A payable on death account is one of the simplest tools in personal finance. You name a person. They get the money when you die. No court. No waiting. Done. That is how the industry describes it, and that part is true. What the industry leaves out is everything that can go wrong: the government program that can legally take the money back, the Social Security problem that blindsides families every single day, the creditor exposure most people never see coming, and the hidden FDIC insurance benefit that almost nobody knows exists. This article covers the full picture of how a payable on death account actually works, because simple is not the same as risk-free.

What a Payable on Death Account Actually Is

A payable on death account, or POD account, is a regular bank account with one extra instruction attached to it. That instruction names a specific person to receive the money in the account when the owner dies.

While the owner is alive, the account works exactly like any other account. The named person, called the beneficiary, has no access. They cannot see the balance. They cannot make withdrawals. They have no legal claim to anything. The account is entirely the owner’s.

When the owner dies and the bank is notified, the instruction activates. The beneficiary goes to the bank, shows a valid ID and a certified death certificate, fills out a claim form, and the bank transfers the funds. No court involved. No attorney required.

That is the system working as designed. The problems come from what the system does not tell you before, during, and after that process.

What Actually Happens at the Bank After a Payable on Death Account Holder Dies

Most articles stop at “show a death certificate and the money transfers.” There are four things that actually happen, and families who do not know them in advance find out the hard way.

First, the bank has to be notified. That does not happen automatically. Nobody calls the bank when a person dies. The beneficiary, or someone handling the estate, has to contact the bank directly and inform them.

Second, a certified death certificate is required. Not a photocopy. Not a printed scan. A certified copy issued by the county or state, with a raised seal or official stamp. Most families need multiple certified copies because every institution wants its own. Order more than you think you need. Funeral homes can help with this. Certified copies typically cost between ten and twenty-five dollars each depending on the state.

Third, the bank will have its own claim form for the beneficiary to complete. This is separate from the death certificate. It asks for the beneficiary’s personal information and confirms their identity. Some banks process this in a single branch visit. Others route it through an estate department and it takes a few business days.

Fourth, if the account has multiple beneficiaries, each one has to claim their portion separately. The bank does not automatically divide and distribute. Each person comes in on their own, with their own ID and their own certified death certificate copy, and completes their own claim.

Knowing this in advance means the family is not standing at a bank counter unprepared on one of the worst days of their lives.

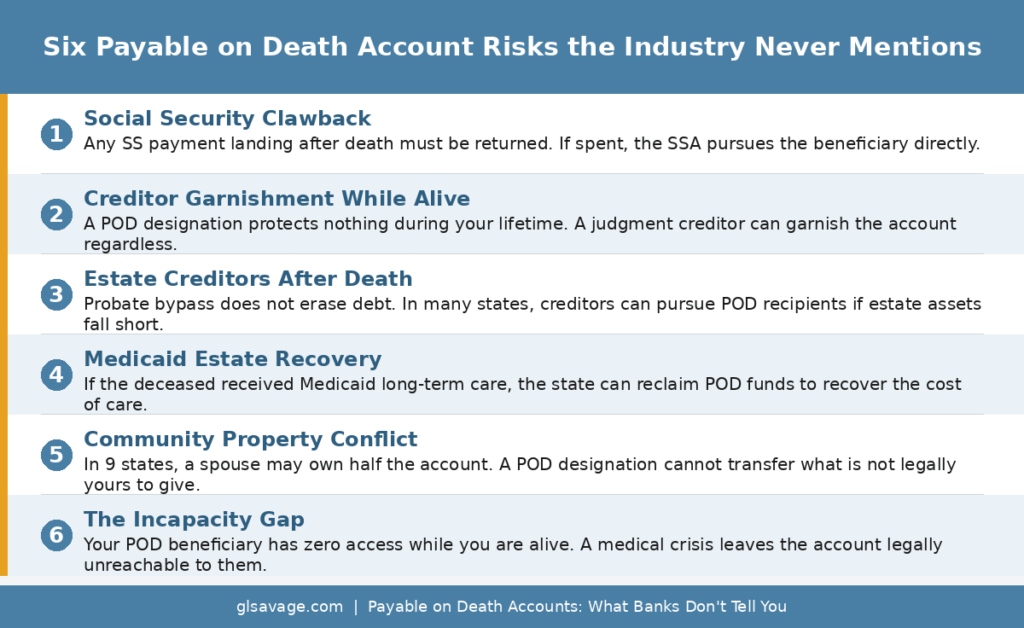

The Social Security Problem Nobody Warns You About

Social Security pays benefits one month behind. The payment that arrives in May covers April. So when someone dies, whatever Social Security payment lands in their account after the date of death does not belong to the family. It belongs to the Social Security Administration, and the SSA requires it to be returned.

Banks are legally required to return Social Security deposits received after a beneficiary’s death when notified by the SSA. In some cases, the bank reverses the deposit before anyone even knows it is happening.

Here is where it becomes a real problem. A family member who is named as the POD beneficiary claims the account quickly after the death, which is the right move. The money transfers. They use some of it to cover immediate costs: funeral expenses, rent, utilities. Then weeks later, the Social Security Administration claws back that deposit from the account. If the account has already been closed and the funds distributed, the SSA can pursue the beneficiary directly to recover the money.

The solution is specific and simple. Notify the Social Security Administration of the death as quickly as possible. The funeral home can do this on your behalf, and most will if you ask. The faster the SSA is notified, the less likely an errant payment is. If you are the beneficiary claiming the account, check whether any Social Security deposits landed after the date of death before spending anything. If one did, set that amount aside. Do not spend it. It will be reclaimed.

Your Payable on Death Account Can Be Garnished While You Are Alive

While you are alive, a POD designation offers zero protection from your own creditors. If a court issues a judgment against you, a collections attorney can garnish your bank account. It does not matter that someone is named as a beneficiary. The account is legally yours. Your creditors can reach it.

If you are dealing with debt collectors, lawsuits, or judgments and you have been told to add a POD designation to protect your money, that advice is wrong. A POD account is not a legal shield. It is a transfer instruction.

There is no simple fix for this one. If protecting assets from creditors during life is a real concern, that is a conversation for a bankruptcy attorney or an asset protection attorney, not a bank form.

What Happens to a Payable on Death Account When the Estate Has Debts

The creditor problem does not end at death. A POD account bypasses probate, but bypassing probate does not mean bypassing all obligations.

When someone dies with significant debts, those debts do not disappear. Creditors have the right to make claims against the estate. The estate is whatever assets went through probate. If the assets in probate are not enough to cover the debts, creditors in many states can look beyond probate to other assets, including POD accounts.

This varies significantly by state law. Some states explicitly protect POD accounts from estate creditors. Others do not. In states that allow it, a creditor can pursue the beneficiary who received the POD funds and demand repayment up to the amount of the debt. The beneficiary may have already spent the money. That does not end the obligation.

The practical solution is to understand the state you live in before assuming a POD account is untouchable after death. If the deceased had significant medical debt, credit card debt, or other obligations, and the estate assets are thin, the beneficiary should not treat the POD funds as fully theirs until they have clarity on whether creditors are making claims. An estate attorney can provide a clear answer for a specific state. One hour of consultation can prevent a serious financial surprise.

The Medicaid Clawback Most Families Never See Coming

Medicaid is the government health insurance program for people with low income. It covers nursing home care and long-term care for elderly people who cannot afford it privately. That coverage is not free. It is a loan the government expects to be paid back from the person’s estate after they die. This is called Medicaid estate recovery.

In a significant number of states, Medicaid estate recovery reaches beyond just the probate estate. It can pursue assets that transferred outside of probate, including payable on death accounts. The beneficiary who received the funds can be required to hand them back to the state to repay the cost of care.

This is not a penalty. It is not a fine. It is the legal recovery of money the government spent on care, which federal law requires states to pursue. The family may have had no idea the person was on Medicaid, no idea what estate recovery was, and no idea the POD account was reachable. None of that protects the funds.

If a parent or grandparent received Medicaid long-term care and had a POD account, anyone named as beneficiary should contact the state Medicaid agency before spending those funds. Many states send a notice. Some do not. Do not wait for a notice.

For people planning ahead, the solution is a Medicaid asset protection trust. Assets held in that kind of trust are generally exempt from estate recovery in most states. That requires working with an elder law attorney, but for families where long-term care is a realistic future situation, it is worth understanding early. Waiting until Medicaid is already involved is too late to use most protection strategies.

The Payable on Death Account and Married Couples in Community Property States

Nine states in the United States operate under community property rules: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

In these states, money earned by either spouse during a marriage is generally considered jointly owned, fifty-fifty, regardless of whose name is on the account.

This matters for payable on death accounts because the account owner can only give away what they legally own. If half the money in an account legally belongs to a spouse, the account owner cannot direct one hundred percent of it to a POD beneficiary. They can only designate their half.

This creates a real problem when someone in a community property state names a child, sibling, or anyone other than their spouse as the POD beneficiary on an account funded with marital earnings. The beneficiary may receive the funds. The surviving spouse may have a legitimate legal claim to half of them. That dispute can end up in court.

The solution in community property states is to be explicit. If you intend your spouse to receive your half as well, say so with a proper beneficiary designation or a trust structure that your spouse agrees to. If you intend the funds to go elsewhere, understand that your spouse’s interest in the money may not go with them. An estate planning attorney in a community property state can clarify this in a single conversation.

A POD Account Is Not a Living Trust

Banks and estate planning marketers often describe POD accounts as a poor man’s trust or a free substitute for a living trust. The transfer part is true. Everything else they are implying is not.

A living trust is a legal structure that holds assets on behalf of a beneficiary under specific conditions. You can set rules. You can say the money goes to your child but only after they turn twenty-five. You can appoint someone to manage the funds if the beneficiary is a minor or has a disability. You can direct how the money is used. A trust gives you control over what happens after you are gone.

A POD designation gives you none of that. The money transfers. That is the entirety of the instruction. If the beneficiary is seventeen years old, a court may need to step in to manage the funds until they reach adulthood, which is the probate involvement you were trying to avoid. If the beneficiary has a gambling problem, a drug addiction, or is in a financially abusive relationship, the full account balance lands in their hands with no conditions attached. If you wanted the money used for education or medical care, you have no mechanism to enforce that.

POD accounts are genuinely useful. They are fast, free, and simple. But they are a transfer tool, not a planning tool. Anyone with a complicated family situation, a beneficiary who needs guidance, or specific wishes about how the money should be used should talk to an estate planning attorney about whether a trust makes more sense. The consultation is not free. Losing control of where your money goes after you die is more expensive.

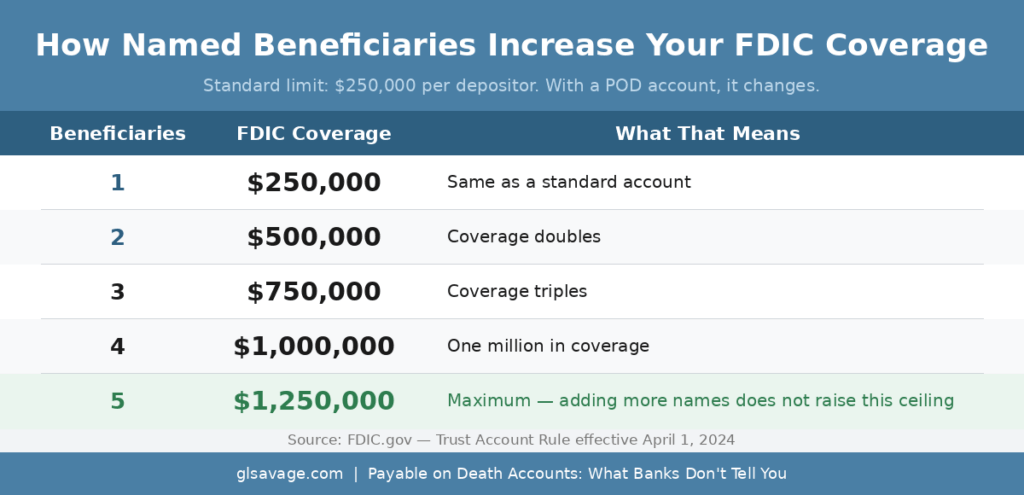

The FDIC Insurance Benefit Almost Nobody Knows About

FDIC insurance is the protection that covers your bank deposits if the bank fails. The standard limit is two hundred fifty thousand dollars per depositor per bank. If you have more than that in a single account at a single bank, the amount above the limit is not insured.

Here is what changes with a payable on death account. When a bank account has named beneficiaries, the FDIC insures the account at two hundred fifty thousand dollars per beneficiary. Name two beneficiaries and the coverage goes up to five hundred thousand dollars. Name four and coverage reaches one million dollars. The coverage maxes out at five beneficiaries under the rules that took effect April 1, 2024. Beyond five beneficiaries, adding more names does not increase coverage further. The maximum for a single account owner is one million two hundred fifty thousand dollars.

For most people living paycheck to paycheck, this is not an immediate concern. But for anyone who receives a settlement, an inheritance, or a large sum that temporarily sits in a single account, knowing that naming beneficiaries increases your insurance coverage is the kind of practical information that most people never hear until it is too late to use it.

The solution is free. Name beneficiaries. Get the coverage. Tell the people you name that they are named.

When Someone Can Legally Challenge a POD Designation

A POD designation feels permanent once it is filed. It is not.

Like any legal document, a POD designation can be challenged in court. The grounds most commonly used are undue influence, fraud, and lack of capacity.

Undue influence means someone pressured the account holder into naming them when the account holder would not have done so freely. This comes up frequently with elderly people who are dependent on a caregiver or a particular family member. The pressure does not have to be dramatic. Subtle manipulation counts.

Fraud means the account holder was deceived. Someone told them they were signing one thing when they were actually signing something else, or gave them false information that led them to make a decision they would not have made with accurate information.

Lack of capacity means the account holder did not understand what they were doing at the time they signed the form. Dementia, severe illness, and certain medications can all be raised as evidence of incapacity.

These challenges do not always succeed. But they are real, they happen in court, and they can hold up the transfer of funds for months while the case is decided.

The practical protection against this is documentation. If you change a beneficiary designation, especially later in life, write down why. Date it. Keep it somewhere accessible. A simple handwritten note that says on this date I changed the beneficiary on my account at this bank from this person to this person, for these reasons, signed and dated, gives anyone defending the designation something concrete to work with. It costs nothing and it can make an enormous difference.

The Gap Nobody Talks About: What Happens If You Become Incapacitated

A stroke. Dementia. A serious accident. A medical crisis that leaves you unable to make decisions. These things happen, and they happen to people of all ages.

Your POD beneficiary has zero authority to help you while you are alive. They cannot call the bank on your behalf. They cannot pay your bills from your account. They cannot move money to cover your care. The payable on death designation gives them no power until you are gone. While you are incapacitated and still living, that account is legally unreachable to them.

If no one else has legal authority to access your accounts, the bank will not release funds to anyone. Not your spouse. Not your adult child. Not the person sitting next to you in the hospital. The account sits while bills pile up, while care costs accumulate, while life does not pause.

The legal tool that solves this is called a durable power of attorney. It is a document that gives a person you choose the authority to manage your financial affairs on your behalf while you are alive. It covers accessing bank accounts, paying bills, managing assets, and making financial decisions if you cannot. It is separate from a will, separate from a POD designation, and completely separate from anything that happens after death.

The word durable is the important part. A regular power of attorney becomes void if you lose mental capacity. A durable power of attorney stays in effect specifically because you have lost capacity. That is the version you need.

Most estate planning attorneys can prepare a durable power of attorney for a few hundred dollars. Some legal aid organizations offer them at reduced cost or free for people who qualify. Many states also have free statutory forms available online that, when properly signed and witnessed, are legally valid.

A payable on death designation handles what happens after you die. A durable power of attorney handles what happens if you cannot manage things yourself while you are still living. You need both. Most people have neither. For more on building the financial foundation that makes either option more survivable, Build an Emergency Fund Living Paycheck to Paycheck covers that side of the picture. And What Is a Beneficiary on a Bank Account? What Banks Don’t Tell You covers the broader beneficiary designation picture across all account types.

The Full Picture

A payable on death account is a genuinely useful tool. It keeps money out of probate. It gets funds to the right person quickly. It costs nothing to set up. For most people in straightforward situations, it works exactly as described.

But the financial industry sells it as simple because simple is easy to market. The Social Security clawback is not simple. The Medicaid estate recovery is not simple. The creditor exposure during life is not simple. The community property rules are not simple. The incapacity gap is not simple. None of those things are in the brochure.

You are not less capable of understanding these things than anyone else. You were just never told about them. That is the system working as designed, not a reflection of you. A payable on death account is a tool. You now know how it actually works. Use it.

Frequently Asked Questions About Payable on Death Accounts

What is a payable on death account?

A payable on death account is a bank account with a named beneficiary attached to it. The account owner keeps full control while alive. When the owner dies and the bank is notified, the beneficiary presents a valid ID and a certified death certificate, completes a claim form, and the funds transfer directly without going through probate.

Does a payable on death account avoid probate?

Yes, in most cases. A POD designation allows the funds to transfer directly to the named beneficiary without court involvement. However, bypassing probate does not eliminate all obligations. Creditors and Medicaid recovery programs can still reach POD funds in certain states depending on the circumstances.

Can creditors take money from a payable on death account?

During the owner’s lifetime, yes. A POD account is a regular bank account and can be garnished by a judgment creditor just like any other account. After death, it depends on state law. In states that allow it, creditors of the estate can pursue the beneficiary who received the funds if the estate does not have enough assets to cover its debts.

What is Medicaid estate recovery and can it affect a POD account?

Medicaid estate recovery is the process by which state governments recoup the cost of Medicaid long-term care from a deceased person’s estate. In a number of states, this recovery can reach beyond the probate estate and include payable on death accounts. If the deceased received Medicaid nursing home or long-term care benefits, the beneficiary should contact the state Medicaid agency before spending any POD funds.

What documents does a beneficiary need to claim a POD account?

The beneficiary typically needs a valid government-issued photo ID, a certified copy of the death certificate with an official seal, and a completed claim form provided by the bank. Each beneficiary must claim their portion separately. Some banks process this in a single visit. Others route it through an estate department and it takes a few business days.

What happens to Social Security payments that arrive after someone dies?

Social Security payments received after the date of death must be returned to the Social Security Administration. Banks are required to return these deposits when notified. If a POD beneficiary claims the account and spends funds that included a post-death Social Security deposit, the SSA can pursue repayment. Notify the SSA of the death as quickly as possible, ideally through the funeral home, and do not spend any funds that may have arrived after the date of death until you have confirmed the source.

How does a payable on death account affect FDIC insurance coverage?

Naming beneficiaries on a bank account increases FDIC insurance coverage. The standard limit of two hundred fifty thousand dollars applies per named beneficiary. Name two beneficiaries and coverage reaches five hundred thousand dollars. The coverage maxes out at five beneficiaries. As of April 2024, the maximum FDIC coverage for a single account owner with five or more beneficiaries is one million two hundred fifty thousand dollars. Adding a sixth or seventh beneficiary does not increase that ceiling.

Can a payable on death designation be challenged in court?

Yes. A POD designation can be challenged on grounds of undue influence, fraud, or lack of mental capacity at the time the form was signed. These challenges can delay the transfer of funds significantly. To protect against a challenge, document your reasoning when you make or change a designation, especially later in life. A dated, signed note explaining your decision gives any future legal defense something concrete to work with.

Is a payable on death account the same as a living trust?

No. A POD designation transfers money but cannot attach conditions to that transfer. A living trust can specify how and when funds are used, protect a beneficiary who is a minor or has special needs, and give the account owner more control over what happens after death. A POD account is a transfer tool. A trust is a planning tool.

What happens if the POD beneficiary dies before the account holder?

If the named beneficiary dies before the account holder and no contingent beneficiary is listed, the account typically falls into the estate and goes through probate. This is why naming a contingent, or backup, beneficiary matters. It is a five-minute addition that prevents the account from losing its probate-bypass benefit entirely.

What happens to a payable on death account if the owner becomes incapacitated?

The POD beneficiary has no authority to access the account while the owner is alive, even if the owner is incapacitated. The account is legally the owner’s until death. If no one else has legal authority to manage the account, it becomes inaccessible even while bills and care costs accumulate. The solution is a durable power of attorney, a separate legal document that gives a trusted person authority to manage financial affairs on the owner’s behalf if they become unable to do so themselves.

Does a payable on death account affect community property rights?

In the nine community property states, money earned during a marriage is generally owned equally by both spouses. An account holder in a community property state can only direct their half of the account through a POD designation. The surviving spouse may have a legal claim to their half regardless of what the POD form says. If you are in a community property state and want to name anyone other than your spouse as beneficiary, speaking with an estate planning attorney first is worth the time.