Banks present themselves as a service. A safe place for your money. A partner in your financial life. The reality is more specific than that. Banks are businesses, and the revenue model at most large banks is built in significant part on fees that fall hardest on customers with the lowest balances and the least margin for error. Roughly 9 percent of bank accounts pay 79 percent of all overdraft and insufficient funds fees. The people walking the thinnest financial line are subsidizing everyone else’s free checking. That is not an accident. That is how banks make money from overdraft fees and a dozen other mechanisms most customers never see. This article covers all of it.

And if you think this problem was getting better, here is the update: it was. Then Congress killed the rule that would have fixed it. Overdraft fee income at major banks started rising again through 2025. The watchdog got defanged. The fees came back. You are reading this at the right time.

How Banks Make Money From Overdraft Fees: The Structure Nobody Explains

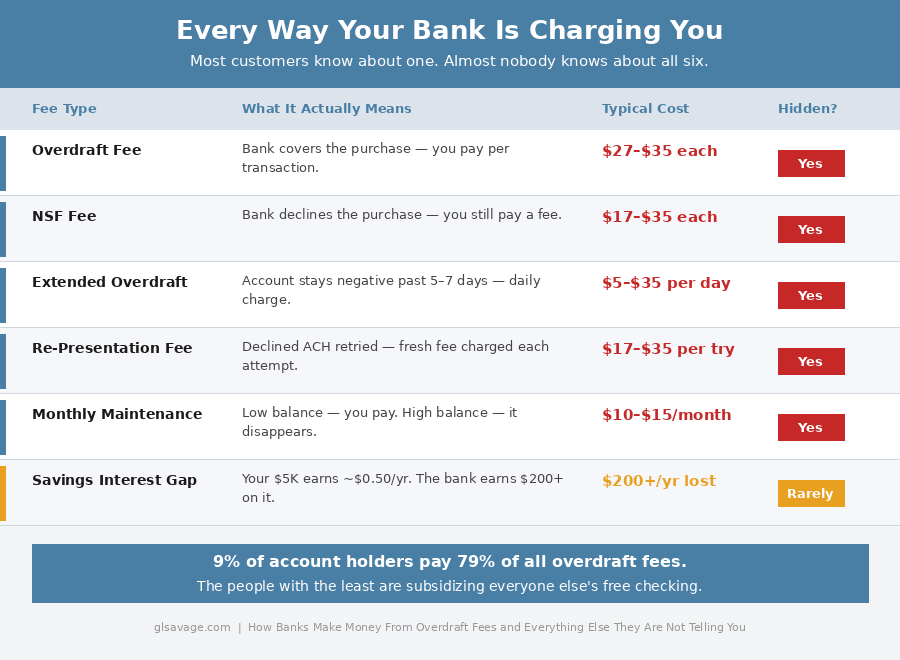

An overdraft happens when you spend more than your available balance. The bank covers the difference and charges you a fee. Most people know that part. Average fee is around $35. Per transaction.

Here is what most people do not know.

When you overdraft, you have taken out a short-term loan without applying for one, without agreeing to interest rate terms, and without receiving the disclosures required for any other loan product. This is the legal foundation of how banks make money from overdraft fees: they have been exempt from the Truth in Lending Act for overdraft transactions since 1969, when overdrafts were treated as an occasional courtesy. That exemption turned a minor administrative accommodation into a multi-billion dollar annual revenue stream.

In December 2024, the Consumer Financial Protection Bureau finalized a rule that would have capped overdraft fees at $5 for large banks or required them to treat overdraft as a loan with full lending disclosures. It was projected to save consumers $5 billion per year. Congress repealed it in April 2025. President Trump signed the repeal in May 2025. The $35 fee structure is now locked in with no federal rule in sight to change it.

And the fees are climbing. Reuters analyzed data from the 20 largest U.S. banks and found that 14 of them posted increases in overdraft and NSF fee income through the first nine months of 2025. One senior banking researcher put it plainly: when the watchdog was put to sleep, some institutions went back out on the prowl.

JPMorgan Chase collected over $1 billion in overdraft fees in 2024. So did Wells Fargo. Just those two banks. In a single year. JPMorgan earned over $51 billion that year without a single overdraft fee. The fees are not necessary for their survival. They are a choice about whose money to take. And if you are in the bottom tier of account holders, a consulting firm estimated that customers who heavily use overdraft services generate more than $700 in profit for their bank per year on a basic checking account. Customers who never overdraft generate about $57. You do the math on who they are designing the system for.

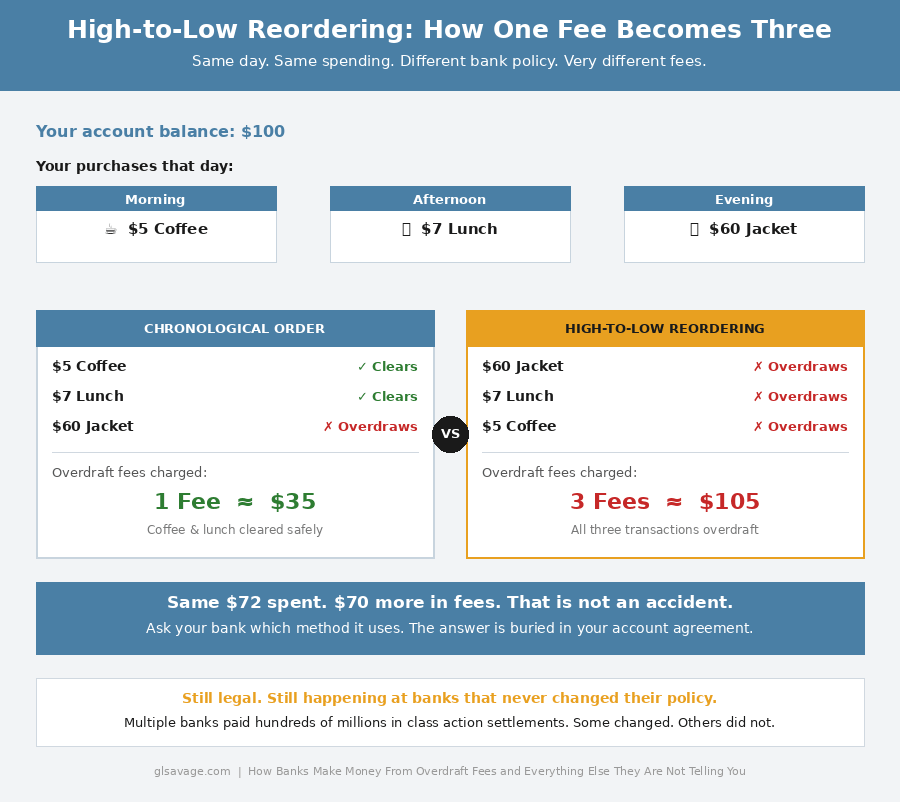

High-to-Low Transaction Reordering: How One Overdraft Fee Becomes Four

Many banks process transactions not in the order you made them but from highest dollar amount to lowest. Walk through what that means in practice. You have $100 in your account. You buy a $5 coffee in the morning, a $7 lunch in the afternoon, a $60 jacket in the evening. In chronological order, the coffee and lunch clear fine. Only the jacket overdraws you. One fee. But if the bank reorders highest to lowest, the $60 jacket hits first, drops your balance to $40, and now the lunch and the coffee both overdraft. Three fees instead of one. An extra $70 in charges for the exact same spending on the exact same day.

Harvard Business School researchers studied this practice and confirmed that it can turn a single overdraft into a cascade of fees, with the damage falling hardest on people with low balances. Multiple banks were sued over this practice and paid hundreds of millions in class action settlements. Some changed their policies. Others did not. It is still legal. It is still happening. Ask your bank directly what order it uses to process transactions. The answer exists somewhere in your account agreement, in language written to discourage you from reading it.

NSF Fee vs. Overdraft Fee: The Charge You Pay Even When the Transaction Fails

Most people mix up these two fees. The difference matters because the rules are not the same.

An overdraft fee is charged when the bank covers a transaction you do not have enough money for. The transaction goes through. You owe the covered amount plus the fee. An NSF fee is charged when the bank declines the transaction. The transaction does not go through. You are still charged a fee, averaging around $17, for the attempt that failed.

You read that correctly. The transaction fails and you still get charged. And because the payment did not go through, you may also face a late fee or returned payment fee from whoever you were trying to pay. One failed payment. Fees from two directions at once.

For debit card and ATM transactions, banks are required to get your consent before charging overdraft fees. You have to say yes before they can charge you. For checks and ACH payments including automatic bill pay, no consent is required. The bank can charge an NSF fee without you ever agreeing to it. Most customers do not know this distinction exists.

Some banks re-present a declined ACH transaction two or three times and charge a fresh NSF fee on each attempt. There is no federal law limiting how many times a transaction can be resubmitted. Some banks stopped this under regulatory pressure. Others have not. And with the CFPB now defanged, the pressure to stop is considerably lighter than it was two years ago.

The Extended Overdraft Fee: The Daily Penalty That Keeps Running

The first fee is not the last one. Many banks charge what is called an extended overdraft fee if your account stays negative after a set number of days, typically five to seven. This fee is separate from and on top of the original. It can run $5 to $35 per day depending on the bank.

Think through what that looks like. You overdraft by $40 on Monday. You do not notice immediately, or you cannot cover it right away. You carry a negative balance for a week. You are now looking at the original overdraft fee plus five to seven days of extended fees stacked on top. The total fees can exceed the original overdraft amount several times over.

Most customers do not know this fee exists until it appears on their statement. Ask your bank whether they charge extended overdraft fees, how many days before they kick in, and what the daily amount is. Ask before you need to know.

The Phantom Opt-In: Overdraft Fees You Never Agreed To

Here is the part nobody talks about. Banks do not pitch overdraft coverage randomly. They pitch it at the exact moment you are most likely to say yes: when you are opening a new account. You are sitting across from a bank employee or clicking through a signup screen, agreeing to terms, selecting preferences, getting set up. You are already in a yes mindset. Some banks train staff to frame overdraft as protection. Your card will not get declined in an embarrassing moment. You will not miss a bill payment. The fee is buried. The risk is not mentioned. And if you click through too fast or the employee skips it entirely, you may end up enrolled without ever consciously choosing it.

Federal law requires banks to get your consent before enrolling you in overdraft coverage for debit card and ATM transactions. You have to say yes before they can charge you. The bank cannot charge you those fees unless you agreed to it. And the CFPB found that some banks charged these fees without any documented evidence that customers had ever agreed to anything. Atlantic Union Bank was ordered to pay $6.2 million. TD Bank, TCF National Bank, Navy Federal Credit Union, Wells Fargo, and Regions Bank have all faced enforcement actions for illegal overdraft practices. Combined refunds and penalties totaling hundreds of millions of dollars. All of them claiming to serve you.

If you have overdraft coverage on debit card and ATM transactions and do not remember opting in, it is worth finding out whether your consent was actually documented. You can opt out at any time through your bank’s app or by calling customer service. No explanation required.

The Available Balance Illusion: Where Surprise Overdrafts Come From

Your bank shows you two numbers: your current balance and your available balance. Most people treat them as the same. They are not. That gap is where most overdrafts you did not see coming actually start.

Your current balance reflects transactions that have fully cleared. Your available balance is adjusted for pending transactions, holds, and items still processing. A deposit you made this morning may show in your current balance but not your available balance. A debit card purchase from yesterday may be pending but not settled. A check you wrote may not have cleared. You see a number that looks fine, spend based on it, and get hit with a fee because the real available balance was lower than what the screen showed you.

Banks are required under Regulation CC to make certain deposits available within specific timeframes, but holds on checks can extend availability by days. The overdraft policy itself, including how your bank processes transaction order, is buried somewhere in a 30-to-60-page account agreement in a subsection with no clear heading, written in language designed to be skimmed past. Knowing what your bank actually does before you spend is the only protection against overdrafts you never saw coming.

This is also why getting a bank account in the first place matters so much. If you are unbanked, you have almost no visibility into any of this. The hidden costs of not having a bank account go well beyond what most people realize.

The Savings Account Interest Rate Gap: Your Money Working for Them, Not You

The average big bank savings account pays somewhere between 0.01 and 0.10 percent APY. At 0.01 percent, $5,000 in savings earns fifty cents a year. Not fifty dollars. Fifty cents. The bank takes that same $5,000 and earns anywhere from 4 to 8 percent lending it out or investing it. The spread between what they pay you and what they earn on your money is one of the largest and most invisible wealth transfers in retail banking, and it runs every single day.

High-yield savings accounts at online banks have paid 4 to 5 percent APY in recent years. That same $5,000 at 4.5 percent generates $225 a year. Not fifty cents. The money is still FDIC insured. The only difference is the bank is no longer keeping most of the return for itself.

Ally, Marcus by Goldman Sachs, and Discover Bank consistently offer significantly higher yields. Your bank has no incentive to tell you this. That should tell you something. And if you are trying to build an emergency fund living paycheck to paycheck, the account you choose to park that money in matters more than most people think.

The Arbitration Clause: Why You Cannot Sue in Court

Almost every bank account agreement contains a mandatory arbitration clause. If the bank harms you, you cannot join a class action lawsuit. You must pursue individual arbitration, a process that is expensive, slow, conducted by arbitrators who are frequently selected by the institution, and statistically favored toward the bank. Customers signing up today have almost certainly signed away the right to sue in a court of law.

This is why the CFPB complaint process matters. Filing a complaint at consumerfinance.gov/complaint is one of the few meaningful recourse mechanisms left. The CFPB is a regulatory agency, not a court, but it has authority over practices that your account agreement signed away your right to challenge in court before you ever had a problem. Your complaint is not just paperwork. It is data they act on. Or at least it was when the CFPB had full enforcement power. With the agency significantly scaled back as of 2025, this mechanism has weakened. File the complaint anyway. It creates a record. Records matter when the political winds shift.

Regulation E Dispute Rights: The Clock You Do Not Know Is Running

Someone makes an unauthorized transaction on your account. You have rights under federal law to dispute it and get your money back. But a clock starts the moment you discover it, and the longer you wait, the less protection you have.

Report it within two business days: your maximum liability is $50. Wait longer than two business days: your liability jumps to $500. Wait past 60 days: the bank may not be required to return any of it. At all.

The clock starts when you discover the problem. Not when it happened. A fraudulent charge that sat unnoticed for two months because you never check your statements is legally yours to eat. Banks know this. They are not going to remind you. Check your account. When you see something wrong, dispute it the same day.

The ChexSystems Trap: How One Bad Account Follows You for Five Years

Most people have never heard of ChexSystems. They find out about it the hard way, when they try to open a new checking account and get denied.

ChexSystems is a consumer reporting agency that tracks your banking history. Unpaid overdraft fees. Bounced checks. Accounts closed by the bank for cause. When you apply for a new account, most banks pull your ChexSystems report before approving you. A negative record can mean a flat no. And it stays on your report for five years.

Here is where the trap closes. You fall behind at one bank, accumulate fees you cannot cover, the account gets closed, it gets reported, and now you cannot get a new account anywhere mainstream. Without a bank account, direct deposit is harder. Check cashing costs money. Bills become harder to manage. Being unbanked is expensive. Which is the exact opposite of what someone who just lost a bank account needs. Harvard researchers found that some low-income customers, facing this exact wall, turn to payday lenders to repay overdraft fees, pulling themselves into a second debt spiral to escape the first one. How payday loans are legal and what to do instead breaks down exactly how that trap works and what the exits look like.

You are entitled to a free ChexSystems report once per year at ChexSystems.com. Pull it. Review it for errors. Under the Fair Credit Reporting Act you can dispute inaccurate information in writing and they are required to investigate. Errors show up more often than people expect. Capital One stopped using ChexSystems over a decade ago. Chime does not use it. Navy Federal Credit Union does not pull it. If you have a negative record, those are the first places to look.

Early Warning Services: The Second Banking Database Almost Nobody Knows About

ChexSystems is not the only one. Early Warning Services is a second consumer reporting agency used by many banks to screen account applicants. Less well known. Covers some of the same ground with different data sources. And it also operates Zelle.

If you have had fraud disputes, unauthorized transactions, or account issues involving Zelle, that activity can appear in your Early Warning Services record and affect your ability to open accounts. Many people who know about ChexSystems have never heard of Early Warning Services and do not know they can request their report.

You have the right to request your free report under the Fair Credit Reporting Act. Go to earlywarning.com. If your ChexSystems report is clean but you are still being denied accounts, Early Warning Services is the next place to look.

When the System Shuts You Out: Second Chance Accounts and Bank On

Most people in this situation never hear about two options that can get them back inside the banking system.

Second chance checking accounts are offered by banks that pull ChexSystems but are willing to work with customers who have negative records. These accounts may have restrictions but they keep you inside the banking system and typically offer a path to a standard account after a period of responsible use.

Bank On accounts are certified by the Cities for Financial Empowerment Fund and must meet specific consumer-friendly standards: no overdraft fees, no minimum balance requirements, low or no monthly fees, and free basic transaction capabilities. Real checking accounts at real banks and credit unions, not prepaid cards. A full list is at joinbankon.org.

Prepaid Debit Card Fees: The Trap People Turn To When Banks Turn Them Away

People who cannot get a checking account often turn to prepaid debit cards. Some prepaid cards are reasonable. Many are not. Common fees include monthly maintenance fees, per-transaction fees charged every time you make a purchase, ATM withdrawal fees, reload fees, inactivity fees, and fees just to check your balance. The fees are disclosed in the cardholder agreement. They are not always disclosed clearly at the point of purchase.

Before loading money onto any prepaid card as a substitute for a bank account, read the full fee schedule and compare the total monthly cost against a Bank On certified account. In most cases the Bank On account costs significantly less and comes with FDIC insurance. If you are going to use a prepaid card, the American Express Serve, Bluebird, and Walmart MoneyCard are considerably less predatory than most. Read the fee schedule before you load anything.

Courtesy Pay at Credit Unions: The Same Problem in a Different Building

Credit unions are generally better than large commercial banks on fees. Generally. Not always. Some credit unions run overdraft programs that are just as aggressive as the banks people left to get away from them.

Many credit unions offer a program called courtesy pay, their version of overdraft coverage. In some credit unions it is structured and priced exactly like big bank overdraft programs, with per-transaction fees in the $25 to $35 range and automatic enrollment you have to actively opt out of.

When you open an account at a credit union, ask the same questions you would ask a bank. What is the courtesy pay fee. Is enrollment automatic or do you opt in. Is there an extended fee if the account stays negative. What order are transactions processed. A good credit union with transparent, low-fee policies is genuinely a better option than most large commercial banks. A credit union running an aggressive courtesy pay program is not.

Monthly Maintenance Fees: A Tax on Low Balances

Many checking accounts charge a monthly maintenance fee of $10 to $15 that disappears if you maintain a minimum balance. Someone with a comfortable cushion pays nothing. Someone living paycheck to paycheck pays $120 to $180 per year just for having the account. The fee is regressive by design. It extracts the most from the people with the least.

It also compounds. An overdraft fee pulls money from your account. A lower balance makes the next overdraft more likely. A monthly maintenance fee further erodes the buffer. Each fee makes the next one more probable. The system is self-reinforcing at the bottom, and that is not a design flaw. That is the poverty premium at work inside the banking system. The poverty premium shows up in insurance, in rent-to-own stores, in check cashing fees, and in the exact structure described in this article.

What You Can Actually Do About This

Knowing how banks make money from overdraft fees is only useful if you do something with it. Start here.

The single most valuable thing most people reading this can do today, right now, in two minutes: opt out of overdraft coverage for debit card and ATM transactions. Open your bank’s app, find account settings, turn it off. Or call the number on the back of your card and say you want to opt out of overdraft coverage. They have to do it. No explanation required. Your card will decline when funds run short. That is occasionally inconvenient. It is almost always cheaper than the fee.

Find out whether your bank uses high-to-low transaction reordering. Ask directly. If it does and you have better options, that is a reason to move.

Ask specifically about extended overdraft fees. Know how many days before they trigger and how much they cost per day. Ask whether your bank has a minimum threshold below which they do not charge a fee at all. Some do. Most do not tell you.

Set up low-balance alerts. Most banks offer text or push notifications when your balance drops below a number you set. Five minutes of setup can prevent months of fees.

If your savings are earning near nothing, compare rates at online banks. Same FDIC insurance. Significantly larger return on money you have already saved.

If you have a negative ChexSystems or Early Warning Services record, pull both reports, review them for errors, and dispute anything inaccurate. Look for Bank On certified accounts or institutions that do not use these databases while disputes are pending.

If you have been charged overdraft fees you did not agree to, or had unauthorized transactions on your account, file a complaint with the CFPB at consumerfinance.gov/complaint. Individual complaints contribute to enforcement patterns that have resulted in hundreds of millions of dollars in consumer refunds. Your complaint is not symbolic. It is data.

Check your account regularly. Under Regulation E your liability for unauthorized transactions rises sharply after two business days and becomes potentially unlimited after 60 days. Checking your account is a legal protection, not just a budgeting habit.

And if you are managing money under serious financial pressure, read about the real cost of eating cheap and why a second job often costs more than it pays. The bank fees are one layer of the system. There are others.

What the System Is Counting On

The overdraft fee structure was built in 1969 as an occasional banking courtesy. It was exempted from lending laws on that basis. Then it was quietly turned into a structured revenue extraction mechanism targeting the customers least able to absorb the cost. That is how banks make money from overdraft fees at scale. Congress had the opportunity in 2025 to cap those fees at $5. It voted to kill the rule instead, 217 to 211. The president signed it. The arbitration clause in your account agreement makes it nearly impossible to challenge the bank in court. ChexSystems and Early Warning Services make it difficult to leave. The savings account interest gap silently transfers wealth from depositors to shareholders every single day. None of it requires anyone to do anything illegal.

One bank CEO named his yacht Overdraft. That is not a rumor. That is a documented fact from someone who studied this industry closely. It tells you everything you need to know about how the people running these institutions view the fee that is costing you sleep.

Here is what “defanged” actually means. As of 2025, the CFPB’s enforcement staff was cut by roughly 90 percent. The agency dropped active investigations and closed cases that were in progress. No major new enforcement actions against banks have been initiated since January 2025. The institution that fined Wells Fargo, TD Bank, Navy Federal, and Regions Bank for illegal overdraft practices is currently not doing that. The banks know it. That is part of why the fees are going back up.

This is the system working exactly as designed. Understanding how banks make money from overdraft fees is not a mystery once someone lays the structure bare for you. It is a documented, legal, deliberate structure. Most people do not find out about high-to-low transaction reordering until it has already cost them. Most people do not know ChexSystems exists until they are denied an account. Most people do not know the Regulation E clock is running. Now you do. What you do with that is up to you.

Frequently Asked Questions About How Banks Make Money From Overdraft Fees

Banks charge a fee, typically $27 to $35, every time they cover a transaction that exceeds your account balance. Because banks have been exempt from lending laws for overdraft transactions since 1969, they are not required to disclose interest rates or loan terms the way they would for any other credit product. Roughly 9 percent of account holders pay 79 percent of all overdraft fees, concentrated among customers with the lowest balances and least financial margin. In 2024, JPMorgan Chase and Wells Fargo each collected over $1 billion in overdraft fees. The CFPB attempted to cap these fees at $5. Congress repealed that rule in May 2025.

Yes. After several years of decline, overdraft fee income started rising again at major banks in 2025. Reuters found that 14 of the 20 largest U.S. banks posted increases in overdraft-related income through the first nine months of 2025. Analysts point to both economic pressure on consumers and the May 2025 repeal of the CFPB overdraft rule, which would have capped fees at $5, as contributing factors.

High-to-low reordering is a practice where some banks process daily transactions from the highest dollar amount to the lowest rather than in the order they occurred. This drains your balance faster, turning one potential overdraft into multiple overdrafts with a fee for each. Multiple banks paid hundreds of millions in class action settlements over this practice. It remains legal. Ask your bank directly what order it uses to process transactions.

An overdraft fee is charged when the bank covers a transaction you do not have enough money for. The transaction goes through. An NSF fee is charged when the bank declines the transaction. The transaction does not go through. You are still charged a fee either way. For checks and ACH automatic bill payments, banks can charge NSF fees without your prior consent. Some banks re-present declined ACH transactions multiple times, charging a fresh NSF fee each time.

An extended or sustained overdraft fee is an additional daily charge applied when your account remains negative beyond a set number of days, typically five to seven. It is separate from and on top of the original overdraft fee and can run $5 to $35 per day at some banks. Most customers do not know this fee exists until it appears on their statement.

Yes. For debit card and ATM transactions you can opt out at any time through your bank’s app or by calling. With overdraft coverage off, your card declines when funds are insufficient and no fee is charged. For checks and automatic bill payments the rules are different and declining those transactions may still result in NSF fees depending on your bank’s policy.

A phantom opt-in occurs when a bank charges overdraft fees on debit card or ATM transactions without any documented evidence that the customer ever agreed to it. Federal law requires the customer to say yes before those fees can be charged. The CFPB has taken enforcement actions against multiple banks including Atlantic Union Bank, TD Bank, Navy Federal Credit Union, Wells Fargo, and Regions Bank for illegal overdraft practices resulting in hundreds of millions in consumer refunds.

ChexSystems is a consumer reporting agency that tracks banking history including unpaid overdraft fees, bounced checks, and bank-closed accounts. Most banks pull your ChexSystems report when you apply for a checking account. Negative information stays on your report for five years. Request your free annual report at ChexSystems.com. Under the Fair Credit Reporting Act you can dispute inaccurate information in writing.

Early Warning Services is a second consumer reporting agency used by many banks to screen account applicants. It also operates Zelle. If you have had fraud disputes or account issues involving Zelle, that activity can appear in your Early Warning Services record. You can request your free report at earlywarning.com and dispute inaccurate information under the Fair Credit Reporting Act. If your ChexSystems report is clean but you are still being denied accounts, Early Warning Services is the next place to look.

Bank On is an initiative run by the Cities for Financial Empowerment Fund that certifies checking accounts meeting specific consumer-friendly standards: no overdraft fees, no minimum balance requirements, low or no monthly fees, and free basic transaction capabilities. These are real checking accounts at real financial institutions, not prepaid cards. A full list is available at joinbankon.org.

Under Regulation E, if you report an unauthorized debit card or bank account transaction within two business days of discovering it, your maximum liability is $50. After two business days your liability rises to $500. After 60 days your liability can be unlimited. The clock starts when you discover the problem, not when it occurred. Check your account regularly. Dispute unauthorized transactions immediately.

Most large bank savings accounts pay between 0.01 and 0.10 percent APY while the bank earns significantly higher returns lending and investing your deposits. High-yield savings accounts at online banks have paid 4 to 5 percent APY in recent years. The same $5,000 earning 4.5 percent generates $225 a year instead of roughly 50 cents. The money remains FDIC insured. Your bank has no incentive to tell you this difference exists.

Almost every bank account agreement contains a mandatory arbitration clause that prevents you from joining a class action lawsuit against the bank. If the bank harms you, you must pursue individual arbitration, a process that is expensive, slow, and statistically favored toward the institution. Your account agreement signed away your right to sue in court before you ever had a problem. Filing a complaint with the CFPB at consumerfinance.gov/complaint is one of the few meaningful recourse mechanisms left.

Generally yes, but not universally. Many credit unions offer a program called courtesy pay which is their version of overdraft coverage, and some structure it with fees and automatic enrollment similar to large bank overdraft programs. When opening an account at a credit union, ask the same questions you would ask a bank: what is the fee, is enrollment automatic, is there an extended fee for sustained negative balances, and what order are transactions processed.

Yes. Capital One, Chime, and Navy Federal Credit Union do not use ChexSystems. Second chance checking accounts are available at some banks willing to work with negative records. Bank On certified accounts at joinbankon.org do not require clean banking history and have no overdraft fees by certification standard. Pull both your ChexSystems and Early Warning Services reports, dispute any errors, and explore these options while disputes are pending.

The rule, finalized in December 2024, would have required large banks to cap overdraft fees at $5 or treat overdraft as a loan subject to lending disclosures. Banking industry groups argued it was government price control that would limit consumer access to credit. Congress passed a resolution to overturn it in April 2025, with the Senate voting 52 to 48 and the House voting 217 to 211. President Trump signed it in May 2025. The repeal also blocks the CFPB from passing a substantially similar rule without a new act of Congress.