building, your car, your roommate’s belongings unless they are named on the policy, or damage from floods or earthquakes.

Does renters insurance cover flooding?

No. A standard renters insurance policy does not cover flood damage. It does cover internal water damage from a burst pipe or a leaking appliance, but water that enters from outside, such as rain, storm surge, or an overflowing river, is excluded. Flood insurance is a separate product available through private insurers or the federal National Flood Insurance Program. If you live in an area prone to flooding, you need to purchase flood coverage separately.

What is the difference between actual cash value and replacement cost renters insurance?

Actual cash value pays you what your belongings were worth at the time of the loss, after accounting for depreciation. A five-year-old laptop might pay out $300 even though a comparable new one costs $1,200. Replacement cost pays what it actually costs to buy a comparable new item today. The premium difference is typically only a few dollars a month. The payout difference after a major loss can be thousands of dollars. Replacement cost is almost always the better choice.

What are sublimits in renters insurance?

Sublimits are caps on specific categories of belongings that apply even when the total loss is within your overall coverage limit. Most standard policies cap jewelry theft coverage at $1,500 regardless of what your jewelry is actually worth. Cash is typically capped around $200. Business property is often capped at $2,500. If you own items in these categories worth more than the sublimit, you need to schedule those specific items on your policy, meaning you list them by name and value for a small additional premium to cover the full amount.

Does renters insurance cover my roommate?

Only if they are specifically named on your policy. Renters insurance does not automatically extend to other people living in the unit. If your roommate is not listed on your policy, their belongings are not covered. Each person either needs their own policy or needs to be explicitly added to yours. If your roommate thinks your policy covers them and they are not named on it, they are uninsured.

How much renters insurance do I need?

Start by doing a home inventory. Walk through every room and estimate what it would cost to replace everything you own at today’s prices. Most renters find they own between $20,000 and $30,000 worth of property when they actually add it up. Set your personal property coverage at or above that number. Set your liability coverage at a minimum of $100,000, higher if you have a dog or regular guests. Choose replacement cost valuation over actual cash value. Keep your deductible at a level you could actually pay out of pocket if you needed to file a claim tomorrow.

Does renters insurance cover theft outside my home?

Yes, in most cases. Most standard renters insurance policies cover theft of your belongings even when it occurs away from home: a laptop stolen from a coffee shop, items taken from a hotel room while traveling, or things stolen from your car. However, the theft sublimits still apply when you are away from home. If your jewelry is stolen while you are traveling, the same $1,500 cap applies as if it had been stolen from your apartment. The coverage travels with you, but the limits travel with it too.

Is renters insurance worth it?

Yes, if you buy it correctly. A policy with replacement cost coverage and properly scheduled valuables costs between $15 and $30 a month for most renters. That covers replacing your furniture, electronics, and clothing in a fire or theft, your hotel bills if you are displaced, and your legal costs if a guest is injured in your home. The risk of any single one of those events in any given year is low. The cost of any one of them without insurance is high. Understanding renters insurance what it covers at the policy level is how you avoid that outcome. The product only fails when people buy the cheapest default version without checking the valuation method or the sublimits.