Two paychecks coming in. Both people working full time. And somehow, at the end of the month, there is nothing left. No savings. No cushion. No explanation for where it all went. If that describes your household, you are not mismanaging your money. You are experiencing something the financial advice industry almost never explains honestly: the second income is not worth what it looks like on paper. By the time taxes, childcare, commuting, and the costs that come with two working adults run through it, that second paycheck often nets far less than either earner expects. Sometimes it barely nets anything at all. This article runs the actual math on why two-income households are still broke, and names the systems that make it this way.

This Was Not a Choice. It Was a Survival Response.

The two-income household is treated as a lifestyle upgrade, a sign of ambition, a modern arrangement that families choose because they want more. That framing is wrong, and it matters because it changes how you understand the financial pressure you are under.

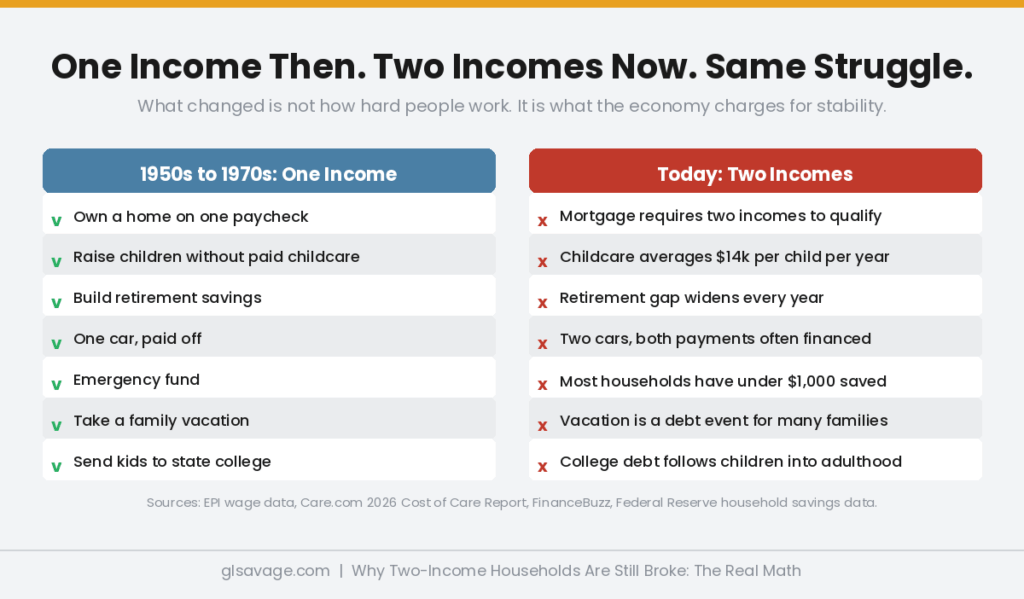

For three decades after World War II, wages grew rapidly and broadly. A single income could support a family, build equity, and fund a modest retirement. Then, starting in the late 1970s, that stopped. Real wage growth for middle and lower earners flatlined. Pew Research Center analysis of federal wage data found that real wages for most U.S. workers have barely budged in decades. The inflation-adjusted hourly wage for the typical worker had roughly the same purchasing power in recent years as it did in the late 1970s. Costs kept rising. Wages did not keep up for most households. The single income that once held a household together stopped being enough.

Women did not flood the workforce in the 1970s and 1980s primarily because liberation was winning. They entered because the math of a single income started failing. Families needed a second paycheck to maintain what had previously been achievable on one. The dual-income household became the norm not as an upgrade but as the new minimum requirement. And then the economy built itself around the assumption that both adults were working, which drove up housing prices, childcare costs, and the overall cost of middle-class life to a level that assumed two incomes even as those two incomes increasingly failed to deliver what one used to.

That is the structure this article is about. Not a budgeting problem. A structural trap that was decades in the making.

The Second Income Is Taxed at the Highest Rate You Pay

This is the mechanism most two-income households never fully understand, and it is one of the core reasons why two-income households are still broke even when both paychecks look healthy on paper.

The U.S. tax system is progressive, meaning income is taxed in layers. The first dollars you earn are taxed at 10%. The next chunk at 12%. Then 22%, and so on up. When a household already has one income, that income has already climbed through the lower brackets. The second income does not start at the bottom. It starts wherever the first income left off.

Here is what that looks like in practice using 2026 IRS brackets. The married filing jointly standard deduction is $32,200, which is the amount the IRS lets you subtract from your income before taxes are calculated. One partner earns $90,000. After the standard deduction, $57,800 is taxable, sitting in the 12% bracket. The second partner earns $80,000. Combined gross income is $170,000. After the standard deduction, $137,800 is taxable, which puts the top portion firmly in the 22% bracket. Almost the entire second income is taxed at 22% or higher, while most of the first income was taxed at 12%. Two people earning the same amount at the same job. Different effective rates because one income arrived second. This is the central math behind why dual income households find themselves no better off than they expected.

This is not the marriage penalty, which is a separate and narrower concept that affects couples with very similar high incomes at the top brackets. This is the second earner penalty, and it applies to virtually every dual-income household regardless of income level. The second income always starts where the first left off. The lower brackets are already claimed. Every dollar of the second income is taxed harder than most of the first, on earnings that look identical on paper.

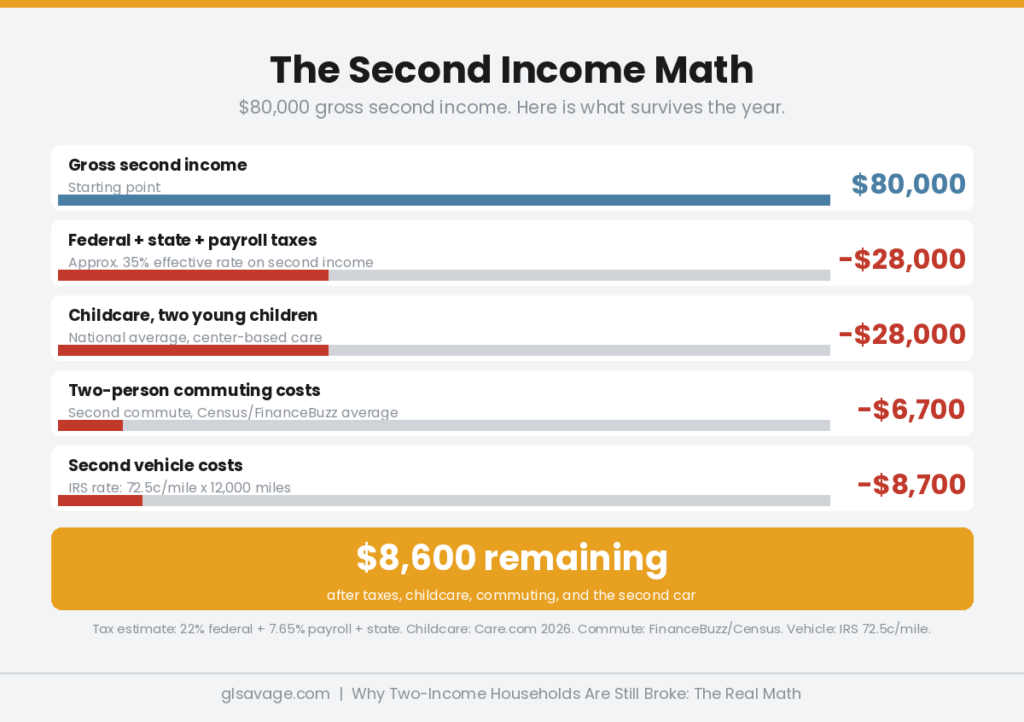

Add state income taxes on top of federal. In most states, the second income gets stacked the same way. For a second earner bringing in $80,000 in a state with income tax, the combined bite of federal income tax at 22%, payroll taxes at 7.65%, and a modest state income tax can push the effective rate on the second income to 35% or more. On $80,000 gross, that is potentially $28,000 gone before that person sees a dollar of their paycheck. The actual number depends on your state and your deductions. The direction is the same everywhere.

Childcare Can Eat the Entire Second Income

The federal government’s own definition of affordable childcare is 7% of household income. The Care.com 2026 Cost of Care Report, based on 3,000 parents, found the average family spends 20% of household income on childcare. Nearly triple the government’s benchmark. One in five families spends more than $30,000 per year.

The national average cost of center-based infant care is $13,935 per year, according to the National Database of Childcare Prices. In 28 states, that figure exceeds the cost of a year of college tuition. In Washington D.C., it runs $24,243. In Massachusetts, $20,913. In most states, childcare for a single infant is the largest line item in a family budget after housing. In some cities it exceeds housing.

Run the math for a family with two young children where the second earner makes $45,000. Two kids in center-based care: roughly $28,000 a year at the national average. After taxes, a second earner making $45,000 takes home somewhere around $31,500. Childcare alone consumes $28,000 of that. What remains, roughly $3,500 for the year, has to cover the second commute, the work wardrobe, the convenience spending, and the emergency fund that never gets funded. In many cases the math does not work at all. The second income is net negative once childcare is fully accounted for. At $80,000, the math is better but not by as much as people expect . At $80,000 gross with no other deductions, take-home is roughly $56,000 after taxes, minus $28,000 childcare, leaves $28,000 to cover every other cost of having a second person employed. That is $2,300 a month. Then the commute, the second car, and the convenience costs come out of it.

This is not a failure of budgeting. The childcare system is a central structural reason why two-income households are still broke at income levels that should provide stability. It was never built to be affordable on a middle-class income. It was built on the assumption that most families would not need it. Then wages stopped growing, both adults had to work, and suddenly everyone needed it at once. The price reflects that demand hitting a system never designed to absorb it.

Two Commutes Cost More Than Most Households Calculate

One worker commuting costs an average of $6,700 per year, according to FinanceBuzz analysis of Census Bureau data. That covers gas, vehicle maintenance, parking, tolls, and transit costs. Two workers commuting costs roughly $13,400 combined. In major metro areas the number is considerably higher. New York area commuters lose an estimated $11,000 per year each. San Francisco workers face average commuting costs over $12,000.

Most households treat commuting as a fixed cost, unavoidable and therefore not worth calculating against the second income. But it is not fixed. It is a direct function of how many people in the household are working outside the home. When the second income disappears, so does the second commute. That $6,700 should be subtracted from the second income’s gross on any honest comparison. It almost never is.

Commuting costs are also not tax-deductible for employees. The IRS does not allow workers to deduct getting to and from work. Commuter benefits, which allow pre-tax dollars to cover transit or parking up to $340 per month in 2026, help reduce the hit, but most workers either do not have access to them or do not use them fully. The second commute is an after-tax expense, paid out of after-tax income, on top of everything else already eating the second paycheck.

The Costs Nobody Counts

Beyond taxes, childcare, and commuting, there is a layer of costs that come with two people working full time that most financial analyses skip entirely. These are real expenses that exist because of employment, not in spite of it.

Work clothing and grooming. Two people maintaining professional appearances is a recurring line item. Dry cleaning, work clothing, haircuts timed to professional standards. Not dramatic individually. Ongoing and unavoidable as long as both people are employed.

Convenience spending. When both adults are working full time and running a household, there is less time for everything. Less time to cook means more takeout and delivery. Less time to shop carefully means less saved on groceries. Less time to maintain things means paying others to do it. The time cost of dual employment converts directly into cash expenditure, and that expenditure comes out of the income employment generates.

A second car. In most of the country, two working adults means two vehicles. Two payments if both are financed. Two insurance policies. Double the maintenance, registration, and depreciation. The IRS estimates vehicle operating costs at 72.5 cents per mile in 2026. Two cars each driven 12,000 miles a year: $17,400 in total vehicle costs. None of it shows on a pay stub. All of it comes out of what both incomes generate.

Elder care. The Care.com 2026 report found the average parent is managing childcare, elder care, pet care, and housekeeping simultaneously, with total caregiving costs consuming 37% of household income when all categories are combined. The sandwich generation, people simultaneously raising children and supporting aging parents, is not a niche demographic. It is a growing share of dual-income households, and the financial weight rarely gets named in conversations about why two incomes do not stretch as far as they should.

Lifestyle Inflation Absorbs What Is Left

After taxes, childcare, commuting, and the invisible costs of dual employment, what remains of the second income is often a smaller number than either earner expects. What happens to it next is the final mechanism explaining why so many two-income households end up feeling as financially stretched as single-income households did a generation ago.

Two incomes create the perception of financial breathing room, even when the actual breathing room after costs is modest. That perception changes spending behavior. The house purchase reflects two incomes, so the mortgage is larger. The car payments reflect two incomes. Dining, travel, and discretionary spending patterns expand to match two incomes. The problem is that all of these commitments lock in at the combined gross income level, before any of the costs above come out.

When the second income is consumed before it arrives through taxes and childcare, and the remaining sliver is absorbed by the second commute and convenience spending, the household discovers it has the obligations of a two-income lifestyle and the actual financial margin of something considerably smaller. This is the structural trap at the center of why two-income households are still broke. It is built by the gap between what two incomes look like on paper and what they actually deliver.

The Breakeven Question Nobody Asks at the Right Time

The question most households never answer with math is this: what does the second income actually net after every cost that exists because of it?

Not the gross. Not the take-home after basic withholding. The real number after childcare, the second commute, the tax stacking, work clothing, and the convenience costs generated by having no time. For many middle-income families with young children, that number is dramatically smaller than either earner believes. For some it is effectively zero or negative during the years when childcare costs peak.

This is not an argument for one person to stop working. Career continuity matters. Future earning potential matters. The financial catastrophe of depending on a single income and having that income disappear is a real risk worth insuring against. But those are different arguments from the cash flow argument, and households get into trouble when they treat them as the same thing. They make commitments based on gross combined income, discover the net is far lower, and then spend years trying to figure out what went wrong. Nothing went wrong. The math was always there. Nobody ran it.

The calculation should be made with real numbers before commitments lock in, not reconstructed afterward when the question is why there is nothing left at the end of the month. The system that produced this outcome is not going to explain itself. Why a Second Job Often Costs More Than It Pays runs the same logic for households considering adding income rather than evaluating an existing arrangement. The math applies in both directions.

What Actually Changes the Outcome

None of this means dual-income households are stuck. It means the standard financial advice, earn more, spend less, save the difference, assumes a baseline that does not exist for most two-income families. What changes the outcome is running the real numbers and making decisions based on those, not on gross income figures.

Dependent Care Flexible Spending Accounts, also called DCAPs, let households set aside up to $5,000 per year in pre-tax dollars for childcare. That is not a lot against actual childcare costs, but it is real money. Employers are required to offer it when they offer health FSAs. Most eligible households do not use it. It sits unclaimed while those same households pay full childcare costs with after-tax dollars.

The Child and Dependent Care Tax Credit allows a percentage of childcare expenses to be credited directly against taxes owed. For 2025, the credit covers 20% to 35% of up to $3,000 in expenses for one child, or $6,000 for two or more, depending on income. It is not a deduction. It reduces the tax bill dollar for dollar. Most households eligible for it claim it. Most also do not know that the DCAP and the tax credit interact, and using both incorrectly reduces the benefit of each. A tax professional who works with families is worth the conversation specifically during the childcare years.

The other thing that changes the outcome is facing the fixed costs that expanded to match two incomes. The mortgage. The car payments. The housing commitments. These are harder to change than discretionary spending, but they are the actual drivers of the gap. Cutting coffee will not solve a problem caused by a mortgage sized for two incomes and a childcare bill that consumes one of them. Build an Emergency Fund Living Paycheck to Paycheck covers what to do when the margin is genuinely thin regardless of income level.

The larger point is that why two-income households are still broke is not a behavioral question. It is a structural one. The tax code was not designed for two working adults with equal incomes. The childcare system was not priced to be affordable on middle-class wages. Wages stopped growing in the late 1970s and two incomes became the new floor, not an upgrade. The cost of everything built itself around that assumption. And the financial advice industry keeps telling households to budget their way out of a problem that budgeting did not cause. Run the math. Name the systems. That is where this starts.

Frequently Asked Questions

Why do two-income families still struggle financially?

Because the second income is taxed at the highest marginal rate the household pays, childcare can consume most or all of what is left after taxes, two commutes and two cars come out of the same pool, and the convenience costs of having no time convert directly into spending. The gross income of two earners looks like stability. The net after every cost that exists because of employment is often dramatically smaller than either earner expects.

Does a second income save money after childcare costs?

For many families with young children, barely or not at all. The national average for center-based infant care is $13,935 per year. Two young children runs close to $28,000. A second earner making $45,000 takes home roughly $31,500 after taxes, leaving about $3,500 after childcare before a single other cost of employment is counted. At $80,000, the picture is better but still tight: roughly $56,000 take-home, minus $28,000 childcare, leaves $28,000 to cover a second commute, a second car, and everything else. The only way to know your actual number is to run it with your real income, your state’s tax rate, and your actual childcare costs.

What is the second earner tax penalty and how does it work?

The second earner penalty is not a formal IRS rule. It is the structural result of how progressive taxation works. When the first income has already moved through the lower brackets, the second income starts where the first left off. In a household where the first partner’s income reaches into the 12% or 22% bracket, the second income is taxed at that higher rate from the first dollar, even if the same amount earned by a single person would be taxed at 10% or 12% at the bottom. The second earner always faces a higher marginal rate than the same income would face if it were the household’s only income. The formal marriage penalty is a related but separate concept that affects couples with very similar very high incomes at the top brackets. The second earner penalty affects virtually everyone.

How much does commuting cost a two-income household per year?

Roughly $13,400 combined, based on FinanceBuzz analysis of Census Bureau data putting the individual average at $6,700. In major metro areas considerably more. New York area commuters average around $11,000 per person per year. This is an after-tax expense that directly reduces what the second income actually delivers, and it is almost never factored into whether dual employment makes financial sense.

What tax benefits exist for two-income families with children?

The Dependent Care FSA allows up to $5,000 in pre-tax dollars annually for childcare, which reduces taxable income and effectively lowers the cost. The Child and Dependent Care Tax Credit covers 20% to 35% of up to $3,000 in eligible expenses for one child or $6,000 for two or more. Both exist and both are underused. They also interact with each other in ways that reduce the combined benefit if you do not use them correctly. A tax professional can structure both to maximize what you get.

Is it worth it financially for both parents to work?

That depends entirely on your specific numbers. The financial case is stronger when childcare costs are lower relative to the second income, when both incomes are high enough that the tax stacking is less punishing proportionally, and when the long-term career and retirement benefits of staying employed are weighed alongside short-term cash flow. The financial case is weaker during the infant and toddler years when childcare peaks, in high-cost metro areas, and for second earners at lower income levels where the math may genuinely not work in the short term. The question deserves real numbers, not a general answer.

Why isn’t a higher household income solving the problem?

Because the costs that constrain two-income households scale with income rather than staying fixed. A higher combined income typically means a larger mortgage, more expensive childcare, higher tax brackets, more lifestyle spending locked in to match what two incomes are supposed to provide, and more expensive vehicles. The costs grow alongside the income. This is why households at $120,000, $150,000, and $200,000 combined often feel as financially squeezed as households at much lower levels. The problem is not the income. It is the proportion of that income consumed by fixed costs that expanded to match it.

When did two-income households become necessary rather than optional?

Starting in the late 1970s. For three decades after World War II, wages grew steadily and a single income could support a middle-class household. When wage growth stalled around 1979, costs kept climbing and the single-income household started failing financially. Women entered the workforce in large numbers through the 1970s and 1980s not primarily as a lifestyle choice but as a financial response to a paycheck that no longer stretched far enough. The economy then built itself around the assumption that both adults were working, which drove up the cost of housing, childcare, and everything else to a level that assumes two incomes. The two-income household is not a modern upgrade. It is what surviving the modern economy requires.