Wage garnishment is built to catch you off guard. The system that makes it possible moves fast, stays quiet, and counts on you not knowing how it works until the money is already gone. One payday you get a full check. The next, a chunk of it is missing. Your employer did not make a mistake. A court told them to do it. And in most cases, the window to stop that from happening closed weeks or months earlier, while you had no idea it was even open. The debt collection industry, the court system, and the creditors who buy up old debt all benefit from you staying in the dark. This article is about what they are not telling you.

What Wage Garnishment Is and How It Actually Works

Wage garnishment is when a court orders your employer to withhold part of your paycheck and send it directly to a creditor. Your employer has no choice. Once that order arrives, they are legally required to comply with it, usually starting with your very next paycheck. The money never reaches your bank account. It goes from your employer straight to whoever is collecting.

Garnishment can apply to wages, salaries, commissions, bonuses, and in some cases pension and retirement payments. The legal term for what can be taken is “disposable earnings,” which sounds like spending money but actually means something specific: what is left over after legally required deductions like taxes and Social Security are taken out. It does not mean what is left after your rent, groceries, or car payment. Those do not count.

Here is the part the system does not explain clearly. Wage garnishment is almost never the first move a creditor makes. It is the last move. Getting there requires a specific chain of events, and that chain has a window where you could have changed the outcome. Most people miss that window entirely because they do not know it exists.

The Chain That Leads to Your Paycheck Getting Docked

This is the step-by-step reality of how wage garnishment actually happens. Most people find out after the fact. Here is what actually happened before that check came up short.

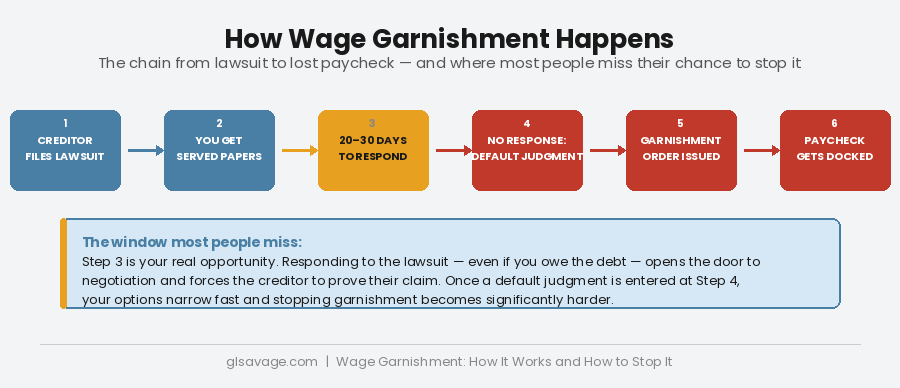

A creditor files a lawsuit against you. You get served with papers, either in person, by mail, or by another method depending on your state. Those papers tell you that you are being sued and give you a deadline to respond, typically 20 to 30 days depending on where you live.

Most people throw those papers away. They look like junk mail. They arrive during a stretch when money is already short and a court summons feels like one more problem too many. Some people assume that ignoring it makes it go away. It does not. When you do not respond by the deadline, the court enters a default judgment. That means the creditor wins automatically, without ever having to prove their claim in front of a judge. You were not there to contest anything, so the win is handed to them.

A default judgment is exactly what it sounds like. You lost by default. And it happens constantly. The overwhelming majority of debt collection lawsuits result in default judgments because most people who are sued for debt do not respond. The creditors know this. They count on it. It is not a coincidence that the papers look like junk mail and arrive with no explanation of what is at stake if you ignore them.

Once they have that judgment, they go back to court and request a wage garnishment order. The court approves it and notifies your employer. In some states that process can begin as quickly as ten days after the judgment. In others it takes a few weeks. Either way, once it starts, it runs every single pay period until the debt is paid in full or you do something to stop it.

The judgment does not just cover what you originally owed. It can also include the creditor’s court costs, attorney fees, and interest that has been accumulating the entire time. You may owe significantly more than the original balance by the time garnishment begins, and the interest continues accruing while garnishment is in progress.

How Much Can Actually Be Taken From Your Paycheck

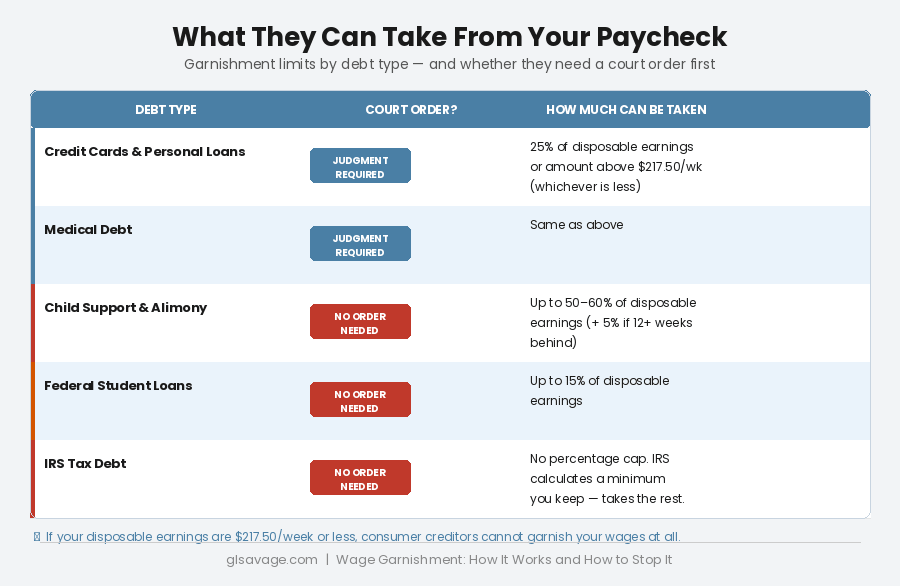

Federal law sets a ceiling on how much can be garnished for most consumer debts. The rule is the lesser of two amounts: 25 percent of your disposable earnings for that pay period, or the amount by which your disposable earnings exceed 30 times the federal minimum wage. The federal minimum wage is $7.25 an hour, which has not moved since 2009. Thirty times that is $217.50 a week. If your disposable earnings are at or below $217.50 a week, they cannot be garnished at all for consumer debt.

To put that in real terms: if your take-home pay after taxes and legally required deductions is $400 a week, 25 percent of that is $100. The amount above $217.50 is $182.50. The garnishment limit is whichever of those two figures is smaller. In this case, $100 per week comes out of every paycheck until the debt is gone. That is not a one-time hit. It is recurring, every single pay period, until the creditor is fully paid.

Some states set stricter limits than the federal ceiling. When state law is more protective, the state rule applies. Four states, North Carolina, South Carolina, Pennsylvania, and Texas, prohibit wage garnishment for consumer debts entirely under most circumstances. If you live in one of those states and your debt is a credit card, medical bill, or personal loan, your paycheck is generally protected. Your bank account is a different matter entirely, which is covered below.

The rules change significantly for certain types of debt. Child support and alimony can take up to 50 percent of your disposable earnings, or up to 60 percent if you are not currently supporting another spouse or child. If you are more than 12 weeks behind on support payments, an additional 5 percent can be added on top of that. Federal student loans can take up to 15 percent without needing a court order at all. The IRS uses its own formula based on your filing status and number of dependents, and unlike consumer creditors, it faces no percentage cap. It simply calculates a minimum amount it must leave you with each week and takes everything above that.

The Debts That Skip the Courthouse Entirely

Most private creditors cannot touch your wages without going through court first. They have to sue you, win a judgment, and get a separate garnishment order. That process takes time, and that time is your window to act.

Certain government debts skip that process entirely. Federal student loans, back taxes owed to the IRS, and child support can all trigger wage garnishment without a court judgment. These agencies have what is called administrative garnishment authority. They can go directly to your employer after following their own required notice process, no lawsuit needed.

For federal student loans, the Department of Education must give you at least 30 days’ written notice before garnishment starts. You have the right to request a hearing within that window to challenge the garnishment or propose a repayment plan. If you request that hearing on time, garnishment cannot begin until the hearing is resolved. That is a real protection, but you have to use it. Ignoring the notice has the same result as ignoring a court summons. The process moves forward without you.

On the student loan front specifically: the Department of Education announced plans to resume wage garnishment for defaulted federal student loan borrowers in January 2026, then reversed course and announced a temporary delay on January 16, 2026, with no new restart date set at that time. As of this writing, that delay remains in place, but it is temporary. More than five million borrowers are currently in default. If your federal student loans are in default, the pause is not a resolution. Contact your loan servicer now about rehabilitation or consolidation. Those are the two paths out of default that can stop garnishment before it starts.

Your Employer Cannot Fire You. With One Specific Exception.

Federal law under the Consumer Credit Protection Act says your employer cannot fire you because your wages are being garnished. That protection exists and is real. But it covers only a single garnishment. If two separate wage garnishment orders arrive from two separate creditors, that protection disappears. Federal law allows your employer to terminate you when your wages are subject to garnishment for more than one debt.

This is one of the most consequential and least discussed details in this entire subject. It matters most to people dealing with multiple debts at the same time, which is exactly the situation most people facing garnishment are in. If you have multiple creditors pursuing you, resolving at least one before garnishment orders start stacking is not just about the money. It is about keeping your job.

Some states offer stronger protections on this point. Check the laws in your state. But do not assume the federal protection covers multiple garnishments. It does not.

The Bank Account Trap Nobody Warns You About

Social Security, disability benefits, veterans’ payments, and other federal benefits cannot be garnished as income by private creditors. That protection is written into federal law. But it comes with a catch that trips up a lot of people who believe they are covered.

Once those payments land in your bank account, different rules apply. A creditor who wins a court judgment can pursue what is called a bank levy, which is a seizure of funds directly from your account. If your Social Security or disability payments are mixed in with other money, or if your balance has grown beyond two months’ worth of protected deposits, the excess can be taken.

Federal law requires banks to automatically protect two months’ worth of directly deposited federal benefits. But that automatic protection only applies if you receive those benefits by direct deposit. If you cash checks or deposit them by hand, you may have to claim the exemption yourself through the court. And two months is the ceiling of protection, not a guaranteed floor. Anything above two months of those deposits is potentially exposed.

The practical answer is specific. If you live primarily on Social Security, disability, or similar federal benefits, keep those funds in a dedicated account separate from any other money you receive. Receive them by direct deposit. Do not let the balance grow significantly beyond what you need month to month. These three steps are the practical difference between money that is protected and money that a judgment creditor can reach.

Judgment Proof: The Status Most People Who Qualify Have Never Heard Of

There is a legal concept that applies to a large portion of the people most likely to face debt collection lawsuits, and most of them have never heard of it. It is called being judgment proof, sometimes called collection proof, and understanding it could change how you respond to an entire situation.

Being judgment proof means that even if a creditor sues you, wins, and gets a garnishment order, there is legally nothing collectible. Your income is too low or comes entirely from protected sources. You have no significant assets for them to seize. A court judgment against you is a piece of paper they cannot enforce.

Under federal law, if your weekly disposable earnings are $217.50 or less, they cannot be garnished at all for consumer debt. If your only income is Social Security, disability, veterans’ benefits, or similar protected federal payments, private creditors cannot garnish it. If you have no significant property, no home equity, no savings worth targeting, a creditor with a judgment against you has essentially nothing to collect on.

This does not make the debt disappear. Judgments in most states are valid for ten years and can often be renewed. If your financial situation improves, a creditor can come back and try again. But if you are in that position right now, knowing it means you do not need to agree to a payment plan you cannot sustain, you do not need to file for bankruptcy unnecessarily, and you do not need to live in fear of a garnishment that legally cannot reach you.

You can notify a creditor of your judgment proof status in writing. Many creditors will not pursue a lawsuit against someone who clearly has nothing collectible, because filing a lawsuit costs them money. A nonprofit legal aid organization can help you evaluate your situation and draft that communication. Find free legal help through the National Legal Aid and Defender Association at nlada.org.

What You Can Still Do Once Garnishment Has Started

Stopping a garnishment already in motion is harder than preventing one. The system is built that way. But harder is not impossible, and real options exist even at this stage.

File a claim of exemption. Many states let you challenge a garnishment if your income is protected by law or if the garnishment creates severe financial hardship. You file paperwork with the court, there is a hearing, and the court can reduce or stop the garnishment if your case holds up. You will need to document your income, your expenses, and the specific hardship. Contact your local court clerk or a nonprofit legal aid organization for the forms your state requires. Free help with this exists in every state.

Negotiate directly with the creditor. Creditors often prefer a reliable, consistent payment over the ongoing administrative burden of maintaining a garnishment order. Even after a judgment is entered, many will settle for less than the full amount or agree to a structured payment plan in exchange for releasing the garnishment. Get any agreement in writing. Make sure it explicitly states that the garnishment order will be released when you comply with the terms. Verbal agreements with creditors are not worth acting on.

Challenge the judgment. If you were not properly notified of the lawsuit, if the debt is not yours, or if the amount is wrong, you may be able to have the default judgment vacated. Debt buyers who purchase old accounts for pennies sometimes use outdated addresses or improper service methods. If that happened in your case, it is grounds to have the judgment thrown out and start over. Time limits apply, generally ranging from six months to two years depending on your state and circumstances. Move quickly if you believe this is your situation.

File for bankruptcy. Filing triggers an automatic stay, a legal halt on all collection activity including active wage garnishment, effective immediately upon filing. Chapter 7 can discharge most consumer debt entirely. Chapter 13 creates a repayment plan. Bankruptcy has real consequences for your credit and is not a first step, but for people buried under multiple garnishments and debt they cannot manage, it is sometimes the clearest path forward. Many bankruptcy attorneys offer free consultations.

How to Stop It Before It Starts

The moment you have the most power is the moment most people do the least with it. When those court papers arrive, responding is the single most important thing you can do.

Respond to the lawsuit. Even if you owe the debt, filing a response to the court forces the creditor to actually prove their claim and opens the door to negotiation. You can contact the creditor before the court date and often arrange a payment plan that stops the lawsuit from going further. Once you respond, the creditor knows they have to show up and make their case. Many debt buyers, the companies that purchased your old account for pennies on the dollar, would rather settle than go through that process. They bought the debt cheap precisely because collecting on it is uncertain. Use that.

Do not assume the debt amount in the lawsuit is accurate. Debt that has been sold through multiple collection agencies frequently arrives with errors in the balance, the account holder’s name, the dates, or the name of the original creditor. You have the right to request written verification of the debt before paying or admitting anything. Errors happen more often than most people expect, and an error in the debt documentation is grounds to challenge the claim entirely.

Free legal help exists. Nonprofit legal aid organizations in every state assist with debt collection lawsuits at no cost. The National Legal Aid and Defender Association can connect you with services in your area. Consumer law attorneys who handle cases under the Fair Debt Collection Practices Act, the federal law that governs how collectors must behave, often work on contingency, meaning you pay nothing unless they recover money for you. If a debt collector violated that law in pursuing the debt, which happens more often than most people know, their violation can end up covering your legal costs entirely.

Wage garnishment is designed to move fast and stay invisible until it is too late. The system does not notify you of your rights. It does not explain exemptions. It does not warn you that ignoring a lawsuit means handing the creditor an automatic win. That is not an oversight. The people who profit from wage garnishment depend on most people not knowing any of this. Now you do. If you are dealing with debt collectors right now, The Debt Collector Is Not Who You Think It Is covers the full picture of who is actually calling and what power they really have.

Frequently Asked Questions About Wage Garnishment

Can a creditor garnish my wages without taking me to court?

Most private creditors, including credit card companies, hospitals, and personal loan lenders, must sue you, win a court judgment, and obtain a separate garnishment order before they can touch your wages. But certain government agencies skip that process entirely. The IRS can levy wages for unpaid taxes without filing a lawsuit. The Department of Education can garnish wages for defaulted federal student loans without a court order. Child support enforcement agencies can garnish without suing you. All of these must give you written notice before starting, and in most cases you have the right to request a hearing to challenge the garnishment or propose repayment. But they do not need a judgment first.

How much of my paycheck can be taken for a credit card or personal loan debt?

Federal law caps it at the lesser of 25 percent of your disposable earnings for that pay period, or the amount by which your disposable earnings exceed 30 times the federal minimum wage, which is $217.50 a week based on the current federal minimum of $7.25 per hour. If your disposable earnings are at or below $217.50 a week, none of your wages can be garnished for consumer debt. Disposable earnings means after taxes and legally required deductions, not after your bills. Some states set limits more protective than the federal rule. North Carolina, South Carolina, Pennsylvania, and Texas generally prohibit wage garnishment for consumer debts entirely.

Can my employer fire me because my wages are being garnished?

Federal law says no, but only for a single garnishment. If you have two separate wage garnishment orders from two separate creditors, that federal protection disappears and your employer may legally terminate you. Some states offer broader protection that covers multiple garnishments. Check the laws in your state if you are facing more than one garnishment order, and consider resolving at least one before multiple orders pile up.

What happens if I ignore a debt collection lawsuit?

The court enters a default judgment against you, automatically, without the creditor having to prove anything. You lose by not showing up. From that point, the creditor can move to garnish your wages, levy your bank account, or place liens on property. The deadline to respond to a lawsuit is typically 20 to 30 days from when you were served. Once a default judgment is entered, reversing it is significantly harder than responding to the lawsuit in the first place. Even a brief call to a legal aid organization before that deadline can change the outcome entirely.

Can they garnish my Social Security or disability payments?

Private creditors cannot garnish Social Security, disability benefits, or veterans’ payments as income. But once those payments land in your bank account, a bank levy can reach them if the funds are mixed with other money or if your balance has grown beyond two months of protected deposits. Receive benefits by direct deposit, keep them in a separate account, and do not let the balance accumulate much beyond your monthly needs. Those steps preserve the federal protection. Government debts, including unpaid taxes and defaulted federal student loans, can access Social Security payments under separate rules that private creditors cannot use.

How do I stop wage garnishment once it has already started?

Your main options are filing a claim of exemption with the court if your income qualifies for legal protection or the garnishment creates serious hardship, negotiating a settlement or structured payment plan directly with the creditor in exchange for releasing the order, challenging the underlying default judgment if it was entered improperly, or filing for bankruptcy, which triggers an automatic stay that stops all garnishment immediately. Each path has different timelines. Free legal aid can help you identify which one applies to your situation. Start at nlada.org.

What does judgment proof mean?

Being judgment proof means that even if a creditor sues you and wins, they cannot actually collect anything, because your income is legally protected and you have no assets worth taking. This typically applies to people with very low wages, people living on Social Security or disability, and people with little or no savings or property. It does not erase the debt or prevent a lawsuit, but it makes any judgment unenforceable for as long as your situation stays the same. A legal aid organization can confirm whether this applies to you and help you communicate your status to creditors in writing.

Can a creditor freeze or take money directly from my bank account?

Yes. A court judgment gives a creditor two tools: wage garnishment and a bank levy. A bank levy freezes your account and allows them to take funds directly, often without much warning. Federal law automatically protects two months of directly deposited federal benefits, but anything beyond that threshold may be exposed. The rules vary by state. If your account is frozen after a judgment, contact a legal aid organization or consumer law attorney immediately. Time matters because funds can be transferred out quickly once the freeze is lifted in the creditor’s favor.

What is a default judgment and can I fight one?

A default judgment is what happens when you are sued and do not respond by the deadline. The court rules for the creditor automatically. Once entered, they can pursue garnishment and account levies right away. You can challenge a default judgment if you were never properly served with the lawsuit, if the debt is not actually yours, or if you had a legitimate reason for not responding in time. The window to challenge varies by state, typically six months to two years. If you believe a default judgment was entered against you improperly, contact a consumer law attorney or legal aid organization as quickly as possible. The longer you wait, the fewer options remain.