The call comes in. Someone says you owe money. Your stomach drops and your first instinct is to figure out how to pay them. Knowing what to do when a debt collector calls, and understanding who is actually on the other end of that line, changes everything. Because the debt collector on the phone is almost certainly not the company you originally borrowed from. They are more likely a company that purchased your debt like a commodity, paid a fraction of what you owe, and is now legally entitled to collect the full amount while being under no obligation to tell you any of that. The debt collection industry runs on one assumption: that you do not know how it works. This article is going to fix that.

When a debt collector calls, do not pay on the first contact. Write down the company name, the amount they claim you owe, and a callback number. Then verify the debt on your credit report, check the statute of limitations for your state, and send a debt validation letter by certified mail before any money changes hands.

Your Debt Was Probably Sold. Here Is What That Means.

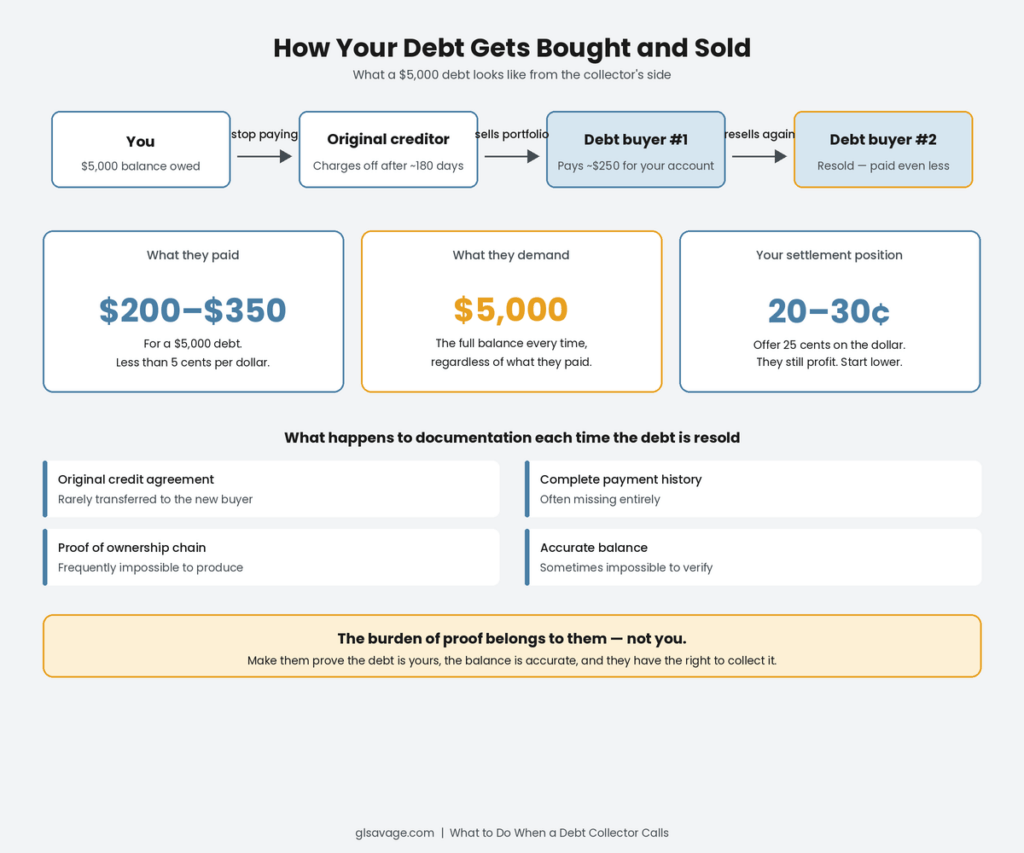

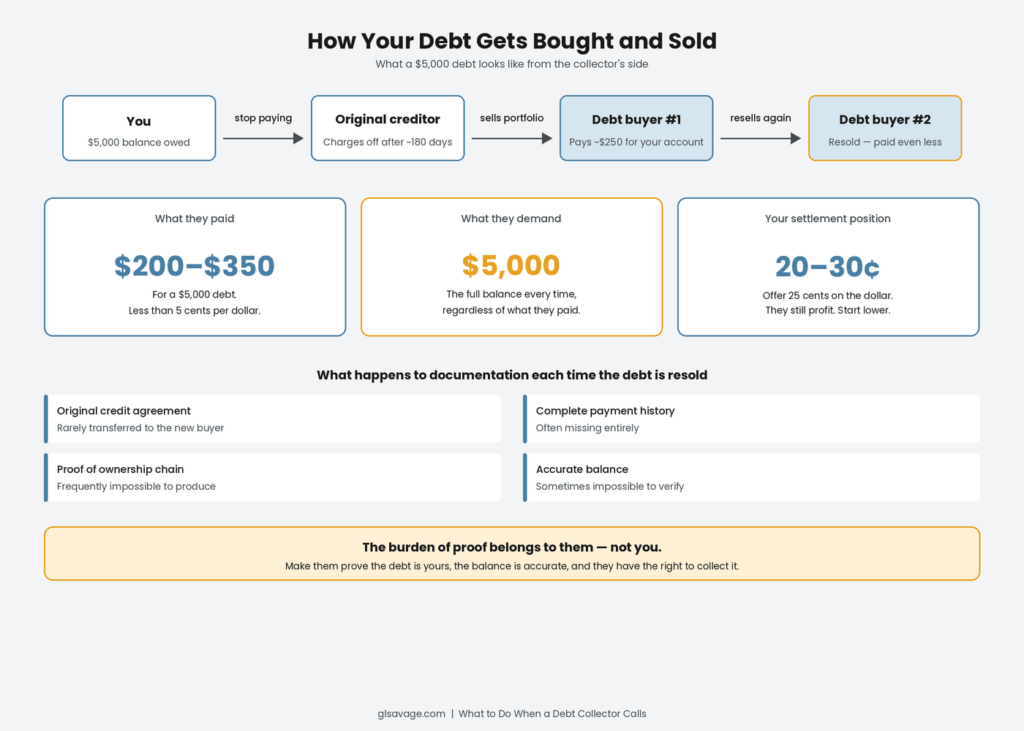

When you stop paying a debt, the original creditor, the bank or credit card company you actually borrowed from, does not chase you forever. After a certain point, usually around 120 to 180 days of nonpayment, they write it off as a loss on their books. This is called a charge-off. It sounds like the debt disappears. It does not. The charge-off also gets reported to the credit bureaus, where it damages your credit score and stays on your report for up to seven years, regardless of whether the debt is later paid or settled. The creditor takes a tax benefit for the loss and then sells the account, often bundled with thousands of other defaulted accounts, to a debt buyer for a fraction of what you owe.

How much of a fraction? The numbers are not hidden, but the industry does not advertise them. Debt buyers routinely pay less than five cents for every dollar of debt they purchase. Credit card debt typically sells for four to seven cents on the dollar. Older debt that has already been through one or more collection attempts can go for less than a penny. The largest debt buying companies purchase portfolios containing millions of accounts at an average of around four to five cents on the dollar.

What that means in plain terms: if you owe $5,000 and your account was sold, the company calling you today may have paid somewhere between $200 and $350 for the right to collect that full $5,000. That is the actual negotiation that happens when a debt collector calls, and most people are not aware of it going in.

Who You Are Actually Talking To Determines What You Can Do About It

The phrase “debt collector” covers three completely different kinds of companies. Your legal rights are not the same with all of them. Most people never find out which one is calling. The industry does not disclose it.

If the company calling you still works for the bank or credit card company you originally borrowed from, that is an in-house collector. Here is what most guides skip: the main federal law that protects you from abusive debt collection, the Fair Debt Collection Practices Act, the FDCPA, generally does not apply to the original creditor collecting its own debt. Chase calling you about your Chase account is largely outside those protections. The law was written to regulate third parties, not the original lender. Some states have passed their own laws to fill that gap. Federally, if it is the original creditor on the line, your options are more limited than people assume.

If an outside company is calling on behalf of the original creditor, without having purchased the debt, that is a third-party collection agency. They earn a percentage of what they collect and pass the rest back. They do not own your debt. The FDCPA applies, and you have the full set of federal protections.

If the company calling you purchased your account outright, that is a debt buyer. They own it. They paid pennies for it. They are not collecting for anyone else. They keep everything they collect. This is who most people are dealing with by the time a stranger calls about an old account. Knowing that going in changes every conversation.

Your Debt Can Be Resold. Multiple Times. With Fewer Records Each Time.

A debt buyer who cannot collect does not necessarily give up. They sell the account to another debt buyer, who may sell it again. Your original $5,000 credit card debt can pass through three or four different companies over several years. Every time it changes hands, the documentation gets thinner. The new buyer typically receives an electronic file with basic account information: your name, an account number, and a balance. They rarely receive the original credit agreement, a complete payment history, or any documentation that independently proves the amount is accurate.

This is how a collector ends up calling about a debt you paid off years ago. Or a debt that belonged to someone else with a similar name. Or a balance that is wrong. Human Rights Watch has documented debt buyers winning court judgments against the wrong people, for incorrect amounts, on debts that were legally unenforceable. This is not fringe behavior. It is a documented feature of how accounts are bought and sold at scale.

None of this means every collector is operating in bad faith. A lot of the debt being collected is real, owed, and within the statute of limitations. But you have no way to know that from a phone call. The burden of proving what you owe, to whom, and that they have the right to collect it belongs entirely to them. Not to you.

Zombie Debt Is Real and One Wrong Move Brings It Back to Life

Some collectors are not calling about a debt you currently owe. They are calling about a debt that is legally dead. Paid off years ago but the records did not survive the resale chain. Past the statute of limitations, meaning no court will enforce it. Discharged in bankruptcy. Or belonging to someone else entirely. These accounts are purchased for almost nothing specifically because they cannot be legally enforced.

Here is the trap: in most states, making a payment on a debt past the statute of limitations restarts the clock. A single payment of $25 on a balance you have no legal obligation to pay can revive it completely and give the collector fresh grounds to sue you for the full amount. A written acknowledgment of the debt, such as an email or a letter where you admit you owe it, can do the same thing in many states. A casual phone call where you confirm the debt exists is less likely to restart the clock in most jurisdictions, but certain states treat an oral promise to pay as legally binding. The safest position is to say nothing and write nothing until you know exactly where you stand.

The FTC has received more than 77,000 reports in a single year of collectors using abusive or threatening tactics or attempting to collect money not actually owed. Some collectors are pursuing accounts that are expired. Before you say anything to a collector about an old debt, find out when the last payment was made and look up the statute of limitations for that type of debt in your state. Those two pieces of information tell you whether the debt is legally collectible at all.

Can a Debt Collector Sue You?

Yes, a debt collector can sue you. And the strategy that produces wins does not require them to prove much of anything. That is the part nobody explains.

Debt buyers file lawsuits by the thousands. Not because they plan to go to trial. Because they expect you not to respond. When someone is sued for a debt and does not file a written answer with the court within the deadline, the judge enters a default judgment automatically. No evidence required. No proof that the collector actually owns the debt. No documentation showing the balance is accurate. You did not respond, so the court assumes everything in the complaint is true and rules against you.

Studies across multiple states consistently show that more than 70 percent of debt collection lawsuits end in default judgments. In some courts the rate reaches 95 percent of cases that go to judgment. File thousands of suits. Most people ignore them. Collect on the judgments. A default judgment allows wage garnishment, frozen bank accounts, and property liens. And because debt buyers often wait until close to the end of the statute of limitations before filing, a high-interest debt has frequently been accumulating the entire time. Human Rights Watch documented that a $2,000 debt at 25 percent interest grows past $6,000 if a collector waits five years before suing.

When people do respond, debt buyers often cannot win. The original credit agreement is frequently missing. Ownership of the account, meaning a documented paper trail from the original creditor to the current collector, often cannot be proved. The balance itself is sometimes impossible to verify. Consumer rights attorneys report that simply having legal representation on the defendant’s side regularly leads to the case being dropped. Filing a written answer is all it takes to change the math.

If a collector sues you, respond in writing within your state’s deadline. That window is typically 14 to 35 days from when you were served. Legal aid organizations in most areas handle debt collection cases at low or no cost. Many consumer rights attorneys take these on contingency, meaning you pay nothing unless you win.

What Rights Do You Have When a Debt Collector Calls?

Congress passed a law in 1977 giving people specific, enforceable power over debt collectors. Most people being collected on right now have never heard of it. That gap between what the law allows and what people know they can do is significant.

Within 30 days of a debt collector first contacting you, you can send a written request demanding they validate the debt. Validation requires them to send you written proof of the amount owed, the name of the original creditor, and evidence they have the legal right to collect it. Once you send that letter within the 30-day window, all collection activity must stop until they provide verification. If they cannot verify it, they cannot legally continue collecting or report the debt to the credit bureaus. You can still send a validation request after 30 days, but the automatic cease-collection requirement no longer applies.

You can also send a written cease contact letter at any point. This is exactly what it sounds like: a letter telling them to stop contacting you. Once they receive it, they can only reach out to confirm they are stopping or to notify you of specific legal action. The calls stop. The debt does not disappear, but the contact does.

The FDCPA also prohibits collectors from calling before 8 a.m. or after 9 p.m., contacting your workplace if you tell them your employer does not allow personal calls, calling more than seven times in a seven-day period about a single debt, threatening legal action they do not actually intend to take, and impersonating attorneys or government officials. Each documented violation gives you grounds to sue in federal court. You can recover actual damages plus up to $1,000 per violation in additional penalties plus attorney’s fees, which the collector pays.

These are not loopholes. They are the law. Send the debt validation letter and any cease contact request by certified mail with return receipt. That paper trail is what makes the violation provable. The CFPB provides sample letters you can use as a starting point.

The Negotiation Position Nobody Tells You About

If the debt is legitimate, within the statute of limitations, and you are dealing with a debt buyer, your negotiating position is stronger than the opening call suggests.

A debt buyer who paid four to seven cents on the dollar for your account can settle for 20 or 30 cents on the dollar and still come out ahead. If you offer 25 percent of the balance on a $5,000 account, you are offering $1,250 on a debt they may have paid $250 to acquire. That is a profit for them. They may counter. Start lower than you expect them to accept and negotiate from there.

Get everything in writing before a single dollar moves. The settlement agreement must state the specific dollar amount being paid, confirm that amount satisfies the debt in full, and ideally confirm they will update the credit bureaus to reflect the settlement. A verbal agreement to settle means nothing if the balance later reappears on your credit report or gets sold again to another buyer.

If you are dealing with the original creditor or a third-party agency collecting on their behalf, the math is different. For them, anything short of the full balance is a loss. You still have room to negotiate, particularly if you are offering a lump sum, but you are not in the same position as you would be with a buyer who purchased the debt at a steep discount. Know who you are talking to before you name a number.

The Tax Bill Nobody Warns You About

People settle debt, feel relief, and then get blindsided the following April. The IRS considers forgiven debt income.

If you owe $5,000 and settle for $1,500, the $3,500 the collector wrote off is added to your taxable income for that year. The collector is required to send you a Form 1099-C, Cancellation of Debt, for any forgiven amount of $600 or more. That amount gets reported to the IRS the same way wages do.

Two situations let you avoid that tax hit. If your total debts exceeded your total assets at the time of the settlement, the IRS considers you insolvent and you can exclude the forgiven amount from taxable income by filing Form 982. Debt discharged in bankruptcy is also excluded. Neither exclusion is automatic. You have to claim it. If you do not know it exists, you pay taxes on money you never actually received.

The practical number: settle $10,000 in debt in the 22 percent tax bracket and you could owe $2,200 in additional federal taxes that year. Factor that into the calculation before you agree to anything. If the numbers are complicated, talk to a tax professional before you settle.

What to Do When a Debt Collector Calls

Do not pay on the first call. Do not confirm information you are not certain they already have. Write down the company name, the collector’s name, a callback number, and what they claim you owe. Then get off the phone and do your homework before the next conversation.

Pull your credit reports at AnnualCreditReport.com. All three bureaus are required to give you a free one. If the debt is real and in collections, it will be on your report with the collector’s name attached. If what the caller described does not appear anywhere on your credit reports, that is a significant red flag. Do not pay anything until you understand the discrepancy.

Look up the statute of limitations for that type of debt in your state before you say another word to them. Find out when the last payment was made. If that date is past the window, the debt is time-barred. They cannot sue you for it. Do not make a payment, do not acknowledge the debt in writing, and do not make any promises until you know exactly where you stand legally.

Send a debt validation letter by certified mail with return receipt requested. Make them prove the debt is yours, the amount is accurate, and they have the legal right to collect it. Send it within 30 days of first contact to trigger the automatic cease-collection requirement. The CFPB provides a sample letter you can use as your starting point.

If you are sued, respond. An unanswered lawsuit hands them a judgment they may never have been able to earn in court. Legal aid organizations in most areas handle debt collection cases at no cost. Many consumer rights attorneys take these on contingency. Responding costs you nothing. A default judgment can follow you for years.

The burden of proof belongs to them. Most of them are counting on you never asking for it.

For more on what happens to your credit once a debt hits collections, read How Collection Accounts Affect Your Credit Report. And if minimum payments never seem to shrink your balance, Minimum Payments Keep You in Debt. That Is Not an Accident. explains exactly how that math was designed to work.

Frequently Asked Questions

Almost certainly not. By the time a third-party collector contacts you, your original creditor has either hired an outside agency or sold your account to a debt buyer. The company calling may have no prior relationship with you and likely paid pennies on the dollar for the right to collect your account.

A debt collector is typically hired to collect on behalf of another company and earns a percentage of what they recover. A debt buyer purchases delinquent accounts outright for a fraction of the balance, often less than five cents per dollar, and keeps everything they collect. Because debt buyers paid so little, they have far more room to settle for less than the full balance and still profit.

A debt validation letter is a written request demanding the collector prove the debt is yours, confirm the balance, and show they have the legal right to collect it. Send it within 30 days of first contact by certified mail with return receipt. During that window, all collection activity must stop until they provide written verification. If they cannot verify it, they cannot legally continue collecting or report the debt to the credit bureaus.

Zombie debt is debt that is past the statute of limitations, already paid, or discharged in bankruptcy. Collectors cannot sue you for time-barred debt. Be careful: making even a small payment or sending a written acknowledgment of the debt can restart the statute of limitations in many states, giving the collector fresh legal grounds to sue you for the full amount.

Yes. Debt collectors and debt buyers can file lawsuits, and they do so by the thousands. The key detail: more than 70 percent of debt collection lawsuits end in default judgments, meaning the person sued never responded. If you are served with a lawsuit, respond in writing within the deadline your state sets, typically 14 to 35 days. An unanswered lawsuit becomes a judgment without the collector having to prove the debt is valid.

Yes, especially with debt buyers. Because they bought your account at a steep discount, they can often settle for significantly less than the full balance and still make money. Get a written settlement agreement before making any payment. The agreement must confirm the amount paid satisfies the debt in full. Also account for taxes: forgiven debt of $600 or more is generally treated as taxable income by the IRS.

Legitimate collectors must provide written notice of the debt within five days of first contact, including the original creditor’s name and the amount owed. They cannot demand payment by gift card, wire transfer, or prepaid debit card. They cannot threaten arrest. They cannot call before 8 a.m. or after 9 p.m. If any of these rules are being broken, report it to the FTC at reportfraud.ftc.gov and to the CFPB.

The Fair Debt Collection Practices Act applies to third-party collectors and debt buyers but generally not to original creditors collecting their own debts. It prohibits calls before 8 a.m. or after 9 p.m., more than seven calls in a seven-day period about the same debt, workplace calls if your employer prohibits them, threats of actions not actually intended, and impersonating attorneys or government officials. Each violation gives you the right to sue for actual damages plus up to $1,000 per violation plus attorney’s fees.

Yes. The IRS treats forgiven debt of $600 or more as taxable income. The collector sends a Form 1099-C for the forgiven amount, which you report as income unless you qualify for an exclusion. The two most common exclusions are insolvency, meaning your debts exceeded your assets at the time of settlement, and bankruptcy discharge. File IRS Form 982 to claim either exclusion. Factor the potential tax consequence into any settlement decision before you agree.