The cruelest thing about credit is that you need it to get it. You cannot qualify for a reasonable loan without a credit history. You cannot build a credit history without someone giving you credit first. If you have no score at all, lenders call you credit invisible, meaning the bureaus have nothing on file for you and most lenders will not touch the application. That is not a personal failing. It is a structure. And sitting inside that structure, aimed at people who are trying to break out of it, is an entire industry of products and services designed to look like solutions while quietly making the problem worse. If you want to build credit fast, whether you are starting from zero or rebuilding after bankruptcy, job loss, or a financial crisis, you need to know which tools actually work, which ones take your money while your score goes nowhere, and what the three credit bureaus are actually measuring. This article covers all of it, including the parts the industry would prefer you never find out.

Before You Do Anything Else: Check Your Credit Report for Errors

Most credit articles bury this at the end or skip it entirely. It belongs at the top, because for a significant number of people reading this, there are errors on their credit report right now that are actively suppressing their score, and no amount of building will fix a score that is being pulled down by information that is simply wrong.

A Federal Trade Commission study found that one in five consumers has an error on at least one of their three credit reports. Five percent had errors serious enough to cause a credit denial or force them into a higher interest rate. People who have been through financial hardship, dealt with debt collectors, or had accounts go to collections are statistically more likely than average to have errors sitting on their reports right now.

You are legally entitled to a free report from all three bureaus every single week, permanently, at AnnualCreditReport.com. Not once a year. Every week. Most people do not know this. Pull your reports before you do anything else.

Common errors to look for: accounts that are not yours, which can mean identity theft or a mix-up with someone who has a similar name; accounts showing as unpaid that you already paid or settled; the same debt listed more than once under different collection agency names, which happens when a debt gets sold between collectors; negative items that are past their seven-year limit and should have already fallen off; and wrong personal information like an old address or a misspelled name.

If you find an error, you have a federal legal right to dispute it under the Fair Credit Reporting Act. You do not need to pay anyone to do this.

Here is what the industry does not advertise about how the dispute process actually works. When you file a dispute, the bureau does not investigate it themselves. They convert your dispute into a two or three digit code and send it electronically to whoever reported the information in the first place. That is the same creditor or debt collector whose records probably contained the error. They check their own records and send back a response. The bureau accepts it, almost always without any independent review. The National Consumer Law Center has documented this system in detail.

Disputes do not always succeed. But they are worth doing. If the creditor cannot verify the information, the bureau is legally required to remove it. And if the error is not corrected after you dispute it properly, you have a legal claim under federal law. Attorneys who take these cases typically work on contingency, meaning you do not pay unless they win.

Dispute in writing, by certified mail with return receipt, not through the bureau’s online portal. The online portal limits what you can say and makes it easy for the system to reduce your dispute to a code and dismiss it. Send a detailed written explanation with copies of any documents that support your position. Keep copies of everything. The FTC has sample dispute letters available free at consumer.ftc.gov.

The Credit Repair Company Trap: Read This Before You Pay Anyone

When you are trying to build credit fast, ads for credit repair companies will find you. On social media, on podcasts, in your email. They promise to remove negative items, boost your score, and fight the system on your behalf. Some charge $50 to $150 a month. Some charge hundreds upfront.

Here is what the FTC has stated directly: anything a credit repair company can legally do, you can do yourself for free. Not most things. Everything. The tools are the same. The rights are the same. The timelines are the same. The only difference is whether you are paying someone $100 a month for access to things you already have.

What they cannot do, no matter what they promise: remove accurate negative information from your report. It is illegal. If a late payment actually happened, no company can make it disappear. If a credit repair company promises to remove accurate negative information, they are lying, planning to do something illegal, or both.

The red flags are specific: any company that asks for payment before doing any work; any company that tells you not to contact the credit bureaus yourself; any company that suggests disputing accurate information; any company that tells you to file a false identity theft report to remove a legitimate debt. Filing a false identity theft report is a federal crime. The FTC has taken action against dozens of operations running exactly these schemes.

If you want real help and do not want to navigate this alone, free legitimate help exists. Use the National Foundation for Credit Counseling’s agency finder at nfcc.org to locate an accredited nonprofit near you. They are not selling anything. They help you build a plan and work it.

What a Credit Score Is Actually Measuring

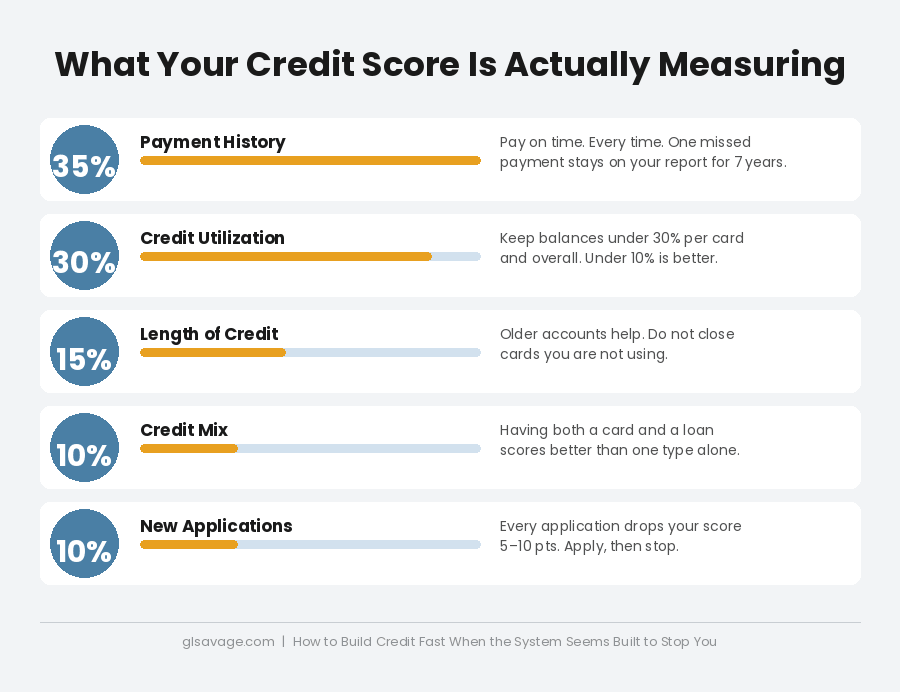

Three private companies you never chose are running the show. Equifax, Experian, and TransUnion maintain files on your financial behavior. Those files get turned into a number between 300 and 850. Lenders use that number to decide whether to give you credit and what interest rate to charge. The higher the number, the less they charge you. The system is not neutral and it is not designed in your favor. But it runs on specific, knowable inputs. Once you understand what those inputs are, you can work the system deliberately instead of being worked by it.

Whether you pay on time is the biggest piece, about 35 percent of your score. Every on-time payment is a point in your favor. Every late payment is damage, and the damage is not proportional to how late you were. One payment that goes 30 days late can drop your score 60 to 100 points. That is months of careful work erased in a single missed deadline.

How much of your available credit you are using is the second biggest piece, about 30 percent. The scoring system looks at this two ways: your overall balance across all cards combined, and each individual card on its own. So if you have five cards and four of them are at zero but one is maxed out, that single maxed card still hurts you, even though your overall picture looks fine. The target is under 30 percent on each card and in total. Under 10 percent is better. This is one of the fastest levers you can pull because it updates every single month.

How long you have had credit accounts for about 15 percent of your score. That means how old your oldest account is, how old your newest account is, and the average age of everything put together. This is why closing old accounts hurts you even when you are not using them, and why opening several new accounts at once hurts you. Both drag the average down.

The types of credit you have is about 10 percent. The scoring system likes to see that you can handle different kinds, a credit card and a loan, not just one or the other. You do not need every possible type, but having only one leaves points on the table.

New applications for credit make up the last 10 percent. Every time you apply, the lender runs a check on your report. That check temporarily drops your score 5 to 10 points, and the record of it stays on your report for two years. Multiple applications in a short period look like financial stress. Apply for what you need, then stop.

Five factors. Each one measurable. Each one movable. That is the whole game. Everything else the credit industry sells you is built around the assumption that you do not know this. For a plain-language breakdown of the full picture, Credit Scores Explained Without the BS covers exactly that.

How to Build Credit Fast: The Tools in Order of Speed

Not all credit building tools work at the same speed. Here is the order that builds fastest, from quickest impact to slowest.

Authorized User: The Fastest Single Move

If you know someone with a credit card that has a long history of on-time payments and a low balance, asking them to add you as an authorized user is the single fastest way to build credit available to most people.

When they add you, the full history of that account often appears on your credit report as if it were your own. If the account owner has had the card for 11 years with no late payments, your report now shows an 11-year-old account with no late payments. Your average account age jumps. Your payment history improves. Your score can move significantly within one to two billing cycles.

You do not need to use the card. You do not need the physical card in your possession. Being listed on the account is enough for the history to transfer. The account owner takes on no risk from adding you as long as they do not give you the card to spend with.

The limitation is that this requires someone with good credit who trusts you. Not available to everyone. But if that person exists in your life, this is the first move to make, not the last. It costs nothing, requires no application, and does not trigger a credit check on your report.

One thing to verify first: not every card company reports authorized user history to all three bureaus. Ask the account owner to confirm with their card company before assuming the benefit will show up on your report.

Secured Credit Cards: The Right Kind and the Wrong Kind

A secured credit card works like this. You put down a deposit, usually $200 to $500, and that deposit becomes your spending limit. You use the card for small purchases, pay the balance in full every month, and the card company reports your payment history to the three credit bureaus. Over time that history builds your score. After 6 to 18 months of responsible use, most card companies return your deposit and upgrade the account to a regular card.

That is how it is supposed to work. Here is where it goes wrong.

Some secured cards are designed specifically to take money from people who are desperate to build credit while doing as little as possible for their score. The National Consumer Law Center calls these fee-harvester cards. They come with a $250 limit, a $75 application fee, a $50 annual fee, a $10 monthly maintenance fee, and additional charges on top. By the time the fees clear, your $250 limit has about $72 in actual spending power. You are paying to borrow your own money at a fraction of what you put in.

How to tell the difference before you apply: no application fee to open the account; no annual fee, or a low one under $40 with no monthly maintenance fee stacked on top of it; reports to all three bureaus, because reporting to only one or two builds less history than it should; and a clear path to get your deposit back and upgrade to a regular card after 6 to 12 months of on-time payments.

The Discover it Secured Card meets all of these criteria and charges no annual fee. The OpenSky Secured Card does not require a credit check to apply, which matters if your credit is damaged enough that other applications are being denied. Both report to all three bureaus.

Avoid any card that shows up in your mailbox or email marked “pre-approved” with a stack of fees attached. Pre-approved for a $250 limit with $170 in first-year fees is not an opportunity. It is a trap dressed as one.

One more thing most people never hear. The balance that gets reported to the credit bureaus is your balance on the day your statement closes, not the day your payment is due. Those are two different dates, usually a week or two apart. If you spend $200 on a $500 limit card and do not pay it down before the statement closes, the bureau sees 40 percent utilization, meaning you are using 40 percent of your available credit. Pay it down to $40 before the statement closes and the bureau sees 8 percent. Same card. Same month. Pay before the statement closes, not just before the due date. The difference between a $490 balance and a $40 balance on that same card is also the difference between a damaged score and a rising one. If you are carrying balances right now and wondering why your score is not moving, Minimum Payments Keep You in Debt. That Is Not an Accident. covers exactly that.

Credit Builder Loans: The Tool Most People Have Never Heard Of

A credit builder loan is the opposite of a standard loan, and that is exactly what makes it useful for people who cannot qualify for one.

With a standard loan, the bank gives you money and you pay it back. With a credit builder loan, you make the payments first and get the money at the end. You apply through a credit union or community bank, get approved, and make fixed monthly payments for 6 to 24 months. That money sits in a savings account you cannot touch until the loan is paid off. When it is done, you get the full amount minus any interest. The lender reports every payment to the bureaus the entire time.

The result is a clean loan payment history on your report, a small amount of savings you did not have before, and a score that has been building the whole time. Credit unions typically offer these for $300 to $1,000 at interest rates between 6 and 16 percent. On a $500 loan at 10 percent over 12 months, the total interest is about $28. That is a reasonable cost for a year of loan payment history on your report.

If you cannot find one at a local credit union, Self Inc. offers credit builder loans online, reports to all three bureaus, and has monthly payment options starting around $25. Not as cheap as a credit union but accessible when a local option is not available.

Before you apply anywhere: confirm the lender reports to all three bureaus. Some only report to one or two.

Rent and Utility Reporting: Free Credit Building You Are Already Leaving Behind

If you pay rent every month you are making one of the largest recurring payments in your life. In most cases none of it shows up on your credit report. Your landlord takes the payment. The bureaus never hear about it.

Experian Boost is free and lets you add on-time utility, phone, and streaming payments directly to your Experian file. It only affects your Experian score, not all three, but it costs nothing and takes ten minutes. Rent reporting services like Rental Kharma and LevelCredit report your rent to one or more bureaus for $6 to $10 a month.

The downside is essentially zero. If you are paying these things anyway, there is no reason not to get credit for them.

Co-Signer: Faster Access, Real Risk

A co-signer is someone with good credit who agrees to sign a loan alongside you. Their credit history backs your application. The loan shows up on both your report and theirs, and your payment history builds your score exactly like any other loan would.

The risk needs to be stated plainly. If you miss a payment, it damages the co-signer’s credit, not just yours. If you stop paying, they are legally responsible for the full debt. This ends friendships and strains families regularly. Do not ask someone to co-sign unless you are completely certain you can make every payment, and make sure they fully understand what they are agreeing to before they sign anything.

Store Cards and Credit Building Debit Cards: Last Resort Tools

Store credit cards, the kind that only work at one retailer, are easier to get approved for than regular cards. Interest rates are typically 25 to 30 percent. Used correctly, meaning one small purchase a month paid in full, they do report to the bureaus and build payment history. Treat them as a last resort if a secured card is not accessible, and never carry a balance on a 28 percent card for any reason.

Products like the Extra Debit Card connect to your bank account and report debit spending to the bureaus. The impact is generally smaller than a secured card and fees vary. If a secured card is accessible to you, start there. These products are for people who have exhausted that option.

How to Build Credit Fast When Your Score Is Already Damaged

Rebuilding damaged credit takes longer than building from scratch, but the tools are identical. The difference is that you are fighting against negative marks already on your report while adding positive ones. A late payment stays for seven years. A collection account stays for seven years from the date the debt first went unpaid. A bankruptcy stays for seven to ten years depending on the type. For a full breakdown of how collection accounts work and what they do to your report, read How Collection Accounts Affect Your Credit Report.

What changes over time is how much those marks hurt you. A late payment from five years ago does far less damage than one from six months ago. Recent positive behavior actively outweighs old negative marks in how the score is calculated. Consistent on-time payments for 12 to 18 months can produce real improvement even with older negative items still on the report.

Do not wait for old marks to age off before starting to build. Start now. The clock on those marks runs whether you are building or not.

How to Rebuild Credit After Bankruptcy

Bankruptcy does not end your ability to build credit. It restarts it. Chapter 7 stays on your report for ten years. Chapter 13 stays for seven. But the scoring impact fades significantly over time, and you can start rebuilding the day your discharge is final. That is the court order that wipes out the eligible debts and officially closes the case.

The tools are the same: a secured card, a credit builder loan, on-time payments on everything going forward. Many people find their score begins to recover meaningfully within 12 to 18 months of discharge because the debt that was destroying their score is gone and new positive history is being added on top of it.

The key mistake to avoid after bankruptcy is taking on new credit too quickly, especially high-interest products that make the financial situation worse. Build slowly. Let the positive history accumulate. The bankruptcy hurts less with every passing year of clean history on top of it.

Paying Off Old Collections: What Actually Happens

Most people assume that paying a collection account removes it from their report. It does not. Paying changes the status from unpaid to paid, which is slightly better under newer scoring models. But the account stays on your report for seven years from the date the debt first went unpaid, regardless.

What you can try before you pay is called pay for delete. You contact the collection agency in writing and offer to pay the balance in exchange for them removing the account from your report entirely. Some agencies agree. Many will not. There is no law requiring them to do it. But it costs nothing to ask. Get any agreement in writing before you send a single dollar. A verbal agreement means nothing.

Before you pay any collection: verify the debt is actually yours, the amount is correct, it has not already passed the seven-year mark, and it has not passed the statute of limitations in your state. The statute of limitations is the window during which a collector can legally sue you to collect the debt. That window is separate from the seven-year reporting window. Paying an old debt can sometimes restart that clock depending on your state’s laws. Know what you are dealing with before you pay anything. If the debt involves medical bills, the rules are different in ways most people do not know about. Read Medical Debt Is Different. Here Is How to Handle It. before you pay anything on a medical collection.

What Does Not Work Despite Being Everywhere

Some of the most common credit-building advice out there is either useless or actively harmful. Here is what to ignore.

Closing a credit card you are not using hurts your score. It reduces your total available credit and potentially shortens your credit history. Unless a card is charging you a fee you cannot justify, leave it open and use it occasionally to keep it active.

Applying for multiple cards or loans at once backfires. Every time you apply for credit, the lender runs a check on your report called a hard inquiry, and each one temporarily drops your score. Multiple checks in a short window signal financial stress. Open your building tools, then stop applying for anything until your score reaches its target.

Debit cards do not build credit. Responsible debit card use does not appear on your credit report at all. Only credit activity builds credit history. Along the same lines, Buy Now Pay Later services like Afterpay and Klarna have not historically affected credit scores, but newer scoring models are beginning to factor in that payment history. If you use these services and miss payments, those misses may start showing up in your score even if they never did before.

Paying off debt in full does not produce an immediate score jump. Paying down a high balance improves your utilization ratio, meaning the share of your credit limit you are carrying as a balance, which does help. But late payment history from the past stays on the report. The score reflects the full history, not just where things stand today.

How Long It Actually Takes to Build Credit Fast

Fast is relative. Building credit fast means using the right tools consistently and not making the mistakes that reset the clock. There are no shortcuts. There is no product that skips the waiting. There are only tools that work and tools that waste your time or take your money.

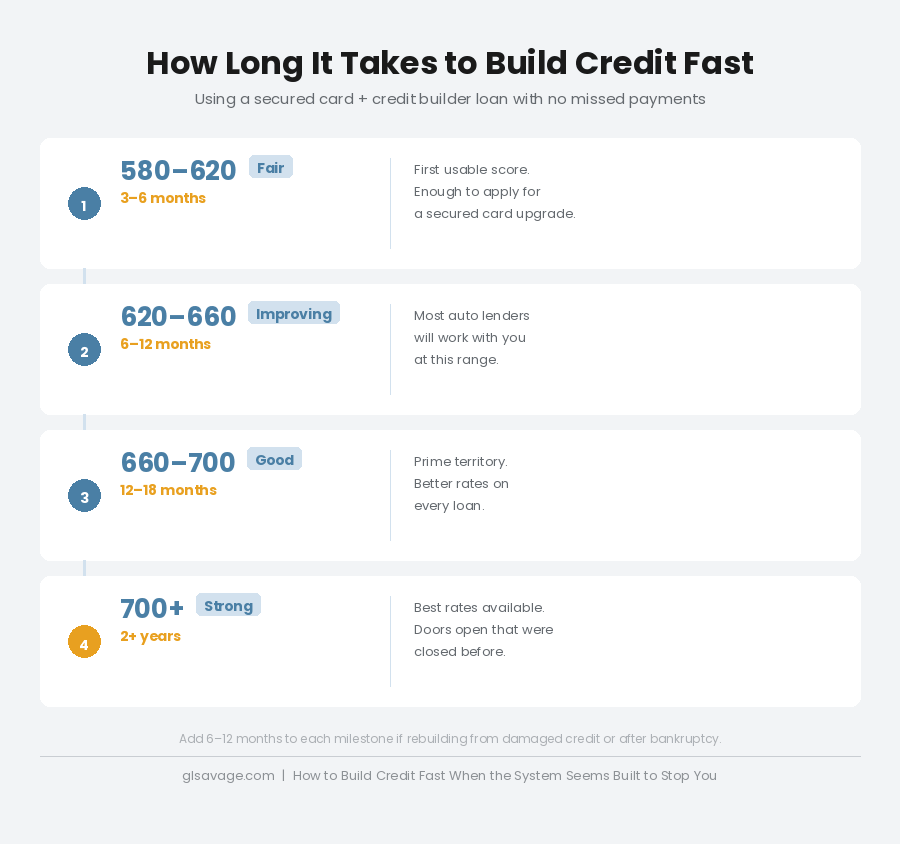

With a secured card, a credit builder loan, and consistent on-time payments, a score in the 580 to 620 range is achievable in 3 to 6 months from no credit history. Reaching 620 to 660 typically takes 6 to 12 months. Getting to 660 to 700 takes 12 to 18 months. Breaking 700 generally requires 2 or more years of consistent history. If you are rebuilding from damaged credit or after bankruptcy, add 6 to 12 months to each of those benchmarks.

The 660 threshold matters specifically if a car loan is part of what you are working toward. At 661 and above you cross into prime territory where interest rates drop significantly. The difference between a subprime rate and a prime rate on a $5,000 car loan is roughly $1,200 over the life of the loan. Eighteen months of work to get there is worth more than that number suggests, because once you cross that threshold, every loan for the rest of your life gets cheaper.

Protect What You Build

Building credit and destroying it can happen at the same time. The people who build fastest are not the ones who find the best products. They are the ones who stop making the mistakes that reset the clock. One late payment at the wrong moment can erase months of progress.

Set up automatic payments for at least the minimum on every account right now, before a busy month catches you off guard. You can always pay more manually. But automatic payments make sure nothing slips and costs you 60 to 100 points in a single billing cycle. One missed payment is not a minor setback. It is a seven-year mark on your report.

Keep your spending under 30 percent of your credit limit every month, and pay the full balance before the statement closes, not just before the due date. The day the statement closes is the day your balance gets reported. A $490 balance on a $500 limit card reported to the bureaus is damage. A $40 balance on that same card is progress. Same card. Same month. The timing is everything.

Do not close old accounts. An old account with no balance and no annual fee is free credit history. Closing it shortens your history and reduces your available credit at the same time. Leave it open. Use it once every few months to keep it active. That is all it takes. And while you are building, make sure you have a financial cushion underneath you. Build an Emergency Fund Living Paycheck to Paycheck covers how to do that without a lot of room to spare.

The System Is Not on Your Side. Work It Anyway.

The credit system is not designed to help people build credit fast. It is designed to extract money at every stage of the process, including the stage where you are trying to qualify for better terms. The fee-harvester cards exist because people with damaged or no credit have fewer options and the industry knows it. Used-car dealers who take your payments for years without reporting them to the bureaus exist for the same reason. The credit repair companies charging $100 a month for something you can do yourself exist because most people do not know they can do it for free. The bureaus built a dispute system that sends your complaint back to the same company that made the error. None of this is accidental.

What is also true: the tools that actually build credit fast are accessible, mostly free or close to it, and available to anyone who knows which ones they are. A secured card from a legitimate issuer. A credit builder loan from a credit union. An authorized user arrangement with someone who trusts you. Your own credit report, checked weekly for free, disputed in writing when something is wrong. These are not complicated tools. They are just not the ones being advertised to you.

You were not given a financial education. You were given a system that profits from you not having one. Now you have the information. Use it.

Frequently Asked Questions

Your first credit score appears after 3 to 6 months of activity on at least one account. With a secured credit card and a credit builder loan used correctly, most people reach a fair credit score in 6 to 12 months and a good score in 12 to 18 months. The timeline assumes no missed payments and balances kept under 30 percent of the available limit consistently.

The fastest combination is being added as an authorized user on an account with a long, clean history, opening a no-fee secured credit card that reports to all three bureaus, and taking out a credit builder loan from a credit union. Done at the same time, these three actions work on payment history, account age, and credit mix simultaneously, which is why the combination builds faster than any single tool alone.

Start with a secured credit card and a credit builder loan from a credit union. Both are accessible without any credit history. Use the card for one or two small purchases a month, pay the full balance before the statement closing date, and make every loan payment on time. If someone with good credit is willing to add you as an authorized user on their account, do that first. It is the fastest single move available for someone with no credit history and costs nothing.

The tools are the same as building from scratch: a secured card, a credit builder loan, and on-time payments on everything going forward. The timeline is longer because negative marks from the bankruptcy are on the report, but positive history you build now actively reduces their impact over time. Many people see meaningful score improvement within 12 to 18 months of their discharge, the court order that wipes out eligible debts and closes the case. Start immediately after discharge rather than waiting for the bankruptcy to age off, because that wait can be ten years.

No. The FTC has stated clearly that anything a credit repair company can legally do, you can do yourself for free. They cannot remove accurate negative information no matter what they promise. The tools are the same, the rights are the same, and the timelines are the same. The only difference is whether you are paying someone $50 to $150 a month for it. If you want guidance without the cost, free nonprofit credit counseling is available through agencies affiliated with the National Foundation for Credit Counseling at nfcc.org.

Look for accounts that are not yours, accounts showing as unpaid that you already settled, the same debt listed more than once under different collection agency names, negative items past the seven-year mark that should have already fallen off, and wrong personal information. You can check your reports for free every week at AnnualCreditReport.com. A Federal Trade Commission study found that one in five people has an error on at least one of their credit reports, and errors serious enough to cause a denial or force a higher interest rate affect about five percent of consumers.

A secured card requires a refundable deposit, usually $200 to $500, which becomes your spending limit. You use it for small purchases and pay the full balance every month. The card company reports your payments to the credit bureaus, building your credit file. After 6 to 18 months of responsible use, most issuers return the deposit and upgrade to a regular card. Choose one with no application fee that reports to all three bureaus, and avoid any card with monthly maintenance fees on top of an annual fee.

A credit builder loan reverses the standard loan structure. Instead of getting money and paying it back, you make payments first and receive the funds at the end of the term. Every payment is reported to the credit bureaus, building your loan payment history. Credit unions and community banks are the most common sources. If a local credit union is not accessible, Self Inc. offers a similar product online. Verify before applying that the lender reports to all three credit bureaus.

No. Paying changes the status from unpaid to paid, which is slightly better under newer scoring models, but the account stays on your report for seven years from the date the debt first went unpaid regardless. Before paying any collection, ask in writing for a pay for delete agreement, where they remove the account entirely in exchange for payment. Some agencies agree. Get it in writing before you pay anything. Also verify the debt is yours, the amount is correct, and that it has not already passed its seven-year mark or the statute of limitations in your state.

A co-signer is legally responsible for the full debt. If you miss a payment, their credit is damaged. If you stop paying, they owe the balance. This arrangement regularly damages relationships. Only ask someone to co-sign if you are fully certain you can make every payment on time for the life of the loan, and make sure they understand exactly what they are agreeing to before they sign.

There are multiple scoring systems and each of the three credit bureaus maintains its own file. FICO and VantageScore are the two main systems, and each has multiple versions. A lender might use your Experian FICO Score 8 while a free monitoring app shows your TransUnion VantageScore 3.0. For car loans, most lenders use a version called the FICO Auto Score, which weighs how you have handled auto loans in the past more heavily than the standard score. The direction of all your scores will be the same. The exact numbers will rarely match.