You already know the feeling. The bank charges you $35 because your account went $3 short. The car insurance bill goes up again and you cannot figure out why. The loan you needed came through, but the rate was brutal, and you signed because you had no other option. Each one of those moments felt like bad luck or bad timing. It was not. There is a name for what just happened to you, and it is called the poverty premium, some people call it the poor tax.

It does not show up as a line item on any bill. There is no single company running it. It is built into the structure of every financial system you already interact with, and it runs in one direction: the less money you have, the more everything costs.

It is not a coincidence. It is not bad luck. It is the system working exactly as designed, and it compounds. Every category where it hits you leaves less money to deal with the next one. Most of the people paying the most have no idea they are paying a premium at all. They think this is just what things cost.

Here is how the poverty premium works, where it hits hardest, and exactly what to do about it.

What Exactly is the Poverty Premium or Poor Tax?

The poverty premium, or poor tax, is the extra amount people with less money pay for the exact same things as people with more money. Same car loan. Same insurance coverage. Same box of detergent. More money out of pocket. Every time.

The financial system evaluates risk, and being poor is treated as a risk category. Not a hardship. Not a circumstance. A risk. And risk gets charged more. That is where the math starts, and it does not stop. Every category where the cost of being poor catches up with you leaves less money to handle the next one. That is not an accident. That is how the trap stays closed.

Where It Hits and How Much It Actually Costs

Payday Loans: The Worst Math in American Finance

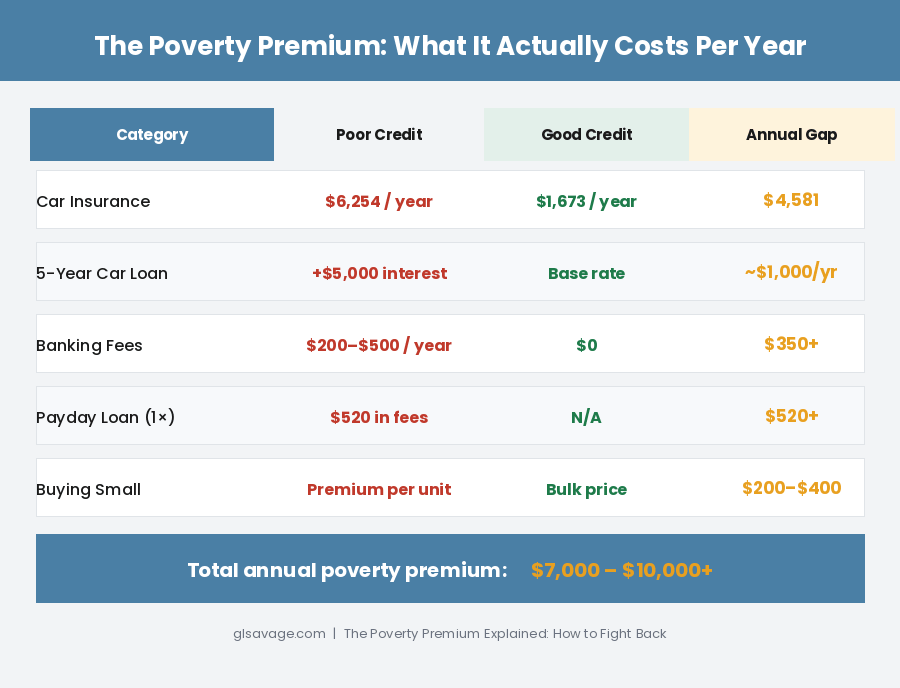

A typical payday loan charges around 391% per year. In some states it runs higher. The business model depends on people who cannot pay the full amount back in two weeks, which is most people who take one, so the loan rolls over and the fees keep running. Twenty states and Washington D.C. have capped rates, but if you do not live in one of them there is almost no legal limit to what you can be charged. The full picture, including a much cheaper alternative most people do not know exists, is at How Payday Loans Are Legal and What to Do Instead.

Loans and Credit: Paying More to Borrow the Same Money

Two people walk into a dealership. Same car. Same price. One has a good credit score and gets a low rate. The other had a bad year three years ago, fell behind on some bills, and now gets a rate two to three times higher. On a five-year car loan, that gap easily costs $4,000 to $6,000 extra in interest alone. On a 30-year home loan, it runs into the tens of thousands.

The credit score is not measuring whether you are a good person. It is measuring your history with a system that does not account for layoffs, medical bills, or bad timing. If you have ever fallen behind because of circumstances, that history follows you into every loan and every application for years. The system that helped create the hardship then charges you more because of it.

Car Insurance: Paying Double for the Exact Same Coverage

In most states, your credit score affects your car insurance rate more than your actual driving record does. Let that land for a second.

According to data from The Zebra, a driver with very poor credit pays an average of $6,254 a year for car insurance. A driver with excellent credit pays $1,673 a year. Same car. Same zip code. Same clean driving record. The only difference is the credit score. That is a gap of $4,581 every single year. Bankrate found the same pattern: drivers with poor credit pay roughly double what drivers with excellent credit pay for identical coverage.

This is not illegal in most of the country. Insurance companies say credit scores predict who will file claims. Whether that is true or not, the result is that someone who went through a financial hardship pays twice as much for something they are legally required to carry. Only California, Hawaii, Massachusetts, and Michigan have banned it. If you do not live in one of those four states, your credit score is affecting your insurance bill right now whether you know it or not. The full guide on pushing back on this specific bill is at Car Insurance Is a Rigged Game. Here Is How to Play It.

Banking: Paying Fees Just to Keep Your Own Money

If you do not have enough money to keep a minimum balance, the bank charges you a monthly fee for the privilege of banking with them. If your account runs low and a charge goes through anyway, they charge you an overdraft fee, often $35 or more, for a transaction that might have been $3. And if you do not have a bank account at all, because you cannot qualify or cannot afford the minimums, you pay a check-cashing service 2% to 5% of every paycheck just to access money you already earned.

This is what being unbanked or underbanked actually costs. Not inconvenience. Real money, every week, just to touch your own wages. Banks designed their fee structures this way deliberately. The accounts most likely to dip below minimums belong to the people who are already stretched thin. That is not a coincidence. That is the product. The full breakdown is at How Banks Make Money From Overdraft Fees and The Hidden Costs of Not Having a Bank Account.

Buying Small Because You Have To

For household staples like detergent, toilet paper, and cleaning supplies, buying in bulk almost always costs less. If you have the cash to buy in volume, you pay less. If you do not, you pay a per-unit premium on the same products every single week because you can only afford the small size. Invisible in any single purchase. Meaningful over a year. It is worth knowing which categories this actually applies to before assuming buying in bulk is always cheaper, because it is not always true. Is Buying in Bulk Cheaper? works through exactly where the savings are real and where the bulk price is a trap.

Rent-to-Own and Buy-Here-Pay-Here: Financial Exploitation Dressed Up as a Solution

These businesses exist specifically for people who cannot get credit anywhere else. No credit check. Low weekly payments. Drive today. Take it home now. What they do not show you is the total cost if you make every single payment, because that number is the whole game.

A $600 television rented to own at $30 a week for 24 weeks costs $720. The person who did not have $600 upfront pays 20% more for the exact same television. That is the mild version. Furniture, appliances, and electronics commonly end up costing two to three times what they would cost to buy outright.

Buy-here-pay-here car lots run the same structure on a bigger number with rates consistently higher than what any bank or credit union would charge the same person. But the financing is not even the worst part.

Many buy-here-pay-here dealers install GPS tracking devices and remote kill switches in the cars before selling them. If you miss a payment, or sometimes if you are just a few days late, they can disable the car remotely. Not repossess it. Disable it. Your car stops working while you are driving to work, while your kids are in it, while you are trying to reach a hospital. This is legal in most states. It happens regularly. The poverty premium here is not just the extra money you pay. It is the power they hold over you the moment you sign. You are not buying a car with bad financing. You are handing someone a switch that controls whether you can get to work tomorrow.

Renting vs. Owning: Why the Barrier Matters

Homeownership builds equity over time. But the barrier to getting there, the down payment, the credit score requirement, the two years of steady income history, keeps a lot of people locked out of it entirely. And while that barrier is still in place, rent keeps going up and nothing accumulates on the other side. Whether renting makes more sense than buying depends on your specific situation, and sometimes it genuinely does. But the poverty premium means the people who need the option of ownership most are the ones who have the hardest time accessing it. The full honest math on both sides is at Is It Better to Own or Rent? The Real Math No One Explains.

Medical Bills: The One That Can Undo Everything Else Overnight

Medical debt is the single largest cause of personal bankruptcy in the United States. It does not care whether you have insurance or whether you did everything right. One serious illness, one accident, one week in the hospital, and the bill that follows can be larger than a year of rent. Once it lands on your credit report, it feeds back into every other part of the poverty premium: higher loan rates, higher insurance costs, harder path to housing. One event, one bill, and years of careful progress can come undone. The rules around negotiating medical debt, billing errors, and hospital assistance programs that most patients are never told about are covered at Medical Debt Is Different. Here Is How to Handle It.

It Is Not a Hole. It Is a Current.

Higher costs make it harder to save. Without savings, every emergency becomes debt. Debt damages your credit. Damaged credit raises what you pay for insurance and loans. Higher bills make it harder to pay down the debt. The credit stays low. The costs stay high.

None of this requires a single bad decision to start. It runs on circumstance and then uses circumstance against you.

The financial world frames this as a personal failing. If you are doing well, you made good choices. If you are struggling, you made bad ones. That framing is extremely useful to the people running the system. It keeps the conversation on individual behavior instead of on structures that make financial stability expensive to build and easy to lose. The poverty premium charges the same rates to someone who did everything right and had a bad year as it does to someone who did not. It does not know the difference. Understanding that is not about making excuses. It is about knowing what you are actually up against. Why Your Credit Score Exists and Who It Actually Serves goes deeper on this.

What It Adds Up To

Run the numbers across insurance, loans, banking fees, and a single payday loan that rolls for a few months and the gap between what someone with good credit pays for the same life and what someone with damaged credit pays can clear $10,000 in a year. Every year. On the same income. Until something in the chain changes. That is the money that could have been the emergency fund, the down payment, the buffer that keeps the next bad week from becoming a two-year setback.

How to Fight Back

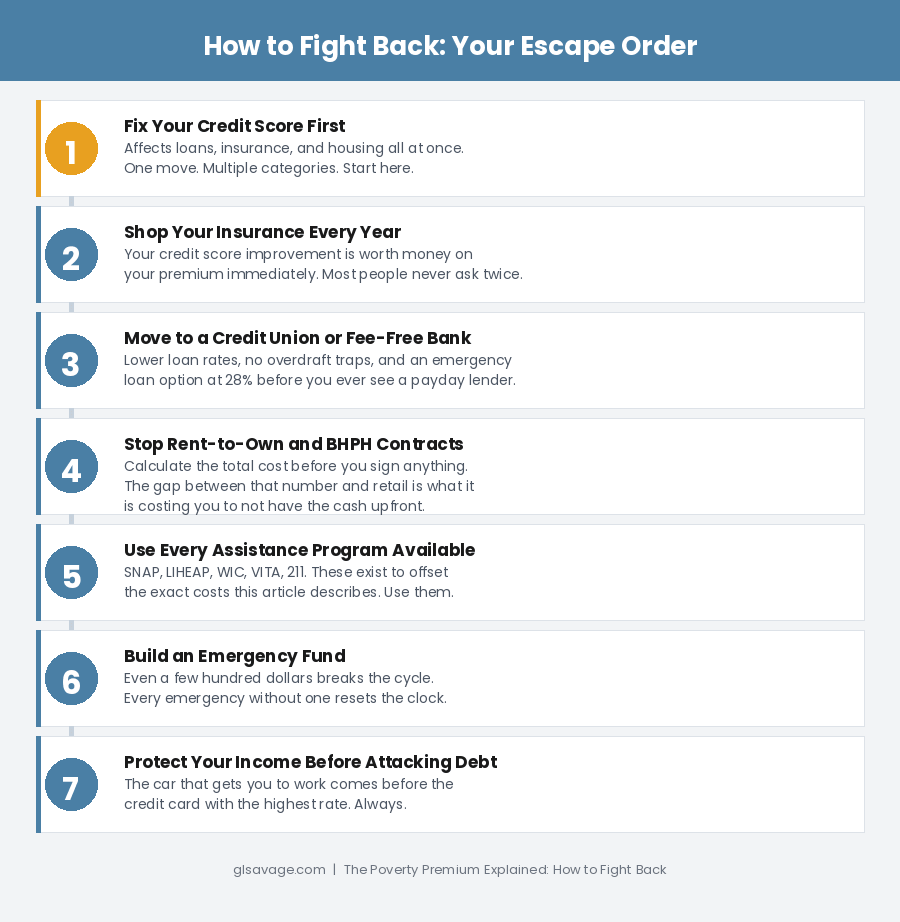

You cannot opt out. But you can reduce what it charges you, one category at a time. Some of these moves matter more than others because they fix multiple problems at once. Start with those.

Your Credit Score Is the Master Switch

Fix this first. It is the one lever that affects loan rates, insurance costs, and housing access simultaneously. Even moving one tier down from where it is right now saves real money across multiple categories at once. The return on improving your credit score, measured in actual dollars per year, is higher than almost any other move available to someone starting from a low number.

Pull your free credit reports at AnnualCreditReport.com. Every year. Errors are more common than people expect and every one costs real money. Dispute anything wrong in writing. Paying on time is 35% of your score and matters more than anything else you can do. Keep the balance on any credit card below 30% of the limit. Below 10% is better. If you have no credit or badly damaged credit, a secured card, where you put down a small deposit and get a card that reports to the bureaus, is the standard path back in. Use it for something small each month and pay it off in full. Do not close old accounts. Do not apply for several new ones at once.

For a plain-language explanation of what the score actually measures and what moves it, read Credit Scores Explained Without the BS. If you have collections on your report, How Collection Accounts Affect Your Credit Report covers what you can actually do about them.

Shop Your Insurance Every Single Year

Insurance companies do not reward loyalty. They count on it. The same driver with the same car and the same record can get quotes that differ by hundreds of dollars a year just by asking more than one company. Most people never ask more than one.

Get at least three quotes every year, not just when the renewal arrives. Any time your credit score improves, shop again immediately. That improvement is worth money on your premium right now. Start with comparison sites like The Zebra or Insurify, then call the top results directly. Ask specifically about every discount: defensive driving course, low mileage, paying the full year upfront, bundling. If you are in California, Hawaii, Massachusetts, or Michigan, they cannot use your credit score to set your rate. Everywhere else, assume they are.

Get Out of the Bank That Charges You to Stay

Credit unions are not-for-profit and owned by their members. They consistently offer lower rates on loans, fewer fees, and better terms than regular banks. Find one at MyCreditUnion.gov. Before you open anything, ask directly about minimum balance requirements, overdraft fees, and loan rates. If no credit union works for your situation, online banks like Chime and Ally have eliminated overdraft fees and minimum balances entirely. There is no reason to pay a bank monthly just to keep your money there.

And if you are ever in a spot where a payday loan seems like the only option, call your credit union first. A small emergency loan through a credit union is capped at 28% a year by federal law. That is not the same universe as 391%.

Never Sign a Rent-to-Own or BHPH Contract Without Doing This First

Before you sign anything rent-to-own, add up every payment you would make and write down the total. Then look up what that item costs to buy outright. The gap between those two numbers is what not having the money upfront is costing you. For furniture and appliances, Facebook Marketplace and thrift stores carry the same things regularly for a fraction of retail. Paying cash for a used version almost always beats financing a new one at rent-to-own rates.

For cars, a credit union will give you a better rate than a buy-here-pay-here lot for the same vehicle, even with damaged credit. Get that quote first. And remember what comes with BHPH financing in many cases: a kill switch. That is not a deal. That is a trap with a payment plan attached.

Use Every Program That Exists to Offset This

SNAP helps with food costs. LIHEAP helps with utilities and is worth applying for before the worst of winter or summer, not during a crisis when the wait lists are longest. WIC covers specific food costs for qualifying women, infants, and children. VITA provides free tax preparation through the IRS for people under the income limit. A paid preparer for a basic return costs $200 to $300. VITA costs nothing.

211.org connects you to local resources for food, housing, utilities, and more in one place. A library card is still one of the most overlooked tools available: free books, audio-books, streaming services, and in many areas museum passes and tool lending. For utility assistance specifically, Utility Bill Assistance Programs Nobody Tells You About covers what is out there and how to get it.

Build a Buffer Before the Next Emergency Hits

Every emergency resets the clock. One car repair, one medical bill, one week of missed work, and everything slowly improving goes straight back into debt. An emergency fund is not a luxury. It is the only thing that breaks that cycle. Even a few hundred dollars sitting somewhere untouched changes what a bad week does to you. How to build one when there is nothing left over at the end of the month is here: Build an Emergency Fund Living Paycheck to Paycheck.

Protect Your Income Before You Attack Your Debt

Here is the thing almost nobody in personal finance will tell you, and it might be the most important idea in this entire article.

The standard advice is to list all your debts, find the one with the highest interest rate, and throw every extra dollar at it. Personal finance people call this the avalanche method. Financially, on paper, in a stable situation, the math is correct. In real life, for a lot of people, following that advice is a serious mistake.

Your income is not guaranteed. It depends on your ability to get to work, stay employed, and keep the basic infrastructure of your life functioning. If your car breaks down and you cannot get to work, you do not just lose one day. You lose your job. And once you lose your job, every debt on that list becomes a crisis at the same time.

A car payment, a repair loan, car insurance, the phone you need for work: these are not just debts. They are the things your income runs on. Paying off a high-rate credit card while your car sits broken in the driveway is not a smart financial move. It is a mistake that costs you everything else.

Protect your income first. Before you look at interest rates, identify every debt and expense directly connected to your ability to earn. Those get paid first, no matter what the interest rate on anything else says. Pay the minimum on everything else, then direct extra money toward whatever creates the most stability in your specific situation, not whatever a spreadsheet says costs the most.

There is also a version of this that involves knocking out one small debt entirely just to free up a monthly payment. Getting a $400 balance with a $40 minimum off your plate permanently frees up $40 every month forever. The math works even when the interest rate is not the highest on the list. How minimum payments are structured to keep you in debt by design is worth understanding: Minimum Payments Keep You in Debt. That Is Not an Accident.

This Is Working Exactly as Intended

The poverty premium is not a flaw in the system. It is not an oversight anyone is trying to fix. The financial system prices risk, low income is classified as a risk category, and the pricing follows from there. Every piece of it is functioning as designed.

The steps in this article do not fix the system. They reduce what the poverty premium charges you inside it. Every category where you fight back leaves more money to take on the next one. That is how you build momentum against something designed to prevent exactly that.

This is not about getting rich. It is about stopping the bleed.

Frequently Asked Questions

The poverty premium is the extra amount people with less money pay for the same things as people with more money. It shows up in loan rates, car insurance, bank fees, and everyday purchases. It is one of the main reasons the cost of being poor compounds over time, and it hits multiple categories at once.

It is real and it is documented. The financial system charges people with lower incomes more for the same products regardless of what choices they make. Credit-based insurance pricing, overdraft fees, minimum balance requirements, and payday loan structures all operate this way by design. That said, some of the moves that reduce what it costs you are things you can control. Both of those things are true at the same time.

Improving your credit score has the widest effect because it reduces what you pay for loans, car insurance, and sometimes rent all at once. It costs nothing to start. It requires consistent behavior over time, not money. Even a moderate improvement reduces costs across multiple categories simultaneously.

Insurance companies say credit scores predict how often someone will file a claim, and most states allow them to use that in their pricing. The result is that someone who went through a financial hardship pays more for coverage than someone who never has, even if their driving records are identical. California, Hawaii, Massachusetts, and Michigan have made the practice illegal. Most other states have not.

A payday alternative loan is a small emergency loan offered by federally insured credit unions. The rate is capped at 28% per year by law. Loan amounts typically run $200 to $1,000 with repayment terms of one to six months. You need to be a member of the credit union to apply. This option exists before the payday lender does. Most people do not know it is there until someone tells them.

Yes. Most credit unions have no minimum balance requirements and charge far fewer fees than regular banks. Online banks like Chime and Ally have eliminated overdraft fees entirely. There is no reason to pay a bank monthly just to keep your money somewhere.

Yes. Because it runs on credit score and income level, and because access to credit and the ability to build savings have historically been unequal across racial and economic lines, the poverty premium falls harder on lower-income communities and communities of color. The mechanism is the number on the credit report, but that number did not appear in a vacuum.