The phone rings a few days after someone dies. The caller says they are a debt collector and they need to discuss the account. The family member on the other end, grieving and overwhelmed, does not know what they owe or what the rules are. That is not an accident. The debt collection industry makes money from that gap in knowledge. Debt after death is one of the most misunderstood areas in personal finance, and the misunderstanding costs families real money at the worst possible time. Most of what you owe does not pass to your family when you die. But what does happen to it matters enormously, and there are specific situations where people do end up on the hook. Knowing which situation you are in before the call comes is the difference between protecting what you have and giving it away.

The Basic Rule and Why It Does Not Tell the Full Story

When you die with debt, that debt belongs to your estate. An estate is everything you own at the time of death: bank accounts, property, personal belongings, investments. Before any of that goes to your family, it has to go through a legal process called probate. During probate, your debts get paid first. Creditors file claims against the estate. The estate pays them in a legally determined order. Whatever is left after the creditors are satisfied goes to your heirs.

If the estate does not have enough money to pay all the debts, most of them simply go unpaid. Creditors cannot reach into your family members’ pockets for debts they did not personally sign for. That is the basic rule and it is genuinely protective. Your credit card debt does not become your children’s credit card debt the moment you die.

But the basic rule leaves out several things that matter. It leaves out what happens when creditors have already consumed most of what you owned before your family sees any of it. It leaves out the specific circumstances where family members actually do become responsible. It leaves out the accounts and assets that skip the estate entirely and go directly to the people you named, protected from creditors. And it leaves out what debt collectors are legally allowed to do to your family and what they do anyway.

Creditors Get Paid Before Your Family Does

This is the part that surprises people. The assumption is that you leave your savings to your family and separately your debts get sorted out. That is not how it works. Your savings are part of your estate. Your debts are paid from your estate. If you die with $30,000 in a checking account and $28,000 in credit card debt, the credit card company gets paid first. Your family gets what is left. If the debts exceed the assets, your family gets nothing from those accounts.

The order in which debts get paid during probate is set by state law, but it generally goes: funeral expenses first, then the costs of administering the estate, then taxes, then secured debts like mortgages and car loans, then unsecured debts like credit cards and medical bills. Your family’s inheritance comes last. If the line of creditors is long enough or the debts are large enough, there may be nothing left by the time it reaches your heirs.

This is the part of debt after death that most financial advice skips. A person who spends years building savings while carrying significant debt may leave behind a much smaller inheritance than anyone expected, not because the money disappeared, but because it went to pay creditors before the family ever saw it. If protecting what you leave behind matters to you, understanding how debt interacts with your estate is as important as understanding how to build the estate in the first place.

The Accounts That Skip the Estate Entirely

Most people do not know this next part, and it is the part that matters most.

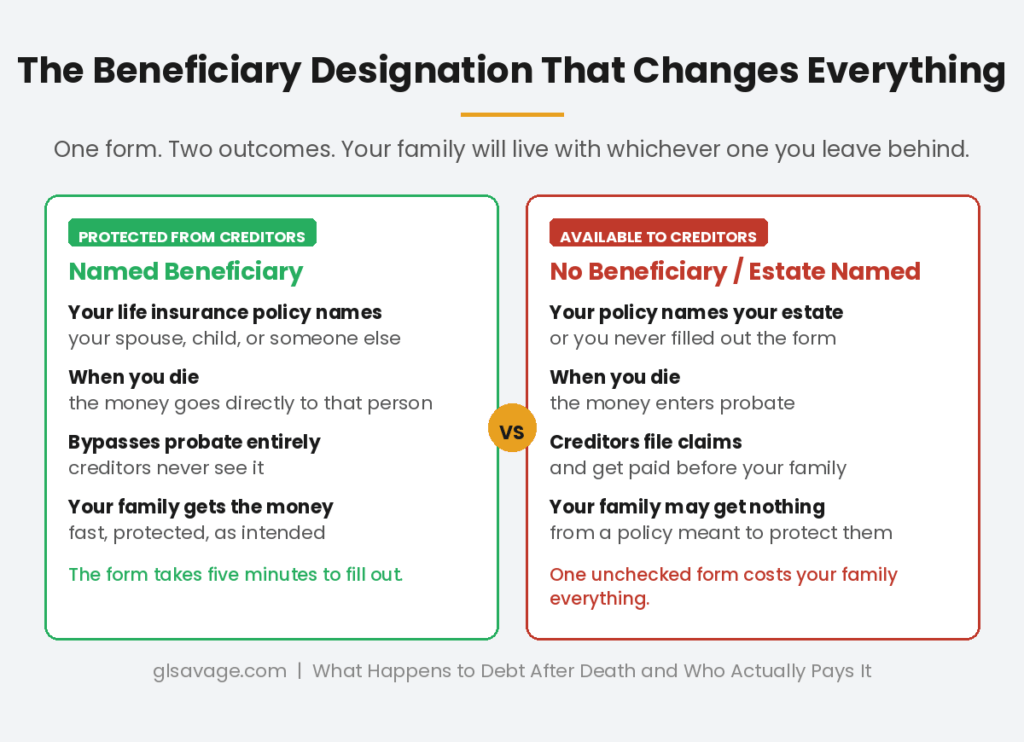

Certain assets do not go through probate at all. Life insurance policies with a named beneficiary pay directly to that person when you die. Retirement accounts like a 401(k) or IRA with a named beneficiary transfer directly to that person. Bank accounts set up as payable-on-death to a named individual pass outside the estate. These assets bypass probate entirely. Because they bypass probate, creditors cannot touch them. The credit card company, the medical billing department, the debt collector, none of them can file a claim against money that never entered the estate.

The catch is one specific detail: the beneficiary has to be a named person, not your estate. If your life insurance policy lists your estate as the beneficiary, or if you never named a beneficiary at all, that money falls into the probate estate and becomes available to creditors. A life insurance payout that was intended to protect your family from your debts becomes the fund that pays those debts instead, because of a form that was never filled out or never updated.

This happens more often than it should. People take out a life insurance policy and never update the beneficiary after a divorce, a death in the family, or a change in circumstance. People open retirement accounts and leave the beneficiary field blank. In both cases, what was meant to protect the family gets pulled into the estate and consumed by the creditors first.

The fix is not complicated. Review your beneficiary designations on every life insurance policy and every retirement account. Make sure a living person is named. Make sure that person is still the right person. This single action is one of the most consequential things you can do to protect your family from your debt after death. You can read more about how assets and credit accounts interact in Payable on Death Accounts: What Banks Don’t Tell You.

Who Actually Does Owe the Debt

The basic rule protects most family members. But there are real exceptions and collectors know exactly who they are.

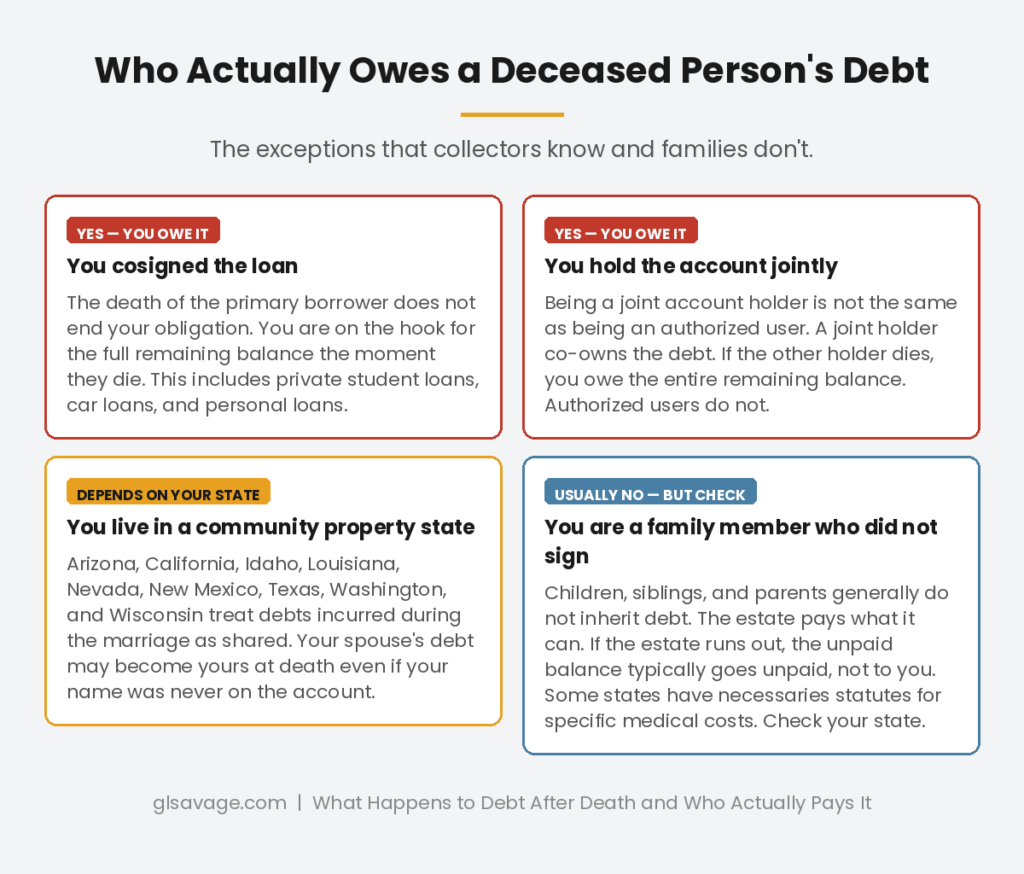

Cosigners are responsible. If someone cosigned a loan with the person who died, they are on the hook for the full remaining balance. The loan agreement said so when they signed it. The death of the primary borrower does not change that obligation. For many families this means a parent or spouse who cosigned a car loan or a student loan suddenly has a debt they were never making payments on and may not have budgeted for.

Joint account holders are responsible. Being a joint account holder is different from being an authorized user. An authorized user can use someone’s credit card but did not agree to be responsible for the balance. A joint account holder is a full co-owner of the account and is equally responsible for everything owed on it. If a credit card is jointly held and one account holder dies, the surviving account holder owes the entire balance.

Community property states work differently. Nine states treat debts incurred during a marriage as shared by both spouses regardless of whose name is on the account: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. If your spouse ran up credit card debt while you were married and you live in one of these states, that debt may be your responsibility after they die, even if your name was never on the account. The rules within community property states vary, and some debts incurred before the marriage or treated as separate property may not transfer, but the general principle is that marital debt is shared debt.

Some states have what are called necessaries statutes, which require surviving spouses and in some cases parents to pay certain types of costs the deceased incurred for essential needs, most commonly medical and nursing home expenses. These laws vary significantly by state and are worth knowing about if you are in a state that has them.

What Debt Collectors Can Do and What They Actually Do

When someone dies, the debt collector’s job does not stop. It shifts. The estate is now the debtor, and collectors have a legal process for filing claims against it. They also have specific rules about how they can contact the family.

Under federal law, the FDCPA treats the surviving spouse, the executor or administrator of the estate, and the parents of a deceased minor as people who can be contacted to discuss the debt, because they may have legal responsibility for it or authority over the estate. Beyond those people, collectors can contact any other family member exactly once, only to ask for the executor’s contact information, and they cannot mention the debt at all during that contact.

What actually happens is often different. Collectors contact grieving family members and create the impression, sometimes explicitly, that the family owes the money and needs to pay immediately. They call multiple times. They suggest that failure to pay will result in serious consequences for people who have no legal obligation to pay anything. The CFPB has documented hundreds of complaints about exactly this type of conduct. It is illegal. And it works often enough that collectors keep doing it.

If a debt collector contacts you about a deceased family member’s debt and you did not cosign, do not hold a joint account, and do not live in a community property state where the debt would apply to you, you are not responsible for that debt. You can tell the collector that, give them the name and contact information of the estate’s executor, and end the call. If they continue contacting you, send a cease contact letter by certified mail. You can also file a complaint with the CFPB at consumerfinance.gov and with the FTC at reportfraud.ftc.gov. The calls and the pressure they create are not evidence that you owe the money. They are a collection tactic.

How Student Loans Are Handled After Death

Federal student loans are discharged when the borrower dies. The surviving family submits proof of death to the loan servicer and the balance is eliminated. This applies to both the Direct Loan program and most other federal loan types. It also applies to Parent PLUS loans, which are discharged if either the parent borrower or the student for whom the loan was taken out dies.

Private student loans are a different story. Some private lenders discharge the loan on death. Many do not. Some private loans have a clause that puts the loan into immediate default when the primary borrower dies, which means the full balance comes due at once and the estate is responsible. If there is a cosigner on a private student loan, which is common because young borrowers often cannot qualify without one, that cosigner becomes responsible for the entire remaining balance when the primary borrower dies. This is not a hypothetical. Families have been hit with five-figure private student loan balances they had no warning was coming, triggered by a death certificate.

If you have cosigned a private student loan for someone, check the loan agreement for what happens on the death of the primary borrower. Some lenders offer cosigner release programs after a certain number of on-time payments. Knowing what you have agreed to before it becomes a crisis is significantly better than discovering it after.

Medical Debt After Death

Medical debt is one of the largest categories of debt people die with. It follows the same basic rules as other unsecured debt: it goes against the estate, gets paid from available assets during probate, and does not automatically transfer to family members who did not sign for it.

There are two exceptions worth knowing. First, in community property states, medical debt incurred during the marriage may be considered a shared debt even if only one spouse received the care. Second, some states have filial responsibility laws, which theoretically require adult children to pay for a parent’s medical or nursing home care. These laws are rarely enforced and the rules vary significantly by state, but they exist, and debt collectors occasionally use them as leverage even in situations where enforcement would be unlikely. If a collector references filial responsibility laws to pressure you, do not pay anything before talking to an attorney who practices in your state.

For more on medical debt specifically, including how it is handled differently from other types of debt, Medical Debt Is Different. Here Is How to Handle It. covers the full picture.

What You Can Do Right Now to Protect Your Family

The debt collection industry counts on families not knowing any of this until the call comes. Here is what to do before and after.

Update your beneficiary designations. Every life insurance policy, every retirement account, every payable-on-death bank account needs a named living beneficiary. Check them now, not after a major life event. The forms take minutes to update and they determine whether those assets are protected from your creditors or consumed by them.

Know what you have cosigned. If your name is on a loan as a cosigner, your obligation does not end if the primary borrower dies. Know which loans you have cosigned and whether the lender offers a cosigner release option.

Understand what joint means. If you share a credit account as a joint holder rather than as an authorized user, you are equally responsible for the full balance. Know which accounts you hold jointly.

Know your state’s rules. If you live in a community property state, understand that debts incurred during the marriage may become your responsibility regardless of whose name is on them. If you are in a state with necessaries statutes, know what those laws cover.

If you are dealing with a debt collector calling about a deceased family member right now, you do not have to pay anything, agree to anything, or continue any conversation that pressures you to take on a debt you did not sign for. Get the name of the collector, the company, and the account they are calling about. Give them the executor’s contact information if there is one. Send a written cease contact request if the calls continue. The pressure is not evidence of obligation.

Understanding how debt is handled in life is the foundation for understanding debt after death. How Collection Accounts Affect Your Credit Report covers what happens when debt goes unpaid and enters collections. And if you are thinking about the bigger picture of what gets left behind, Payable on Death Accounts: What Banks Don’t Tell You goes deeper on the accounts that bypass the estate entirely.

Frequently Asked Questions

Does debt go away when you die?

No. Debt transfers to your estate when you die. Your estate’s assets are used to pay creditors during probate before anything passes to your heirs. If the estate does not have enough to cover all the debts, those debts go unpaid. Your family members do not inherit the unpaid balance unless they cosigned, hold the account jointly, or live in a community property state where the debt applies to them.

Are family members responsible for a deceased person’s debt?

Generally no, with specific exceptions. Cosigners are responsible for the full remaining balance. Joint account holders are equally responsible for anything owed on a shared account. Surviving spouses in community property states may be responsible for debts the deceased incurred during the marriage. In some states, necessaries statutes may require spouses to pay certain medical or care expenses. Beyond these situations, family members are not legally required to pay debts from their own money.

What happens to credit card debt when you die?

Credit card debt becomes a claim against your estate during probate. Creditors are paid from estate assets before heirs receive anything. If the estate has no assets or insufficient assets to pay the balance, it typically goes unpaid. If the card was held jointly with another person, that person owes the full remaining balance. Authorized users on the account are not responsible.

Can debt collectors contact my family after I die?

Collectors can contact a surviving spouse, the estate’s executor or administrator, and the parents of a deceased minor. They can contact other family members once, only to locate the executor, and cannot mention the debt or reveal the call is about a debt during that contact. Any collector who tells a family member they personally owe a deceased person’s debt, when they do not meet one of the exceptions, is engaging in illegal collection tactics. File a complaint with the CFPB and FTC.

Do student loans go away when you die?

Federal student loans, including Parent PLUS loans, are discharged when the borrower dies. The family submits proof of death to the loan servicer and the balance is eliminated. Private student loans depend on the lender’s policy. Some discharge the loan. Many do not. Cosigners on private student loans may become responsible for the full balance when the primary borrower dies. Check the loan agreement for the specific terms.

Is a surviving spouse responsible for a deceased spouse’s debt?

It depends on the state and the type of debt. In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), debts incurred during the marriage are generally shared and a surviving spouse may be responsible even if the debt was only in the deceased’s name. In other states, a surviving spouse is generally not responsible for debts that were solely in the deceased’s name unless they cosigned or held the account jointly. Some states have necessaries statutes covering specific types of medical expenses.

Can creditors take life insurance money to pay a deceased person’s debts?

No, if the policy has a named living beneficiary. Life insurance proceeds pass directly to the named beneficiary outside of probate, which means creditors cannot file claims against them. If the estate is named as the beneficiary or no beneficiary was named, the proceeds become part of the probate estate and can be used to pay debts. Keeping beneficiary designations current and naming a living person is the single most important step to protecting life insurance from your creditors after death.

What is probate and why does it matter for debt?

Probate is the legal process of settling a deceased person’s estate under court supervision. During probate, debts are identified and paid from estate assets before anything passes to heirs. The order of payment is set by state law. If estate assets are not enough to cover all debts, unpaid debts generally do not transfer to family members. Assets with named beneficiaries, like life insurance and retirement accounts, typically bypass probate entirely and go directly to the beneficiary, where they are protected from creditors. Understanding probate is central to understanding how debt after death actually works.