Uber tells new drivers they can earn $23 an hour. DoorDash advertises $15 to $30. These numbers are not made up. They are also not what lands in your bank account. The platforms show you gross earnings on purpose. That number is bigger. It is more appealing. And showing you the number after expenses would make a lot of people never sign up. Gig work real pay, the money left over after taxes, car costs, and the benefits that disappear the day you stop being an employee, looks completely different. This article runs that math. All of it. Not to push you toward a decision. Because you deserve the real numbers before you put miles on your car.

The Number They Show You vs. What You Actually Keep

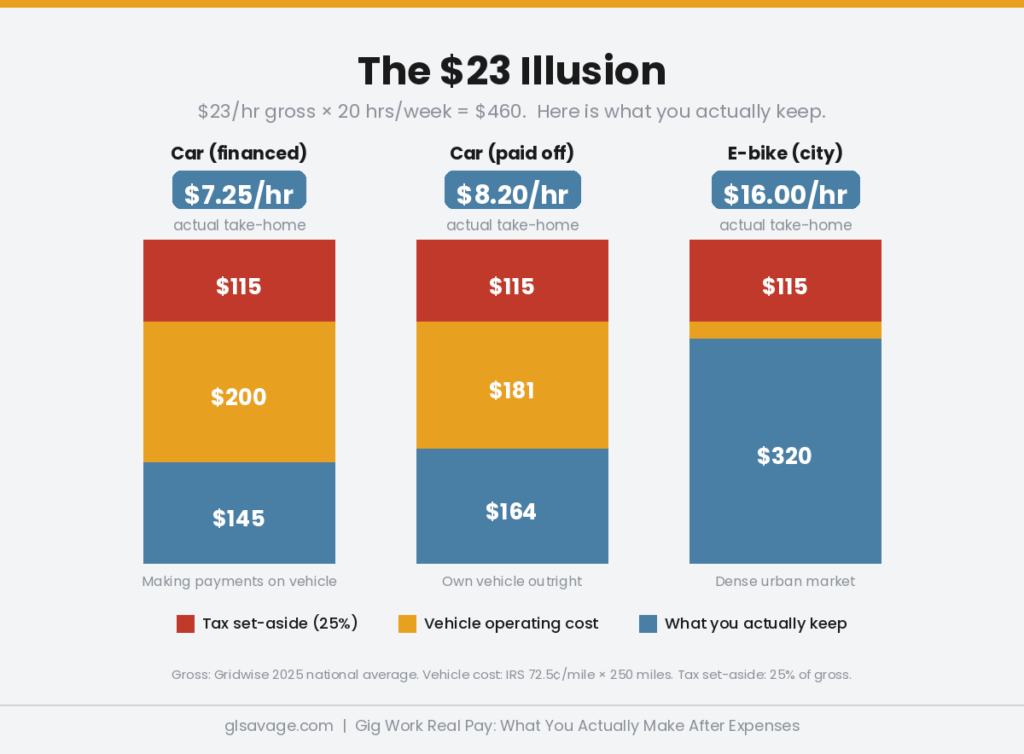

Start with a real example. You drive for Uber 20 hours a week in an average U.S. city. Gridwise, which tracks earnings from over a million gig drivers, puts the Uber national average at $23.33 per hour based on 2025 data. Multiple other sources land in the $20 to $25 range. Call it $23. That is $460 for the week. Here is what happens to that money before you touch it.

The tax nobody warns you about. When you work a regular job, your employer splits your Social Security and Medicare taxes with you. You each pay half. As a gig worker you are legally classified as an independent contractor, which means you pay both halves yourself. The IRS calls this self-employment tax and the rate is 15.3%. On $460 in gig earnings, that is roughly $65 owed to the IRS in self-employment tax before you owe a single dollar of regular income tax. Most tax professionals tell gig workers to set aside 25% to 30% of every payment to cover self-employment tax and income tax together. At 25%, you are setting aside $115 of that $460 before you spend any of it.

Then the car. Every year the IRS publishes a mileage rate based on what it actually costs to run a vehicle, covering gas, oil changes, tires, maintenance, and depreciation. For 2026 that rate is 72.5 cents per mile. Of that, 35 cents per mile is specifically the depreciation piece, meaning the IRS calculates your car loses 35 cents in value for every mile it travels. A driver working 20 hours a week in a mid-size city typically puts on 200 to 300 miles. At 250 miles, the true cost of running your vehicle that week is $181.

Do the math. $460 gross, minus $115 set aside for taxes, minus $181 in vehicle costs, leaves $164 for 20 hours of work. That is $8.20 an hour. Below minimum wage in most states.

That is not a worst case. That is the average case, built from IRS data on what vehicles actually cost to run. The platforms know this math exists. The weekly earnings screen does not show it.

Why Your Car Is the Variable That Changes Everything

The biggest factor in gig work real pay is what you drive. Almost no coverage of this topic treats it seriously.

If you own your car outright and it gets decent gas mileage, your actual per-mile cost may be lower than the IRS rate. The mileage deduction at tax time works in your favor. If you are still making payments on a newer car, you are not just burning through its resale value. You are paying interest on a depreciating asset every month, and that payment exists whether you are logged in or not. It does not go away on your slow weeks.

In dense cities the calculation shifts completely. Delivery drivers in Manhattan, central Chicago, and San Francisco who use e-bikes instead of cars report gross earnings of $20 to $32 per hour with vehicle costs that are almost nothing by comparison. No gas. Minimal maintenance. No depreciation draining away with every mile. The same delivery order that guts a car driver’s net earnings barely touches an e-bike rider’s. If you live somewhere bike delivery is practical and safe, you are looking at a fundamentally different set of numbers.

In suburban and rural markets it tends to go the other direction. Orders are farther apart. Dead miles, the distance you drive to reach a pickup while nothing is running on the meter, make up a larger slice of your total. Base pay per hour is lower because order volume is lower. Your vehicle costs do not care about any of that. The economics in low-density markets often do not support gig work beyond occasional, low-stakes supplemental income.

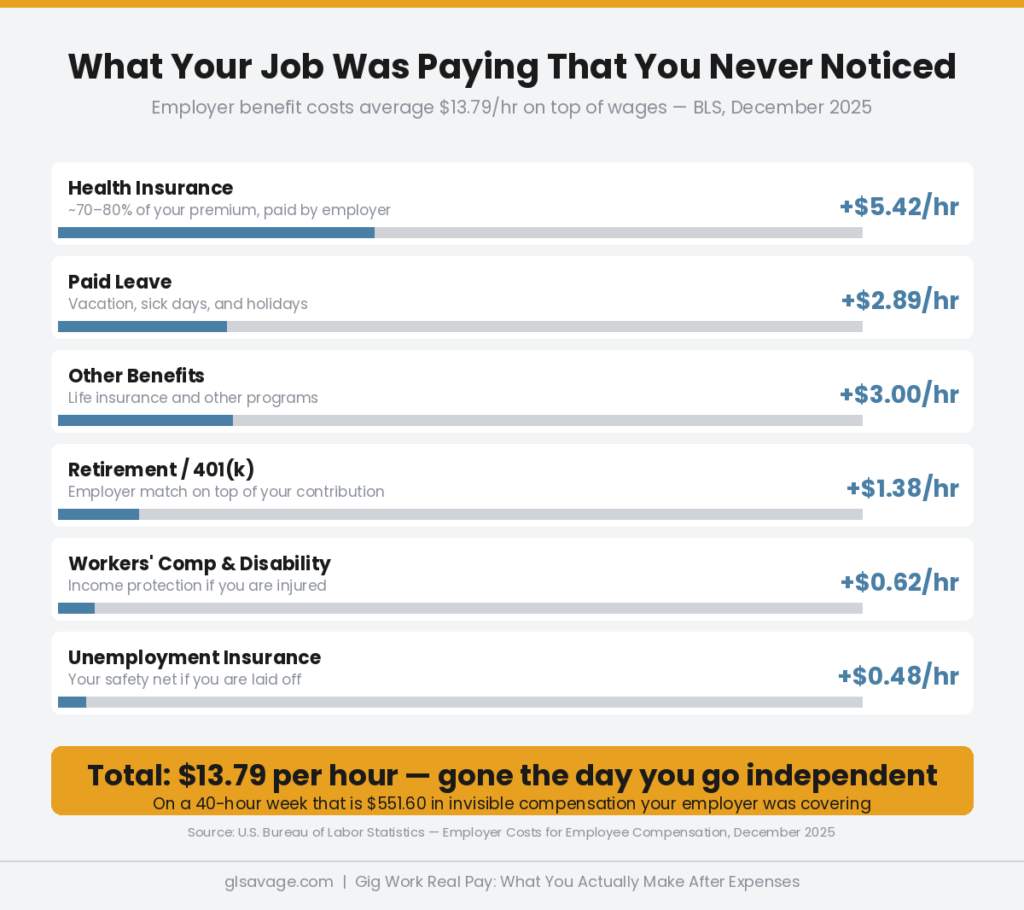

The $13.79 an Hour Your Employer Was Paying That You Never Noticed

Here is the part almost nobody puts in these articles, and it might be the most important part of the whole picture.

Bureau of Labor Statistics data from December 2025 shows that employer benefit costs for private industry workers average $13.79 per hour worked. That money sits on top of your wage. You never see it on your pay stub. But it is real compensation that your employer pays and you receive. When you move to gig work, it does not come with you. It disappears. And because it was never a line item you could point to, most people do not notice it is gone until the moment they need it.

Health insurance. Employers typically cover 70% to 80% of your premium. That arrangement does not exist for gig workers. In 2026 the gap got considerably more expensive. The enhanced ACA premium tax credits in place since 2021 expired at the end of 2025. Marketplace premiums rose roughly 26% on average as a direct result. A 40-year-old gig worker earning $50,000 now faces around $500 to $600 per month for a Silver plan before any income-based tax credits kick in. Once your income clears $60,240 as a single person, those credits disappear and you pay the full amount. A family plan costs considerably more. This is not a theoretical number. It is a bill that lands every month out of the same earnings pool already cut by vehicle costs and taxes.

Retirement. A standard employer 401(k) match runs 3% to 6% of your salary. On $50,000 that is $1,500 to $3,000 a year going into your retirement account just for showing up. Gig workers can open a Solo 401(k) or SEP-IRA, and those are real options worth using, but every dollar in them has to come from you, out of earnings that are already reduced. The gap between a gig worker and a salaried employee with a match compounds every single year they are not receiving one.

Unemployment protection. Lose a traditional job and you can file for unemployment. Lose your gig income, because the platform’s algorithm deactivated your account, because demand in your market dried up, or because you got hurt, and there is no filing to do. Independent contractors do not qualify. This was not an oversight. It was built this way.

Accident coverage, and the gap that exists on purpose. This is where people get badly hurt and no one warned them. Gig platforms provide some liability coverage while you have an active order. But there are three distinct periods in every gig driving session. Period 1 is when your app is on and you are waiting for a request. Period 2 is when you have accepted an order and are on your way to pick it up. Period 3 is when you have the order or passenger and are completing the delivery. Uber and Lyft provide their strongest coverage in Periods 2 and 3. Period 1, the time you spend waiting with the app on, has limited liability coverage from the platform and no collision or comprehensive coverage. Your personal auto policy almost certainly does not cover this period either, because it excludes commercial use. That window, app on, waiting for a ping, is where your vehicle is fully exposed with no coverage from either direction. A rideshare endorsement on your personal policy closes this gap. Adding one to an existing policy costs most drivers $15 to $40 per month depending on insurer and location, with USAA as low as $6 for military-connected members. Before you drive a single paid mile, call your insurer and ask whether your current policy covers rideshare or delivery work. If it does not, get a number for an endorsement. Find out before you need it.

What the Tax System Gives Back, If You Know to Ask

Gig taxes are harder than a regular job. They also have real advantages built in that most drivers never use, because no one explains them at sign-up.

The 72.5 cent mileage deduction is not a reimbursement. It is a deduction that shrinks the income you owe tax on. A driver with 15,000 business miles in a year deducts $10,875 from their taxable income. For someone in the 22% federal tax bracket, that deduction saves roughly $2,393 in federal income tax. It also reduces the self-employment tax owed on those earnings, saving another roughly $1,535. Together, that is nearly $3,900 in taxes that stays in your pocket instead of going to the IRS. The catch is that you have to track every mile as you drive them. The IRS wants records kept at the time, not reconstructed later from memory. Apps like Stride and MileIQ run in the background and log every drive automatically. Three minutes of setup, potentially thousands of dollars recovered.

One decision that matters in your first year: the IRS gives you two ways to deduct vehicle costs. The standard mileage rate is the simpler option. The actual expense method requires tracking every individual vehicle cost and calculating your business percentage. If you choose the actual expense method in your first year, you are locked into it for the life of that vehicle. You cannot switch. Start with the standard mileage rate. It is simpler, it preserves your flexibility, and it works out better for most drivers.

There is a newer deduction that most gig workers have not heard of yet. The One Big Beautiful Bill Act, signed July 4, 2025, created a tips deduction for tax years 2025 through 2028. The IRS has confirmed that gig economy workers including rideshare and delivery drivers are among the qualifying occupations. Tips you receive are deductible up to $25,000 a year. The phase-out starts at $150,000 in yearly income for single filers and $300,000 for married filers. Most gig drivers are well under both. Tips must be reported on a 1099 or similar form to qualify. If you earn meaningful tip income, this deduction changes your actual take-home significantly. Most gig workers do not know it exists.

Other things that belong on your taxes and often get skipped: the share of your phone bill that goes to gig work, delivery bags and equipment, platform fees, the business share of your car loan interest, and a home office if you have a dedicated space for managing your gig business. A tax professional who works with self-employed clients is worth the cost if you are doing serious volume. Their fee is itself deductible.

How the Platforms Are Built to Keep You From Seeing This

The way earnings are displayed on gig apps is not neutral design. It is a choice, made deliberately, and it goes in one direction.

Gross earnings are shown prominently. The app shows your weekly total the moment you open it, in large numbers at the top of the screen. Net earnings after expenses are nowhere. There is no calculation on any platform’s driver app that shows what you actually made per hour after your car costs. You have to build that yourself with information the app does not supply.

The advertised averages are also built from data that skews high. Platforms report earnings during all hours including surge and peak bonus periods. But Uber’s own data shows that most drivers work fewer than 20 hours a week and many work under 10. Drivers logging on for a few hours on a slow Tuesday are not earning the same average as full-time drivers working surge windows. Those casual hours pull the real average down. The platform average includes bonus and surge periods that inflate it. Neither of these facts appears anywhere on the sign-up screen.

Seattle ran a direct experiment on this in January 2024. The city passed a law requiring delivery apps to pay a minimum of $5 per delivery, specifically to ensure drivers earned enough. Here is what actually happened. DoorDash added a roughly $5 regulatory fee to all Seattle orders. Customers, seeing higher totals, tipped less. Uber Eats removed the tip option at checkout entirely. The drop in tips offset more than a third of the base pay increase. On top of that, fewer orders were placed overall because prices were higher, so drivers completed 20% to 30% fewer deliveries per month. Not because drivers stopped logging on. Because customers stopped ordering at the same rate. The platform shifted the cost to customers. Customers reduced tips. The intended benefit to drivers partly dissolved. This is not an argument about whether that law was right or wrong. It is data about how platform economics respond when costs are pushed on them from outside.

The Moves That Actually Change What You Net

None of this means gig work cannot be worth doing. It means the people who make it work do not treat it like a casual income tap. They make specific decisions that change the real hourly number.

Multi-apping means running DoorDash and Uber Eats at the same time and taking whichever order pays better at any given moment. Both platforms technically allow this as long as you finish your current active order before accepting a new one from a different app. Drivers who do this consistently report meaningfully higher hourly earnings than single-app drivers. It takes practice to manage two apps simultaneously. It is the most consistently cited strategy among high earners in gig delivery.

The hours are the job. Lunch from 11 a.m. to 2 p.m. and dinner from 5 p.m. to 9 p.m. are when the orders stack and the tips go up. Weekends outperform weekdays. Rain and bad weather push order volume up because people who would normally go out stay home and order in. Working those specific windows in a dense area and logging off during the flat hours in between is the actual strategy. Drivers who log on whenever it is convenient for their schedule and then wonder why the hourly math does not work are solving the wrong problem.

Not every order is worth taking. DoorDash shows you the delivery destination before you accept most orders. A $7 delivery that sends you 8 miles out to a low-density area, leaving you far from the next pickup, earns you less per real hour than a $5 order in a dense neighborhood where the next request arrives three minutes later. The way to evaluate an order is payout divided by total time including the dead time getting back to a productive zone, not payout alone. Accepting by dollar amount is how new drivers end up with a confused hourly rate and no explanation for it.

Your vehicle costs compound across every single shift. A car that gets 35 miles per gallon costs less per mile than one that gets 22. A paid-off car removes a fixed monthly cost that exists regardless of whether you drive 5 hours or 40 that week. These differences are not dramatic on any individual shift. Across months of gig work they add up to real money.

The Full Picture on Gig Work Real Pay

Gig work real pay lands higher when you are in a dense, high-demand city. When you drive an efficient or fully paid-off vehicle. When you work peak hours with discipline. When you run more than one platform at a time. When you track every business mile from day one and claim every deduction. When health insurance is covered through another source so it does not come out of your gig earnings.

It lands lower when you are in a spread-out market where orders are thin on the ground. When you are making payments on an expensive car and accelerating its depreciation with every mile. When flexibility is the actual goal and the hours you work are off-peak. When you are trying to replace a salaried job and have not added up the cost of replacing the benefits that came with it. Why a Second Job Often Costs More Than It Pays runs that math in detail. When you are not tracking miles and leaving thousands in legitimate deductions unclaimed.

One in three Americans who do gig work say they use it to cover regular living expenses, not extras. The platforms are designed to make that sound like a straightforward plan. Gig work real pay is real money. Whether it is enough money, for your car and your market and your hours, is a math problem that only works with the full set of numbers. You now have them.

Frequently Asked Questions

How much do Uber drivers actually make after expenses in 2026?

Gridwise, which tracks over a million gig drivers, put the Uber national average at $23.33 per hour gross in 2025. After IRS vehicle costs at 72.5 cents per mile and self-employment tax, most drivers in average U.S. markets net somewhere between $8 and $14 per hour depending on vehicle, market, and hours worked. Drivers in dense cities using e-bikes or bikes net more because their vehicle costs are close to zero compared to car drivers.

What taxes do I owe on DoorDash and Uber income?

All of it is taxable. Self-employment tax runs 15.3% and covers the Social Security and Medicare contributions that an employer would normally split with you. On top of that you owe federal income tax at your bracket rate and state income tax where it applies. Set aside 25% to 30% of every payment. If you expect to owe more than $1,000 for the year the IRS requires quarterly estimated payments in April, June, September, and January. Miss them and you owe interest and penalties on top of the original tax.

What can gig workers deduct to lower their taxes?

The biggest one is mileage: 72.5 cents per business mile in 2026. Log them as you drive using an app like Stride or MileIQ. Beyond that: the work-related share of your phone bill, delivery equipment, platform fees, the business share of your car loan interest, and a home office if you have a dedicated workspace. Starting with tax year 2025, tips are deductible up to $25,000 a year under the One Big Beautiful Bill Act. The phase-out starts at $150,000 in yearly income for single filers. Tips must be reported on a 1099. Most gig workers have not heard about this deduction yet.

Does gig work count toward Social Security?

Yes. The self-employment tax you pay on gig income goes into your Social Security and Medicare record exactly the same way payroll taxes from a regular job do. The difference is that a regular employer pays half of those contributions. In gig work, you cover both halves yourself. Your record builds. It just costs more to build it.

What happens to my health insurance when I do gig work?

Nothing happens automatically. You are responsible for finding it and paying for it from the day employer-sponsored coverage ends. In 2026 marketplace premiums rose roughly 26% on average after the enhanced subsidies that had been in place since 2021 expired. A 40-year-old earning $50,000 is looking at $500 to $600 a month for a Silver plan before income-based credits. Once income clears about $60,240 for a single person, those credits are gone. This is a real monthly cost that needs to go into any honest calculation of what gig work actually nets you.

Am I covered by insurance if I get into an accident while delivering?

Less than most drivers realize. Gig platforms provide some coverage during active orders, but the app-on, waiting-for-a-request window called Period 1 has limited liability coverage from the platform and typically no collision or comprehensive coverage. Your personal auto policy almost certainly excludes commercial use entirely during this period. Adding a rideshare endorsement to your existing policy closes this gap and costs most drivers $15 to $40 per month. USAA offers it for as little as $6 for eligible military members. If you have not looked hard at what your current auto policy actually covers, Car Insurance Is a Rigged Game. Here Is How to Play It. explains what insurers count on you not knowing. Call your insurer before your first paid drive and ask specifically whether your current policy covers delivery or rideshare work. Know the answer before you need it.

Is it better to work for Uber, Lyft, DoorDash, or Instacart?

No single platform wins everywhere. Rideshare generally pays higher gross per hour but requires a newer inspected vehicle and involves passengers. Delivery needs less from your vehicle and no passenger interaction. Instacart adds a shopping component and pays differently by market. The highest earners in most cities run more than one platform simultaneously during peak hours and decline orders that fall below a minimum pay-per-mile threshold they set themselves. The platform matters less than what you do with it.

Can you make a full-time living from gig work?

Some people do. It generally requires a high-demand market, an efficient or paid-off vehicle, consistent peak-hour discipline, running multiple apps, tracking every mileage deduction, and either separate health coverage or a plan to fund it from gig earnings. In a low-density market with a financed vehicle and no other source of benefits, the math usually does not work at full-time volume when everything is accounted for. The conditions that make it viable are specific. Fewer drivers meet all of them than the platforms imply.