The threat works because most people have no idea what is actually legal. A collector calls, raises their voice, says something about law enforcement, mentions arrest, and suddenly the fear takes over. People pay debts they do not owe. They agree to arrangements they cannot sustain. They hand over money to people running outright scams. The threat of jail is the single most powerful weapon in the debt collection industry, and it is almost always illegal to use it. This article is about what can actually happen to you when you owe money, what cannot happen no matter what anyone tells you, and what to do when someone crosses the line.

The Short Answer: No, You Cannot Go to Jail for Owing Money

The United States abolished debtor’s prisons in 1833. Before that, people were routinely locked up for failing to pay what they owed. Several signatories to the Declaration of Independence had debt problems serious enough to cause legal trouble. The system was eventually recognized as cruel and counterproductive, and federal law eliminated it. No state has a debtor’s prison today.

So can you go to jail for debt? No. You cannot be arrested or jailed for failing to pay a credit card bill, a medical debt, a personal loan, a payday loan, a utility bill, or most other consumer debts. These are civil debts. Not paying them is not a crime. A creditor cannot call the police on you. Law enforcement has no role in collecting a civil debt. If someone claiming to be a collector tells you otherwise, they are either lying to you or running a scam. Both of those things are illegal.

What a creditor can do is sue you. That is the legal path available for collecting a civil debt. A lawsuit is not the same as a criminal charge. It does not involve the police, prosecutors, or jail. It involves a judge, a courtroom, and a process that takes time and gives you opportunities to respond. Understanding that process is what this article is really about, because the process does have teeth, and the teeth are real, even if jail for the debt itself is not.

When a Debt Collector Threatens Jail, They Are Breaking Federal Law

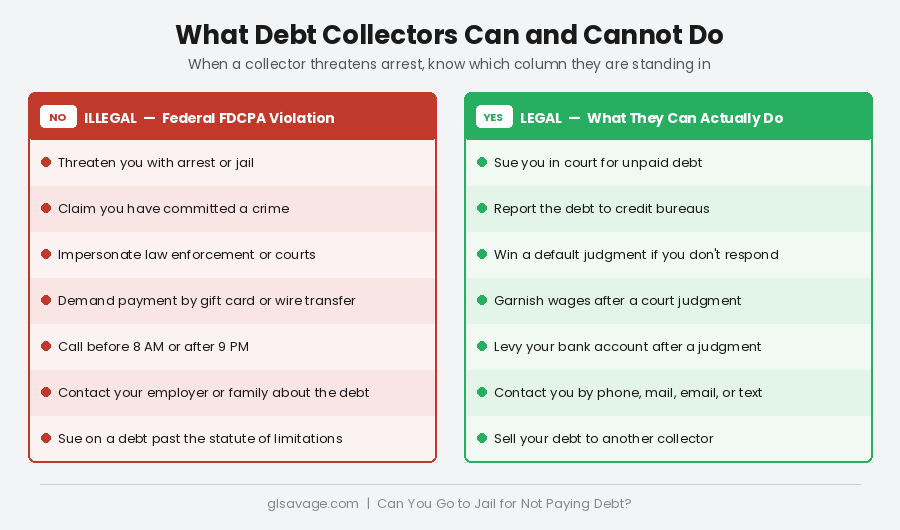

Here is the part most articles skip. When a debt collector threatens you with arrest or jail to pressure you into paying a consumer debt, that is not just an aggressive tactic. It is a federal violation of the Fair Debt Collection Practices Act, specifically Section 807, which prohibits false representations of what can legally happen to you as a result of not paying a debt.

The Fair Debt Collection Practices Act, usually shortened to FDCPA, is the federal law that governs how third-party debt collectors must behave. It covers collection agencies, debt buyers who purchased your account, and law firms that collect debts. The FDCPA explicitly prohibits threatening to have you arrested for a civil debt, falsely implying that you have committed a crime, and misrepresenting what legal consequences you face. Threatening jail for an unpaid credit card or medical bill hits all three of those.

Here is what that means in practical terms. When a collector makes that threat, you do not just have a defense. You have a claim. You can sue that collector in state or federal court. If you win, the court can award you up to $1,000 in statutory damages even if you cannot prove specific financial harm, plus reimbursement for your attorney fees and any actual damages you suffered. Consumer law attorneys who handle FDCPA cases almost always work on contingency, meaning you pay nothing unless they win. The collector’s illegal threat just handed you a potential case.

You have one year from the date of the violation to file. Do not wait. Document everything now.

If the Caller Claims to Be Law Enforcement, That Is a Scam

There is a specific version of the jail threat that goes further than illegal debt collection tactics. It crosses into criminal fraud. Callers who claim to be from a sheriff’s office, a court, a government agency, or law enforcement, and who say you will be arrested unless you pay immediately, are almost certainly running a scam. Impersonating a government official or law enforcement officer is a federal crime entirely separate from the FDCPA violation.

These scams are sophisticated. Callers use real government agency names. They have badge numbers. They know your address. They create urgency, saying arrest is happening today, this afternoon, in the next hour, unless you pay right now by wire transfer, gift card, or cryptocurrency. Those payment methods are the clearest signal that something is a scam. No legitimate court process demands payment by gift card. No sheriff’s office collects debts over the phone.

If you receive a call like this, do not pay anything and do not give out any personal or financial information. Write down every detail you can: the phone number, the name they gave, the agency they claimed to represent, the exact wording of the threat, the time and date. Then report it to the Federal Trade Commission at ReportFraud.ftc.gov and to your state attorney general’s office. These reports matter. They build the case record that allows agencies to pursue the people running these operations.

What Can Actually Happen When You Do Not Pay a Civil Debt

No jail for the debt itself. But the consequences of not paying are real and worth understanding clearly. When you stop paying a consumer debt, here is what the creditor’s actual legal options look like.

The creditor can sell the debt to a collection agency. That agency will contact you, report the delinquency to the credit bureaus, and attempt to collect. Your credit score takes a significant hit. That hit stays on your credit report for seven years.

From there, the creditor or collection agency can sue you in court. This is where most people make the mistake that costs them the most. When you receive court papers, you have a deadline to respond, typically 20 to 30 days depending on your state. If you do not respond, the court enters a default judgment against you. You automatically lose. The creditor wins without ever having to prove their claim in front of a judge, simply because you were not there to contest it. That default judgment then unlocks collection tools including wage garnishment and bank account levies. If you are facing a debt lawsuit right now, Wage Garnishment: How It Works and How to Stop It covers exactly what comes next and what you can still do.

After a judgment is entered, the creditor can garnish your wages, meaning your employer is ordered to send part of your paycheck directly to the creditor. They can also levy your bank account, freezing the funds and taking what they need. They can place a lien on property you own. None of this involves arrest. All of it involves money leaving your control without your agreement.

The Scenario Where Jail Actually Becomes Possible

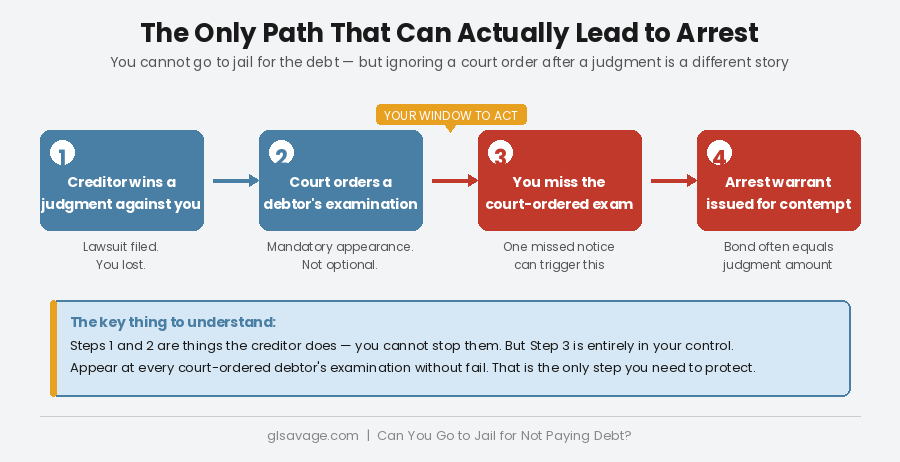

Now here is the detail most articles get wrong, and it has real consequences for real people. You cannot go to jail for the debt. You can go to jail for ignoring a court order related to the debt. That distinction is real.

After a creditor wins a judgment against you, they have a specific legal tool available in most states called a debtor’s examination, sometimes also called a judgment debtor exam. This is a court-ordered proceeding where you are required to appear and answer questions under oath about your finances: your income, your bank accounts, your assets, anything the creditor could use to collect what you owe.

A debtor’s examination is not optional once it is ordered. This is the critical difference between the original lawsuit and the post-judgment process. You could ignore the original lawsuit and not show up. You should not have, but you legally could, and you would simply lose by default. A debtor’s examination is different. Once a judge issues an order requiring you to appear, that order must be obeyed. It is a court order, not a request. Ignoring a court order is contempt of court, and contempt of court can result in a warrant for your arrest.

To be precise about what happens: if you miss a court-ordered debtor’s examination without a valid reason, the creditor can go back to court and request a contempt finding. The court may then issue what is called a bench warrant, or in some states a capias or body attachment. These are arrest warrants. Law enforcement can pick you up and hold you in custody until you appear before the judge. In some states, the bond amount to get out is set equal to the judgment amount, which means you could remain in custody if you cannot pay it.

You are not in jail for the debt. You are in jail for ignoring the court. But the effect is the same.

The Repeat Exam Trap Creditors Use

Here is something no other article covering this topic explains, and it is one of the most predatory post-judgment collection tactics in use today.

In many states, creditors can request debtor’s examinations repeatedly. Some creditors, particularly subprime lenders and payday loan companies, schedule these examinations over and over, sometimes as frequently as once a month, with one specific goal: waiting for you to miss one. Your life is complicated. You have work, children, medical appointments, transportation problems. One missed notice, one scheduling conflict, one piece of mail that did not arrive, and you have missed a court-ordered appearance. The creditor gets the contempt finding. The arrest warrant issues.

This is a documented practice. It is legal in most states. It is deliberately designed to use the court system as leverage against people who have no money to pay the debt anyway. If you are being subjected to repeated debtor’s examination orders, talk to a consumer law attorney or legal aid organization immediately. Some states have laws that require the creditor to show your financial circumstances have changed before they can bring you back on the same issue. You may have more protection than the creditor wants you to know about.

Child Support and Taxes: The Real Exceptions

Two categories of debt operate under completely different rules, and they are worth understanding clearly.

Unpaid child support is a court order, not just a debt. When a judge orders you to pay child support and you do not, you are violating a direct court order. That is contempt of court from the start, without needing the additional steps of a civil lawsuit and debtor’s examination. Courts take child support violations seriously. Jail time for willful nonpayment of child support is a real outcome in every state. The key word is willful. If you genuinely cannot pay because your circumstances have changed, you need to go back to court and ask for a modification before you stop paying, not after. Stopping payments without court approval and then explaining your hardship later is treated very differently than proactively addressing a change in circumstances.

Federal tax debt is also different. Not paying your taxes is handled by the IRS as a civil matter first, through liens, levies, and wage garnishment, none of which involve jail. However, willful tax evasion and tax fraud are criminal offenses. If the government can show you deliberately hid income, filed false returns, or took deliberate steps to avoid paying what you owe, criminal prosecution and prison time are possibilities. Simply being unable to pay taxes you legitimately owe, while owing and unpleasant, is not criminal. The IRS wants money, not prisoners, and offers payment plans and hardship programs for that reason. Contacting the IRS directly about your situation is almost always better than avoiding them.

What to Do When a Collector Threatens Arrest

The first thing to know: nothing about the way legitimate legal processes work requires you to pay right now, over the phone, before the end of the day. Urgency is a tactic. Real legal proceedings have timelines measured in weeks and months, not hours. Do not pay under pressure in the moment.

Document everything immediately. Write down the date and time. The phone number that called you. Every name they gave, every company they mentioned, every agency they claimed to represent. Write down their exact words, as close to verbatim as you can. If your state allows one-party recording of phone calls, and most do, record any subsequent calls. This documentation is the foundation of any legal action you take.

Do not give out any personal information. Bank account numbers, Social Security numbers, payment card numbers. Nothing. A legitimate collector already has enough information to have contacted you. A scammer needs you to supply the rest.

Verify whether the debt is real. Request written verification of the debt. Under the FDCPA, a debt collector must send you a validation notice within five days of first contacting you, and they must provide written verification if you request it within 30 days of receiving that notice. If the debt is real, find out the original creditor, the amount, and when the last payment was made. That last date matters for the statute of limitations.

Contact a consumer law attorney. FDCPA cases are the kind consumer lawyers take on contingency because the law makes the collector pay the fees when the consumer wins. Finding one costs you nothing upfront. The National Association of Consumer Advocates at consumeradvocates.org has a directory of attorneys who handle exactly this type of case. You can also file a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov/complaint and with the Federal Trade Commission at ReportFraud.ftc.gov.

The debt collection industry built the threat of jail because it works. It works on people who do not know the law. It stops working the moment you do. If you are dealing with debt collectors right now, The Debt Collector Is Not Who You Think It Is covers the full picture of who is actually calling and what authority they actually have.

Frequently Asked Questions About Jail and Debt

Can you go to jail for not paying credit card debt?

No. You cannot be arrested or jailed for failing to pay a credit card debt. Credit card debt is a civil matter. A creditor can sue you, win a judgment, and use that judgment to garnish your wages or levy your bank account. None of that involves law enforcement or arrest. If a debt collector tells you that you can go to jail for not paying a credit card bill, they are breaking federal law under the Fair Debt Collection Practices Act and you can sue them for it.

Can debt collectors have you arrested?

No. Debt collectors have no authority to arrest anyone. They cannot call the police on you. They cannot have a warrant issued for you over an unpaid bill. If a collector claims they can have you arrested, or threatens to call law enforcement to collect a consumer debt, that is an FDCPA violation. Document it, do not pay under that pressure, and contact a consumer law attorney. You may be owed up to $1,000 in statutory damages plus attorney fees.

Is threatening jail to collect a debt illegal?

Yes. Threatening arrest or jail to collect a consumer debt is explicitly prohibited by the Fair Debt Collection Practices Act under Section 807. It constitutes a false representation of what can legally happen to you as a result of not paying. This applies to collection agencies, debt buyers, and law firms collecting debts. It does not apply to original creditors calling about their own accounts, who are not covered by the FDCPA, though many states have their own laws that extend similar protections.

What is a debtor’s examination and can it lead to arrest?

A debtor’s examination is a court-ordered proceeding after a creditor has won a judgment against you. You are required to appear and answer questions under oath about your income and assets so the creditor can determine how to collect. Unlike the original lawsuit, this appearance is mandatory once the court orders it. If you ignore a court-ordered debtor’s examination, the creditor can ask the court to find you in contempt, which can result in an arrest warrant. You are not being arrested for the debt. You are being arrested for disobeying the court. The distinction matters legally but the result is the same. Never ignore a court order related to a debt.

Can you go to jail for not paying medical debt?

No. Medical debt is a civil debt like any other consumer debt. You cannot be jailed for failing to pay a hospital bill, a doctor bill, or any other medical expense. A medical creditor can sue you, obtain a judgment, and pursue garnishment or bank levies. They cannot have you arrested. Threatening jail to collect medical debt is the same FDCPA violation as threatening jail for any other consumer debt.

Can you go to jail for not paying a payday loan?

No. Payday loans are civil debts. You cannot be arrested for not paying one. Payday lenders have a particularly well-documented history of threatening arrest, claiming that writing a check that bounced is check fraud, or implying criminal charges are coming. These are illegal tactics. Bouncing a check because you did not have funds is a civil matter in most circumstances, not a criminal one, and payday lenders threatening criminal prosecution for a bad check related to a loan are violating the FDCPA. If a payday lender has made these threats, document them and contact a consumer law attorney immediately.

What debts can actually lead to jail?

Unpaid child support, when a court order to pay exists and the nonpayment is willful, can lead to jail for contempt of court in every state. Willful federal tax evasion and tax fraud are criminal offenses that can result in prosecution and imprisonment. Failing to comply with any direct court order related to a debt, such as ignoring a required debtor’s examination, can lead to arrest for contempt. In all of these cases, the imprisonment is for violating a court order or committing a crime, not for the debt itself.

What should I do if a debt collector threatens me with jail?

Do not pay under that pressure. Write down everything: the date, time, number that called, name of the caller, company they claimed to represent, and their exact words. Do not give out any personal or financial information. Request written verification of the debt. Contact a consumer law attorney, many of whom take FDCPA cases at no upfront cost. File a complaint with the CFPB at consumerfinance.gov/complaint and with the FTC at ReportFraud.ftc.gov. The threat itself may be your strongest leverage in settling or eliminating the debt.

Does filing for bankruptcy stop a debtor’s examination?

Yes. Filing for bankruptcy triggers an automatic stay, which is an immediate legal halt on all collection activity. This includes debtor’s examinations. Once you file, a scheduled examination cannot proceed, and the creditor cannot request your arrest for missing it while the stay is in effect. If you are facing repeat debtor’s examinations and are considering bankruptcy, talk to a bankruptcy attorney before your next scheduled appearance. Many offer free consultations.