When you opened your bank account, the bank did not ask you to name a beneficiary. That was not an oversight. They are not required to ask, so they do not. What is a beneficiary on a bank account? It is the person legally designated to receive your money when you die, bypassing probate entirely. The form that makes it happen has been sitting at your bank since the day you opened the account. They just never told you to fill it out. Understanding this is the difference between your family accessing your money within days of your death and watching it sit frozen in a probate process that can drag on for months, while rent is still due, while funeral costs arrive immediately, while the legal system takes its time.

What Is a Beneficiary on a Bank Account, Actually

A beneficiary is the person you legally designate to receive the money in your account when you die. That is the plain definition. The mechanics are what matter.

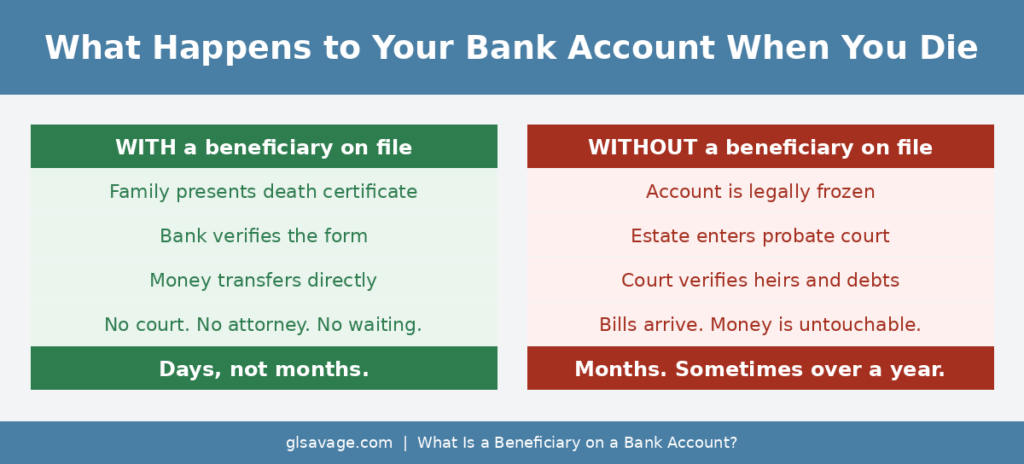

Most banks implement this through a payable on death designation, shortened to POD. You fill out a short form. You name a person. The bank keeps that form on file. When you die and the bank receives a certified death certificate, it transfers the money directly to that person.

No court. No attorney. No waiting period for probate. The bank verifies the paperwork and moves the money.

While you are alive, nothing changes. The beneficiary has zero access to the account. They cannot see the balance. They cannot withdraw anything. The designation is legally invisible until death activates it.

That is a well-designed system. The problem is not the system. It is that banks do not offer you the form when you open an account, and most people spend their entire lives without one.

Why Banks Do Not Bring Up the Beneficiary Form When You Open an Account

Banks are not required by law to ask you to name a beneficiary on a checking or savings account. It is optional. It is available. But it is not part of the standard account-opening process at most retail banks.

When you sit down to open an account, you sign forms covering account ownership, fee disclosures, and terms of service. The payable on death form is a separate document the bank keeps available on request. The teller does not pull it out by default. The new accounts representative does not hand it to you as part of the packet. Some banks have made it available through online banking. Many have not.

The result is that millions of people have bank accounts with no beneficiary designation because no one ever told them they could have one. Not a failure of character. Not a failure of planning. A failure of disclosure that the industry has no incentive to fix.

You have to know to ask. Now you know.

What Happens to a Bank Account With No Beneficiary

If there is no beneficiary designation, the bank cannot release the funds to anyone after you die. Not a spouse. Not a child. Not the person who has been managing the bills for years.

The account gets frozen. Not metaphorically. Legally. No one touches that money until a court says so.

From that point, the money becomes part of the legal estate and must move through probate. Probate is the court-supervised process for settling a dead person’s financial affairs: verifying legal heirs, confirming outstanding debts, and authorizing distributions. Depending on the state and the complexity of the estate, this can take months. In disputed or complicated cases, it can take over a year.

During that time, the money is untouchable. Rent is due. Utilities are due. Funeral costs arrive within days of death and do not wait for court schedules.

Here is a practical tell that estate attorneys know and most families do not. When you contact a bank after someone dies, pay attention to what they ask for. If they ask for a death certificate and nothing more, a beneficiary designation likely exists and the transfer process is straightforward. If they ask for Letters Testamentary, there is no beneficiary designation and the account is headed into probate. Letters Testamentary are court documents that give an executor legal authority to act on behalf of the estate. If the bank is asking for them, no shortcut exists.

Beneficiary Designations Override Wills. Almost Nobody Knows This.

A beneficiary designation on a bank account overrides whatever is written in a will.

If a will says the money goes to a daughter but the bank account lists a brother as beneficiary, the bank follows the account form. Not the will. The financial institution is not interpreting wishes. It is enforcing a contract.

Courts have ruled on this repeatedly. The contract wins almost every time.

This cuts in both directions. It is protective when the designation is current and intentional. It is catastrophic when it is outdated. Someone who spent money on an estate attorney, wrote a detailed will, and believed everything was handled can still have their assets go somewhere they never intended because they never updated a bank form.

The will and the bank account form are two separate legal documents. The bank only cares about one of them. It is not the will.

The Accidental Inheritance: When Old Paperwork Rewrites the Future

Beneficiary designations get set and forgotten. That is how they become disasters.

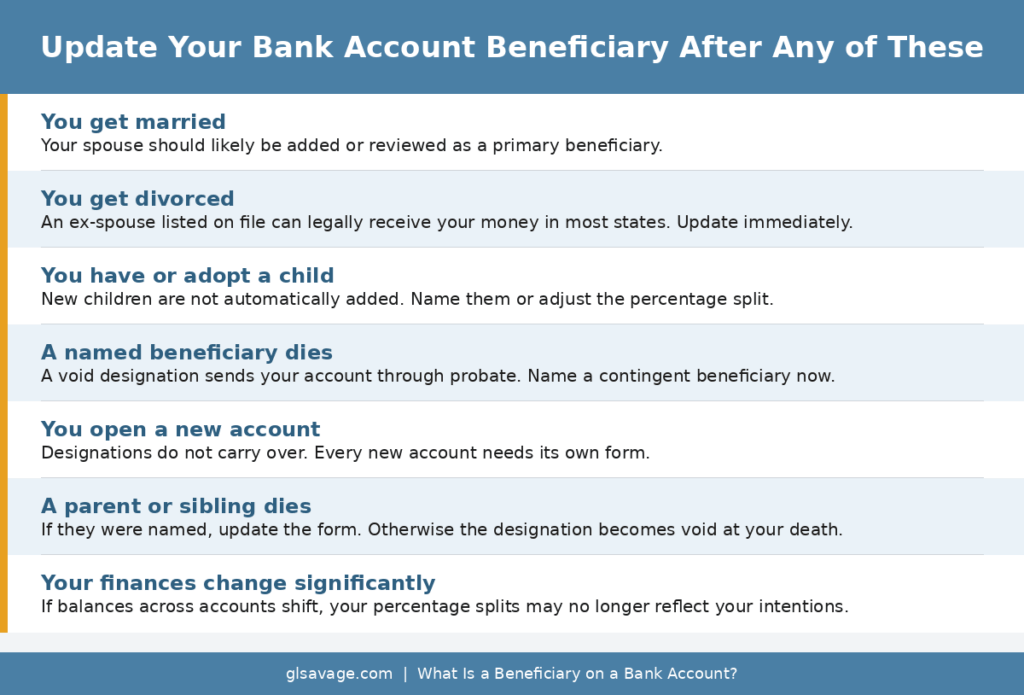

Someone opens an account at twenty-two and names their parent. They get married at thirty. They have children at thirty-four and thirty-seven. They die at fifty-one. If the parent is still living, the parent may receive the account balance. Not the spouse. Not the children. The parent.

This is not hypothetical. It is a recurring problem in estate law.

The divorce scenario is even sharper. An ex-spouse listed as beneficiary on accounts opened during a marriage can legally receive those funds after death in many states, even after a divorce decree. Some states automatically revoke an ex-spouse’s beneficiary status when a divorce is finalized. Others do not. The rules depend on the state and the account type. Federal law governs some retirement accounts differently than state law governs bank accounts.

Banks do not flag accounts where the named beneficiary is now an ex-partner. They do not send annual reminders to review designations. They do not cross-reference account forms with current family situations. They hold the form and wait. However long it takes.

The fix is a calendar reminder, not a lawyer. Any major life event, marriage, divorce, a child born, a parent who has died, is a reason to call your bank and ask who is currently listed. The form takes ten minutes to update and costs nothing.

What Is a Beneficiary vs. a Joint Account Owner

A joint account owner co-owns the account in real time. They can deposit and withdraw while the original owner is alive. They have equal legal access to every dollar in the account.

A beneficiary has no ownership and no access while the account holder is alive. The designation only activates at death.

People sometimes add a family member as a joint account holder to simplify things after death. It does transfer quickly when one owner dies. But while the original owner is still alive, that account is now legally the joint owner’s money too. If the joint owner gets sued, goes through a divorce, or carries significant debt, that account may be exposed to their creditors. The money is legally theirs.

A beneficiary designation accomplishes the same transfer-at-death goal without any of that exposure during life. The money stays entirely in the account holder’s control until the moment it is not needed anymore.

Joint ownership is a blunt instrument. A POD designation is a scalpel. Most people use the blunt instrument because no one told them the scalpel existed.

The Split Account Trap

If you have multiple accounts and name different people as beneficiaries on each one, each person receives whatever happens to be in that specific account when you die. The amounts are not equalized. They are not adjusted. They are locked to the balance at the time of death.

If you named one child on a savings account and another on a checking account, and one account holds significantly more than the other, those children receive unequal amounts. That may not be what you intended. The bank does not know what you intended. It only knows the form.

This is compounded when balances shift over time. You may have set up the designations when both accounts held similar amounts. Life moves, balances change, and the designations stay fixed to the old picture.

The solution is to name all intended beneficiaries on a single account with a percentage split, or to review designations regularly and adjust when account balances change significantly.

What Happens if the Beneficiary Dies First

If the person you named as beneficiary dies before you, and you never update the form, the designation becomes void at your death. The account then falls back into the estate and may go through probate, which is exactly what the designation was meant to prevent.

Most banks allow you to name a contingent beneficiary, sometimes called a secondary beneficiary. This person receives the funds only if the primary beneficiary is already dead. Without one, a single death in the family can collapse the entire plan.

When you set up a beneficiary designation, naming a contingent beneficiary at the same time takes two extra minutes and can prevent a significant delay later.

The Beneficiary Has to Claim the Money

The transfer does not happen automatically the moment someone dies. The beneficiary has to go to the bank, show valid identification, and present a certified copy of the death certificate. The bank then processes the claim and releases the funds.

If the beneficiary does not know they are named, nobody will tell them. The bank does not reach out. There is no notification system. If the account holder never told the beneficiary they were listed, the beneficiary may never know the account exists.

Accounts that go unclaimed long enough eventually get transferred to the state’s unclaimed property division. The money is not permanently lost, but it requires knowing to look, knowing where to look, and going through a claims process to get it back.

Tell your beneficiary they are named. Tell them which bank. Tell them they will need a certified death certificate and a valid ID. That conversation takes five minutes and prevents real chaos. The form you filled out is only half the job. The other half is making sure the right person knows it exists.

What POD Accounts Do Not Protect Against

A payable on death designation avoids probate. It does not make the account invisible to everyone.

Creditors of the estate can sometimes reach POD accounts. If the estate does not have enough assets in probate to cover outstanding debts, creditors in some states have grounds to make claims against non-probate assets, including POD accounts. This varies significantly by state law, and it is worth knowing your state’s rules if significant debt is part of the picture.

Naming a minor as beneficiary creates its own problem. Banks will not release funds directly to a child. If a minor is named and no trust or legal guardian arrangement is in place, the money gets held until a court appoints someone to manage it, which puts you right back into the legal process you were trying to avoid. If you want to leave money to a child, the practical options are a UTMA custodial account or a formal trust. A UTMA (Uniform Transfers to Minors Act) account lets an adult manage money for a child without going to court and is the simpler path for most people. The POD form alone does not solve the minor problem.

Inheritance taxes are also still possible. The beneficiary typically will not owe federal income tax on funds received, but some states charge an inheritance tax on money received after a death. Whether that applies depends on where the beneficiary lives and the size of the amount. Bypassing probate does not automatically bypass all tax exposure.

Community property states add another layer. Nine states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin) treat assets acquired during a marriage as jointly owned by both spouses. In these states, a spouse may have legal rights to account funds regardless of what the beneficiary designation says. If you live in one of these states and have named someone other than your spouse as beneficiary, that designation may be contested. The rules vary, and they interact with federal law in ways that differ by account type. Worth knowing before assuming the form settles everything.

A POD designation is a powerful tool. It is not a blanket shield against every obligation connected to an estate.

Beneficiary Designations Across Other Account Types

Bank accounts are the most overlooked place beneficiary designations exist, but they are not the only place. Retirement accounts like 401(k)s and IRAs have them. So do brokerage and investment accounts, certificates of deposit, and life insurance policies. The transfer-on-death designation, often labeled TOD rather than POD, works identically but is used for investment accounts instead of bank accounts.

All of them override the will. All of them bypass probate. And all of them are subject to the same problem: set once, left unchanged for years, and trusted to reflect a life that no longer looks the same.

Federal law governs 401(k) beneficiaries differently than state law governs bank accounts. In many cases, a divorce does not automatically revoke a 401(k) beneficiary designation the way it might for a bank account in certain states. An ex-spouse named on a 401(k) from a previous employer may still be the legal beneficiary decades later if the form was never updated.

Every account type requires its own review. Updating one does not update the others.

Why Knowing What Is a Beneficiary on a Bank Account Matters More When Money Is Tight

Estate planning is marketed as something wealthy families do. The financial services industry has done an excellent job of making people with modest assets feel like this category does not apply to them.

The truth is the opposite. Knowing what is a beneficiary on a bank account matters most when money is already tight. A household without significant savings cannot absorb a financial freeze. If the person who managed the accounts dies and those accounts get locked in probate, the surviving family may face an immediate crisis with nothing to buffer it. Funeral costs alone can run several thousand dollars, and that bill does not pause for a court schedule.

A named beneficiary means the money is accessible within days of presenting a death certificate. Not months. The family can cover immediate costs and keep basic expenses moving while everything else gets sorted.

This does not require an attorney. It does not require a trust. It requires asking your bank for a form they already have, that costs nothing to fill out, and that most people have never been told exists. If you are also working on building a financial cushion, Build an Emergency Fund Living Paycheck to Paycheck covers that side of the picture. And The Hidden Costs of Not Having a Bank Account covers what it costs when the financial system treats you as an afterthought.

How to Add or Update a Beneficiary on a Bank Account

Contact your bank and ask whether your accounts have a payable on death designation on file. Some banks confirm this through online banking. Others require you to call or come in.

If no designation exists, ask for the POD form. You will typically need the beneficiary’s legal name, date of birth, and Social Security number. Fill it out, sign it, and submit it. Ask for written confirmation that the designation has been recorded. They will not always offer it. Ask.

If a designation already exists and needs updating, complete a new form. The new designation replaces the old one. The bank does not notify the person being removed.

Do each account separately. A designation on one account does not carry over to other accounts at the same bank.

Then tell your beneficiary. Their name, which bank, which accounts, and what they will need to bring. The form you filed is only useful if they know it exists.

The Full Picture

The financial system is not designed around your intentions. It is designed around your paperwork. A will says what you meant. A beneficiary designation is what actually happens.

Banks offer this form. They do not push it. They do not follow up. They do not remind you when your life changes. They keep the form on file until someone needs it, and if you never filled one out, they freeze the account and wait for a court to sort it out.

That is not a conspiracy. It is just how the system runs. It runs that way because most people never push back. They pay the bill, sign the forms they are handed, and assume someone would have mentioned it if something important was missing. What is a beneficiary on a bank account? It is the form that was missing. Now you know what to do about it.

Frequently Asked Questions About Bank Account Beneficiaries

What is a beneficiary on a bank account?

A beneficiary on a bank account is the person legally designated to receive the funds when the account holder dies. Most banks implement this through a payable on death designation. When a certified death certificate is presented to the bank, the funds transfer directly to the named person without going through probate.

Why don’t banks automatically set up beneficiaries when you open an account?

Banks are not legally required to ask customers to name a beneficiary on a checking or savings account. The payable on death form exists and is available, but it is typically a separate document the customer has to request. Most people never know to ask, so they never get one.

Does a bank account beneficiary override a will?

Yes. A beneficiary designation on a bank account overrides the instructions in a will in almost all cases. The bank follows the account form, not the will. This is one of the most consequential and least-discussed facts in personal finance.

What happens to a bank account with no beneficiary when someone dies?

The bank freezes the account. The money becomes part of the estate and goes through probate, a court process that can take months before the funds are accessible. Bills do not pause during that time.

How can you tell if a bank account has a beneficiary designation?

When contacting a bank after someone dies, pay attention to what documents they request. If they ask for a death certificate only, a beneficiary designation likely exists. If they ask for Letters Testamentary, a court-issued document giving an executor legal authority, there is no designation and the account must go through probate.

Can an ex-spouse still collect on a bank account after divorce?

In many states, yes. Some states automatically revoke an ex-spouse’s beneficiary designation when a divorce is finalized, but many do not. The bank follows the form on file regardless of marital history. Updating beneficiary designations after a divorce is not optional. It is urgent.

Does a payable on death bank account avoid probate?

Yes. A POD account with a valid beneficiary designation bypasses probate entirely. The bank transfers funds to the named beneficiary once the death certificate is presented, without any court involvement required.

What is the difference between a bank account beneficiary and a joint account holder?

A beneficiary has no ownership or access while the account holder is alive. A joint account holder co-owns the account in real time and can make withdrawals during the original owner’s lifetime. A joint account also exposes the funds to the joint owner’s creditors and legal situations in ways a beneficiary designation does not.

Does the money transfer automatically to the beneficiary after death?

No. The transfer is not automatic. The beneficiary must go to the bank, present valid ID and a certified death certificate, and initiate the claim. If the beneficiary does not know they are named, the money may sit unclaimed. Unclaimed accounts are eventually turned over to the state’s unclaimed property division.

Can creditors take money from a payable on death bank account?

Possibly, depending on state law. A POD designation bypasses probate but does not automatically eliminate all debt obligations. If the estate has significant outstanding debts and insufficient probate assets to cover them, creditors may have grounds to claim against POD accounts in some states.

Can you name a minor as a bank account beneficiary?

You can name a minor, but the bank will not release funds directly to a child. Without a trust or court-appointed guardian arrangement in place, the money gets held until a court appoints someone to manage it. If you want to leave money to a child, a UTMA custodial account (which lets an adult manage funds for a minor without going to court) or a formal trust are the more reliable paths. The POD form alone does not get money to a child cleanly.

Can you name more than one beneficiary on a bank account?

Yes. Most banks allow multiple beneficiaries with a percentage split. You can also name a contingent, or secondary, beneficiary who receives the funds only if the primary beneficiary has already died. Without a contingent beneficiary, an outdated or void primary designation can send the account back into probate anyway.

Do you have to pay taxes on money received as a bank account beneficiary?

You typically will not owe federal income tax on funds received as a POD beneficiary. However, some states charge an inheritance tax, and the rules vary by state and amount received. Bypassing probate does not automatically mean bypassing all tax exposure.