A raise is supposed to be good news. You take on more, stay longer, perform better, and finally get a few more dollars an hour. The obvious assumption is that your financial situation improves. Sometimes it does. Sometimes the system hands you a raise with one hand and takes a chunk of it back with three others, and nobody warns you it is coming. Your paycheck goes up. Your SNAP goes down. Your ACA subsidy recalculates. Your childcare copay rises. Your tax refund shrinks. None of that happens on the same schedule, from the same office, or with any coordination between the programs involved. You are the one standing in the middle when all of it lands. This is what that actually looks like, program by program, and what you can do about it before it catches you off guard.

The Benefit Cliff: What It Actually Means

The phrase gets used a lot without being explained clearly. Here is what it actually means. Many government assistance programs are built around income thresholds. Below the line, you qualify. Above it, you do not, or you qualify for less. When a raise pushes your income over one of those lines, the program recalculates. The problem is not that recalculation happens. The problem is the math that results from it. In the worst cases, the loss in benefits exceeds the gain from the raise, leaving the household worse off financially than before the raise happened.

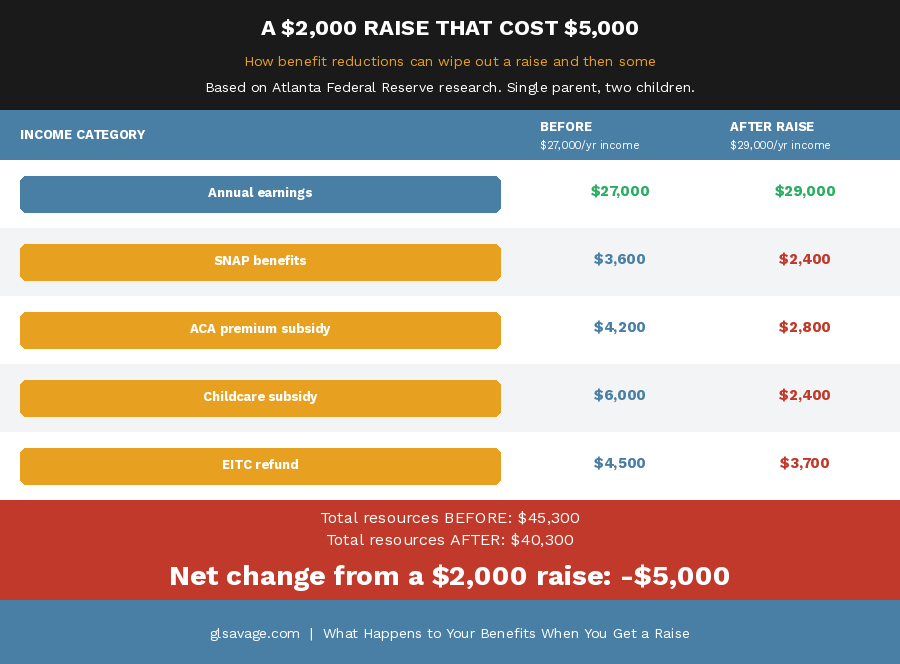

Research from the Atlanta Federal Reserve documented one scenario where a single parent with two children saw their income rise from $27,000 to $29,000. A $2,000 raise. It triggered a net loss of $6,000 in total resources when the benefit reductions were counted. The raise was real. The net position was worse. That is the cliff. The U.S. Department of Health and Human Services reports that about a quarter of lower-income workers face effective rates of more than 70 percent when you count both taxes and the loss of benefits together on every extra dollar they earn. The posted wage has almost nothing to do with the actual result. A survey in Tennessee found that once the benefit cliff was explained to them, 85 percent of lower-income parents said they had experienced one. Within that group, 63 percent had resisted working additional hours, 50 percent had resisted taking a better-paying job, and one in four had turned down a raise outright. That is not irrational behavior. That is a rational response to a system that has already taught them the math the hard way.

What Happens to SNAP When Your Income Goes Up

Food assistance is one of the first places people worry about, and the mechanics are more nuanced than a simple on-off switch. SNAP eligibility runs through both a gross income test and a net income test in most states, with deductions allowed for housing costs, dependent care, and medical expenses. A raise does not automatically eliminate benefits, but it feeds into the formula. The basic rule is that SNAP benefits decrease by roughly 30 cents for every dollar of net income increase. A $200-a-month raise in net income reduces SNAP by around $60 a month. That is not catastrophic by itself. The damage comes from the stacking when other programs adjust at the same time.

What most people are not told: the timing of reporting matters enormously. SNAP has reporting rules that vary by state, and when you report a raise relative to your certification period determines when the benefit change hits. Some households report mid-period and see an immediate adjustment. Others do not feel it until recertification. Either way, the system does not pause to let the raise build up a cushion first. The benefit drops as soon as the new income is counted, whether or not you have had time to absorb the transition. When the raise happens, contact your state SNAP office and ask specifically: when does this income need to be reported, and when will the benefit change take effect? Knowing the exact date is more useful than a general warning.

There is also a legislative change that affects SNAP and is worth knowing about. The One Big Beautiful Bill, signed into law on July 4, 2025, expanded SNAP work requirements to adults ages 55 to 64 without dependent children, and to parents whose youngest child is 14 or older. If you fall into either of those groups and you were not previously subject to work requirements, that has changed. The law also restricts how much SNAP benefits can increase each year, capping future increases to the annual cost-of-living adjustment each October. If a raise reduces your SNAP and you were counting on the benefit keeping pace with food costs more broadly, that cushion is smaller going forward than it used to be.

What Happens to Your ACA Health Insurance Subsidy

This one has a specific and expensive trap that does not show up until tax season, and it catches people completely off guard. If you buy coverage through the ACA Marketplace and receive advance premium tax credits, meaning the government pays part of your monthly health insurance premium directly to your insurer to lower your cost, your subsidy is calculated based on your estimated annual income. The Marketplace uses that estimate to reduce your monthly premium in real time throughout the year. When you file your taxes, the IRS reconciles what you actually earned against what you estimated. If your income was higher, the subsidy you received was higher than you were entitled to. The difference has to be paid back.

A raise mid-year creates a tax bill you were not expecting. The premium felt affordable all year. Then April arrives and the reconciliation happens. The fix is straightforward but it requires action before it becomes a problem: update your income estimate at healthcare.gov as soon as you know the raise amount. Do not wait. Every month the old estimate stays in the system is a month of potential overpayment that becomes a repayment obligation at filing. Updating the estimate triggers a premium adjustment going forward and limits or eliminates what you owe.

Here is the part almost nobody outside of tax circles knows: contributing pre-tax dollars to a 401k, a traditional IRA, or an HSA all reduce your Modified Adjusted Gross Income, which is the income figure the government uses to calculate your subsidy. It is different from your paycheck number. Think of it as the income the IRS sees after certain deductions are taken out. Every dollar you put into a traditional 401k or an HSA through payroll reduces that number by a dollar, which can keep your subsidy intact even as your paycheck rises. The 2026 HSA contribution limits are $4,400 for self-only coverage and $8,750 for family coverage. If your employer offers a high-deductible health plan with HSA eligibility, this is one of the most powerful tools available for someone navigating a raise near an ACA threshold. The people who need this strategy most are almost never the ones who have been told it exists.

What Happens to Medicaid When Your Income Increases

Medicaid eligibility varies by state and by the category you fall into, which makes the system harder to navigate than it should be. A raise can push someone over the eligibility threshold for their category. When that happens, the question becomes what replaces the coverage and what it costs. Medicaid is often zero premium, zero or very low copays. Marketplace coverage, even subsidized, comes with premiums, deductibles, and out-of-pocket exposure. The transition can feel like a cliff because it effectively is one. You lose low-cost coverage and move into a more expensive system, all because income rose by an amount that may not cover the difference in healthcare costs.

One documented case shows a parent in Ohio who received a raise to $21 an hour, which pushed their income over the CHIP eligibility limit and also triggered an increase in childcare copayments. The family would not regain the financial ground lost until the parent earned $27 an hour. Six dollars an hour of raises just to get back to even. Some states have expanded Medicaid eligibility or put in place gradual tapers to reduce the cliff effect. If you are approaching a Medicaid income threshold, contact your state Medicaid office directly and ask whether there is a transitional coverage period, whether you qualify for extended eligibility, and exactly what income level triggers the change. The system does not volunteer this information. You have to ask for it.

The rules around Medicaid just changed significantly and most people have not been told. The One Big Beautiful Bill, signed July 4, 2025, introduced Medicaid work requirements for expansion enrollees. Starting January 1, 2027, adults ages 19 to 64 who receive Medicaid through the ACA expansion, meaning people who qualified for Medicaid specifically because their state expanded eligibility under the Affordable Care Act, must show 80 hours per month of qualifying activity, which can include employment, job training, education, or community service. States can implement this earlier if they choose. Eligibility renewals are also moving from annual to every six months beginning late 2026, which means more frequent paperwork, more chances to fall through the cracks, and more opportunities for coverage to lapse even for people who technically still qualify. Here is the cliff inside the cliff: the new law specifically makes people who lose or are denied Medicaid because of work requirements ineligible for ACA Marketplace premium tax credits. That means losing Medicaid for a work requirement violation does not open the door to subsidized Marketplace coverage. It opens the door to nothing. If you receive Medicaid expansion coverage and a raise is moving you toward the eligibility line, understanding this new landscape matters more now than it did a year ago.

What Happens to Childcare Assistance When Your Pay Goes Up

This one lands hardest on the households that were working hardest to build stability, because childcare costs are often the largest single expense in the budget and childcare assistance is what makes working possible in the first place. The federal CCDF program, which funds most state childcare assistance, now limits family copayments to no more than seven percent of household income. But a higher income still means a higher dollar copay, and in some cases a raise pushes income over the eligibility line entirely. When that happens, the family faces full market-rate childcare costs, which in many metro areas run $1,500 to $2,500 a month per child. A $2-an-hour raise does not cover that gap. Not even close.

The timing issue makes this worse. Childcare assistance eligibility is typically re-evaluated at recertification, which runs on its own schedule with no connection to when raises occur. A raise in March might not affect the copay until the September recertification. Then it arrives all at once rather than gradually, and the household absorbs a large payment increase with no lead time to plan. If you know a raise is coming and you receive childcare assistance, contact your program administrator before the raise takes effect and ask exactly when and how the income change will be applied. The earlier you know the timeline, the more time you have to plan around it. Why a Second Job Often Costs More Than It Pays covers the same stacking dynamic from a different angle and is worth reading alongside this one.

What Happens to SSI When Your Earnings Change

Supplemental Security Income uses an earned income formula that reduces the monthly benefit as countable earnings rise. The structure is straightforward: SSI disregards the first $65 of monthly earnings plus half of anything above that. So for every $2 in earnings above $65, the SSI payment drops by $1. A raise or added hours does reduce the benefit payment. Total cash into the household may still improve, but the gain is smaller than the raise alone suggests. If you are on SSI and your earnings change, you are required to report that change to the Social Security Administration. Failing to report can result in overpayment claims later, which create their own financial damage. The SSA has a program called Ticket to Work that provides free employment support services for people on SSI or SSDI who want to work more without immediately losing benefits. Most people who are eligible for it have never heard of it. Search “SSA Ticket to Work” to find the program directly on the SSA website.

What Happens to the EITC and Your Tax Refund

The Earned Income Tax Credit is one of the most powerful income support tools in the tax code, and a raise can shrink it in ways that most people never connect to the raise at all. The EITC is structured to increase as earnings rise to a peak, then phase out as income continues to climb. The exact income range where it phases out depends on filing status and number of children. If a raise pushes your income into the phaseout range, the credit begins to decrease. The Child Tax Credit and other income-sensitive credits follow similar logic. The raise goes up. The paycheck goes up modestly after withholding. The refund in April comes in smaller than the year before. The household was counting on that refund. Now it is smaller and nobody explained why.

This is not unavoidable in all cases. Pre-tax 401k contributions and HSA contributions reduce adjusted gross income, which is what the EITC calculation uses. If a raise threatens to push you into the EITC phaseout range, increasing pre-tax contributions can keep your AGI lower and preserve more of the credit. That is a real strategy. It is also one that financial advisors charge for, which means the people who need it most are rarely the ones who access it. Now you have it for free.

The Stacking Problem Nobody Tells You About

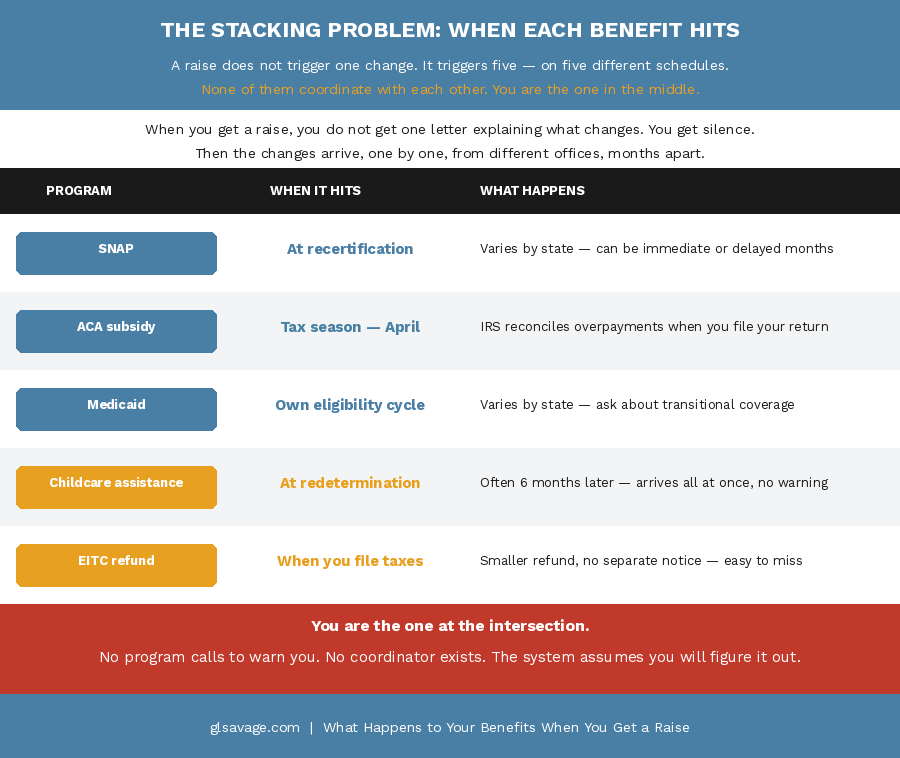

One program adjusting is manageable. Four adjusting at the same time is not, and that is exactly what can happen when a raise crosses multiple thresholds in the same income window. The system does not evaluate your life as a whole. Each program recalculates independently, from inside its own silo, on its own timeline, using its own rules. SNAP changes at recertification. The Marketplace reconciles at tax time. Medicaid has its own eligibility cycle. Childcare assistance has its own redetermination schedule. The EITC adjusts when you file. None of them coordinate with each other. You are the one at the intersection where all of them converge, trying to absorb changes arriving from different directions on different schedules with no warning about any of them.

A 2025 report from Washington University in St. Louis found that nearly one in four public assistance recipients, 22 percent, had taken at least one negative action to avoid triggering a benefit cliff, including turning down a raise, working fewer hours, or declining a job offer. That is not a small number of people making irrational choices. That is a large number of people responding rationally to a system that has already shown them what happens when income crosses the wrong line. The Poverty Premium Explained: How to Fight Back covers the broader structure that makes this pattern show up across housing, insurance, food, and credit too.

What to Do Before the Raise Starts Rearranging Everything

The first move is information. Before the raise kicks in, you need to know specifically which programs you are in, what income thresholds apply to your household, and how close the raise puts you to any of them. This is not paranoia. It is the work the system requires you to do because it will not do it for you.

The Atlanta Federal Reserve Bank has built a free suite of tools called CLIFF, which stands for Career Ladder Identifier and Financial Forecaster, specifically to model this problem. The tools show exactly where your benefit thresholds are and what income level would actually improve your overall financial position. Demo versions of the CLIFF Snapshot are publicly viewable on the Atlanta Fed’s CLIFF tool page. The full tool is used through workforce agencies, nonprofits, and benefits counselors, so searching for a CLIFF tool or benefits cliff calculator in your state through your local workforce agency or a community organization may get you access to a counselor who can run your specific numbers. It is the most useful planning resource available for this situation and most people who need it have never heard of it.

If you have Marketplace health insurance with advance premium tax credits, update your income estimate at healthcare.gov as soon as you know the raise amount. Every month the old estimate stays in the system is a month of potential overpayment that becomes a repayment obligation at filing.

If your employer offers a 401k, a traditional IRA, an HSA, or a dependent care FSA, look at what increasing pre-tax contributions would do to your countable income, which is the income figure the program actually uses when it decides what you qualify for. Pre-tax 401k and HSA contributions reduce both AGI and MAGI simultaneously. A $200-a-month increase in 401k contributions reduces your MAGI by $200 a month. That can be the difference between staying below a threshold and crossing it. The money is not gone. It is sitting in a retirement account in your name. It is just not countable income right now.

Check the reporting rules for every program you are in. SNAP has specific timelines for reporting income changes that vary by state. Missing a reporting deadline does not make the income disappear from the calculation. It makes it show up as a retroactive adjustment, which is worse. Ask your caseworker directly: when does this raise need to be reported, and when will the benefit change take effect?

The Pretax Strategy: Lowering Countable Income Without Earning Less

Here is what almost nobody in this situation has been told. Several types of employer-sponsored contributions reduce the income that programs count against you, without reducing what you actually have. A traditional 401k contribution is taken out before taxes are calculated, which means it reduces your reported income. An HSA contribution through payroll is excluded from federal income tax, state income tax in most states, and Social Security and Medicare taxes, making it one of the most tax-efficient accounts available. A dependent care FSA reduces both your taxable income and your MAGI.

If a raise is going to push you $200 a month over an important threshold, and your employer offers a 401k, you may be able to contribute $200 a month more to that account and keep your countable income right where it was. Your actual financial position improves because you are building retirement savings. The programs do not see the raise because the contribution offsets it in the income calculation. This is not gaming the system. It is using the system as it was designed to be used. The problem is that the people who most need this strategy are the least likely to have access to someone who would walk them through it. The 2026 401k contribution limit is $23,500. The 2026 IRA contribution limit is $7,000, or $8,000 if you are 50 or older. The 2026 HSA limits are $4,400 for self-only and $8,750 for family coverage. If your employer does not offer a 401k, a traditional IRA contribution is deductible from adjusted gross income for people below certain income limits and works similarly for these calculations.

A Raise Should Feel Like Progress. The System Makes That Harder Than It Should.

The benefit cliff is not the result of one bad policy decision. It is the accumulated result of dozens of programs built separately over decades, each with its own income rules and thresholds, none of them designed to coordinate with the others. Atlanta Federal Reserve research tracked a hypothetical single mother advancing from certified nursing assistant to licensed practical nurse to registered nurse. After each certification upgrade she received higher wages but experienced an overall loss in total resources due to taxes and lost benefits. It took eight years for her to see a net benefit from moving up the career ladder. Eight years of working harder and earning more before the math finally worked in her direction. That is the system. You did not design it. But knowing how it works is the only tool available while it stays this way. Build an Emergency Fund Living Paycheck to Paycheck is the next practical step once you have mapped the cliff and know where you actually stand.

Frequently Asked Questions About Benefits and Getting a Raise

Will I lose my benefits if I get a raise?

Not automatically, and not all at once in most cases. What happens depends on which programs you are in, how much your income increases, and how close the raise puts you to each program’s eligibility threshold. SNAP usually reduces gradually rather than cutting off entirely. Medicaid has its own threshold. ACA subsidies reconcile at tax time. Childcare assistance adjusts at redetermination. The risk is not always losing benefits entirely. Sometimes it is losing enough from enough programs at once that the raise barely improves your overall position. The Atlanta Federal Reserve’s CLIFF tools, accessible through the Atlanta Fed’s CLIFF tool page, show your complete picture before the raise starts moving things.

What is a benefit cliff and how does it work?

A benefit cliff is the point at which a raise triggers a loss of assistance that exceeds the financial gain from the higher earnings. It happens because income-based programs use thresholds. Below the line you qualify, above it you do not, or you qualify for less. When multiple programs phase out around the same income level, the combined reduction can be larger than the raise itself. Research from the Atlanta Fed documented one scenario where a $2,000 raise triggered a net loss of $6,000 in total resources when benefit reductions were counted.

Does getting a raise affect my SNAP benefits?

Usually yes, though not always immediately. SNAP benefits decrease by roughly 30 cents for every dollar of net income increase. A raise does not typically eliminate SNAP in one step but it does reduce the benefit amount as countable income rises. The timing depends on your state’s reporting rules and your certification period. You are required to report significant income changes, and missing the reporting deadline can result in retroactive adjustments that are harder to manage than a planned reduction. Ask your state SNAP office specifically when the income change needs to be reported and when the benefit change will take effect.

Can getting a raise make me owe money back on my ACA health insurance?

Yes. If you receive advance premium tax credits through the Marketplace, your subsidy is based on your estimated annual income. If your actual income ends up higher than the estimate, the IRS reconciles the difference when you file your taxes, and you may owe back the excess subsidy received during the year. The fix is to update your income estimate at healthcare.gov as soon as you know about the raise. Updating quickly limits the exposure. Months before you updated it may still be reconciled at filing, but updating immediately stops the overpayment from accumulating further.

Can pretax contributions to a 401k or HSA protect my benefits when I get a raise?

Yes, and this is one of the most underused strategies available. Traditional 401k contributions and HSA contributions through payroll both reduce your Modified Adjusted Gross Income, which is the income figure that ACA subsidy calculations and several other program eligibility rules use. If a raise would push your MAGI over a threshold, increasing pre-tax contributions by a corresponding amount can keep your countable income at the same level, preserving your subsidy or eligibility, while still building your actual financial position. The 2026 HSA limits are $4,400 for self-only and $8,750 for family coverage. The 2026 401k contribution limit is $23,500.

What happens to Medicaid if my income goes up from a raise?

Medicaid eligibility is income-based and varies by state and eligibility category. A raise can push someone above the threshold for their category, ending Medicaid coverage. Medicaid typically costs very little, while Marketplace coverage comes with premiums, deductibles, and out-of-pocket costs that can exceed what the raise provides. Some states offer transitional Medicaid coverage for a period after income rises above the threshold. There is also a new layer to understand: the One Big Beautiful Bill signed July 2025 introduced work requirements of 80 hours per month for Medicaid expansion enrollees starting January 1, 2027, and moved renewals from annual to every six months starting late 2026. People who lose Medicaid due to work requirement violations are specifically barred from ACA Marketplace premium tax credits under the new law. Contact your state Medicaid office and ask about transitional coverage options, the exact income level that triggers a change, and what the work requirement rules mean for your specific situation.

Should I turn down a raise to keep my benefits?

Not without running the full math first. For most people, a raise still results in a net improvement even after benefit reductions, especially if the raise is substantial. But for households close to a cliff in multiple programs simultaneously, the math can genuinely work against acceptance in the short term. Use the Atlanta Fed’s CLIFF tools to see your complete picture, look at whether pre-tax contributions could offset the income increase, and understand the timeline over which the raise becomes a net positive. Turning down money is rarely the right answer, but making an informed decision before it happens is always better than being surprised by the consequences after.

How does a raise affect the Earned Income Tax Credit?

The EITC increases as earnings rise to a peak, then phases out as income continues to climb. If a raise pushes your income into the phaseout range, the credit you receive when you file will be smaller than in prior years. This shows up as a smaller refund rather than a bill, which feels different but is still a real reduction. Pre-tax 401k contributions and HSA contributions reduce adjusted gross income, which is what the EITC calculation uses. Increasing those contributions when income rises can partially or fully protect the credit depending on how close you are to the phaseout range.

Is there a free tool to see how a raise affects all my benefits at once?

Yes. The Atlanta Federal Reserve Bank’s CLIFF tools are designed specifically for this analysis. Demo versions of the CLIFF Snapshot are publicly viewable on the Atlanta Fed’s CLIFF tool page. The full tool is used through workforce agencies, nonprofits, and benefits counselors. Searching for a CLIFF tool or benefits cliff calculator through your local workforce development office, a community action agency, or a financial coaching nonprofit may connect you with a counselor who can run your specific numbers. It is the most useful planning resource available for this situation.