Your credit score was not built for you. That is the thing most explanations of this system leave out. The number exists because lenders needed a faster way to sort millions of borrowers, price loans differently for different people, and do it all without having to look any of them in the eye. The three private companies maintaining your financial file right now are not government agencies. They are businesses. The banks pulling your score are their customers. You are the product being evaluated. Understanding why your credit score exists does not change the system. But it changes how you see it, and that matters when the system is making decisions about your life.

It Started as a Math Problem for Lenders, Not a Tool for Borrowers

Before modern credit scoring, lending was personal. A banker looked at you, your job, your reputation in town. Lending decisions depended on judgment and familiarity. This system was slow, inconsistent, and deeply biased. Who you knew mattered as much as whether you could actually pay. Race, religion, and neighborhood shaped outcomes that had nothing to do with creditworthiness.

By the 1950s lenders wanted something faster. They wanted a way to evaluate millions of borrowers without personal knowledge. In 1956 Bill Fair and Earl Isaac built a company that tried to convert lending decisions into math. That company became FICO.

The concept was simple: look at how people repaid debt in the past, use that data to predict how they will repay in the future, assign a number, move on. This is the foundation of why your credit score exists. It is not a measure of your character. It is not a reward for being responsible. It is a probability model that lets lenders process applications at scale without thinking about you as a person.

What the industry rarely acknowledges is that replacing personal bias with a formula did not eliminate bias. It encoded it. Black and Hispanic borrowers score lower on average not primarily because of payment behavior differences, but because generational wealth gaps affect credit history length, available credit limits, and the types of accounts that build strong files. The system stopped asking who you knew and started asking how long you had been inside the system. For people who were historically locked out of that system, that distinction matters less than it sounds.

Your Score Is How Lenders Decide What to Charge You

Getting approved is only part of what your score does. The more consequential part is pricing.

Lenders use your score to decide what interest rate to charge you. A higher score gets a lower rate. A lower score gets a higher rate. This is called risk-based pricing. It means the lender charges you more if they think you are more likely to miss a payment.

Over the life of a mortgage, the difference between a strong score and a mediocre one can be tens of thousands of dollars. Over a car loan, it can be several thousand. That gap is not random. It is calculated. Your score is not there to help you get a better deal. It is there to help lenders decide how much to charge you for one. Knowing exactly how credit scores work is the only way to use the system instead of being used by it.

Three Private Companies Own Your Financial History

Most people assume their credit information lives in some kind of government database. It does not.

The credit reporting system is run by three private corporations: Equifax, Experian, and TransUnion. These companies collect your financial behavior data and sell access to it. Every time a bank pulls your credit report, the bureau gets paid. Your borrowing history is the product. The lenders are the customers. You are not.

That is not a conspiracy. That is the business model, stated plainly. And it explains another layer of why your credit score exists: predictive borrower data is extremely valuable, and there is an entire industry built on packaging and selling it. The same structure that drives how banks make money from overdraft fees operates here. Private companies, limited oversight, and profit motive pointing in a direction that is not yours.

You Can Avoid Debt and Still End Up With a Credit Problem

Many people believe they can sidestep the credit system by simply avoiding debt. In practice the system tends to find them anyway.

Collection agencies, medical providers, and some landlords can report information to credit bureaus. A medical bill that went to collections can appear on your credit report even if you never took out a loan in your life. Utility companies, phone carriers, and buy-now-pay-later services have expanded into credit reporting. A missed payment on a phone plan can affect the same number that determines your mortgage rate.

The system expands wherever financial behavior data becomes useful to someone who wants to evaluate you. Avoiding debt does not mean avoiding the system. This is part of what the poverty premium looks like inside the credit system: the less access you have had to mainstream financial institutions, the harder it is to build the file that the system rewards.

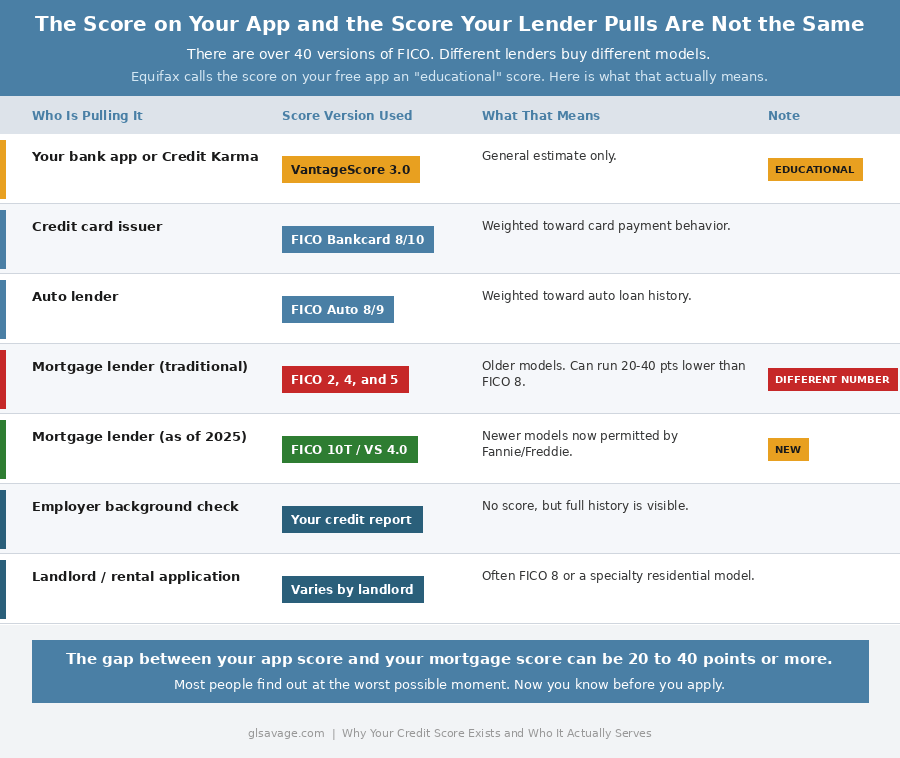

The Score on Your Free App Is Probably Not the Score That Matters

Most people think they have one credit score. They do not.

FICO alone has dozens of versions. Some are designed specifically for mortgage lenders. Some for auto lenders. Some for credit card issuers. VantageScore has its own versions. Different lenders buy different models depending on what they are lending for. The score your free monitoring app shows you is likely a VantageScore 3.0. That is not the score most lenders use.

Mortgage lenders have historically used older FICO models called FICO 2, FICO 4, and FICO 5. Credit card issuers often use FICO 8 or FICO 10. Auto lenders use versions weighted specifically toward auto loan repayment history. The score you check on your phone on Tuesday may look meaningfully different from the score a mortgage company sees on Wednesday. Not because anything changed. Because they are literally different products built on different formulas.

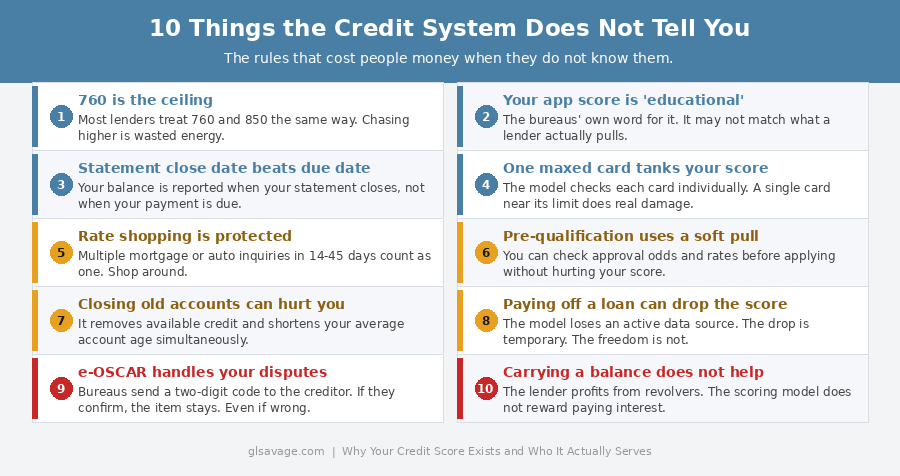

Equifax itself describes the scores consumers typically see as “educational” scores, meaning they are intended to give you a general sense of where you stand, not to replicate the exact number a lender will see. That word, educational, is doing a lot of work. It is a polite way of saying the number may not be the one that counts when it matters most. People make major financial decisions based on a number that is not the number being used to evaluate them. That is a design feature of this system, not an oversight.

Congress has pushed back on this. In 2023, the FHFA began requiring Fannie Mae and Freddie Mac to accept FICO 10T and VantageScore 4.0 for conforming mortgages alongside the older models. Both newer models better account for thin files and medical debt. The transition is ongoing as of 2025. If you are preparing for a mortgage, ask your lender specifically which score versions they are pulling.

How to See What Your Lender Actually Sees

The most direct option is myFICO.com, FICO’s own consumer site. A free account gives you a FICO Score 8 from Equifax. Paid plans, around $20 to $30 a month, include scores from all three bureaus plus the mortgage-specific and auto-specific versions lenders actually use. If you are preparing for a major loan application, this is the closest picture available before the lender pulls your file.

For free options that give you an actual FICO score rather than a VantageScore: Experian’s own site offers a free FICO Score 8. American Express MyCredit Guide offers a free FICO Score 8 from Experian and you do not need to be an Amex customer. Many banks and credit unions now offer free FICO scores to account holders. Check your existing accounts before signing up for anything new. Even a free FICO Score 8 is not identical to what a mortgage lender pulls, since mortgage lenders use older models. The number will be closer than a VantageScore, but the mortgage-specific scores at myFICO are the only way to see exactly what those lenders see.

For the underlying data your scores are built on, AnnualCreditReport.com is the only federally authorized source for free reports from all three bureaus. It does not give you a score, but it shows you exactly what the bureaus have on file, which is where errors live. One in five credit reports contains an error. Pulling your reports is not optional maintenance. It is how you find out if the system has something wrong on you before someone else uses it to make a decision about your life.

When You Pay Matters as Much as Whether You Pay

Most card companies report your balance to the bureaus once a month, when your statement closes. Whatever balance is on the account at that exact moment is what the scoring model sees. It does not know what you paid last week. It does not know what you will pay next week. It only sees that snapshot.

Two people can carry the exact same debt and get different scores based purely on timing. Someone who pays before the statement closes reports a low balance. Someone who pays after reports a high one. Same debt. Different picture. Different score.

Pay down your balance before your statement closes, not just before your due date. Those are two different dates and most people do not know that. The due date is when the payment is required. The statement close date is when your balance gets reported. Only one of them affects your score. This is covered in more depth in the credit scores explained article.

One Maxed-Out Card Can Hurt You Even When Your Overall Debt Looks Fine

The model looks at each card individually, not just the overall picture. Three credit cards. Two empty. One nearly maxed out. That single card can drag your score down even if your total utilization across all three looks reasonable. The model treats high utilization on individual accounts as a risk signal regardless of what is happening on the others. Spreading a balance across multiple cards instead of concentrating it on one makes a real difference to the model, even with the same total amount owed.

Shopping Multiple Lenders Will Not Wreck Your Score

A lot of people apply to one mortgage lender or one auto lender and stop there because they are afraid multiple applications will damage their score. That fear is costing them money.

Applying for credit triggers a hard inquiry that temporarily lowers your score by a few points. But scoring models recognize rate shopping. Multiple mortgage or auto loan inquiries within a short window, typically 14 to 45 days depending on the model, are counted as a single inquiry. You can apply to five mortgage lenders in two weeks and the score impact is the same as applying to one.

The lending industry does not advertise this. The difference between the first rate you are offered and the best rate you qualify for on a 30-year mortgage can be tens of thousands of dollars. Shopping around is not reckless. It is the only financially rational move.

You Can Check Your Approval Odds Without Hurting Your Score

There are two types of credit checks. A hard inquiry happens when you formally apply for credit and temporarily lowers your score. A soft inquiry happens when a lender pre-screens you or when you check your own credit. Soft inquiries do not affect your score at all.

Many card companies and lenders offer pre-qualification tools that use a soft inquiry. You can find out whether you are likely to be approved and what rate you might receive before you formally apply and trigger the hard pull. Most people do not know this exists. They apply blind, take the hit, and sometimes get declined anyway. Pre-qualification is not a guarantee, but it gives you real information before you commit.

Closing Old Accounts Can Hurt You Even if You Never Use Them

Closing an old card feels like cleaning up. Fewer accounts, simpler finances. In practice it can push your score down, sometimes significantly, for two reasons at once.

Your average account age drops because that older account is no longer in the mix. And your total available credit shrinks, which raises your utilization ratio even if your actual spending does not change. A card you opened ten years ago and never use is doing two things right now: adding age to your credit history and adding available credit that keeps your utilization low. Closing it removes both. The model does not know you did it to simplify your life. It just sees the numbers change.

Paying Off a Loan Can Temporarily Lower Your Score

Someone makes their last car payment and expects their score to go up. Sometimes it drops instead. This confuses people, and it makes sense that it does.

When you pay off an installment loan, the account closes. The model now has one fewer active account generating current repayment data. You are in a stronger financial position. But the model is reading a smaller dataset, and that can temporarily shift the number down. The score usually recovers. The model is not punishing you for being responsible. It is reacting to a change in what it can see. The score is not a grade on your behavior. It is a read on whatever signals happen to be available right now.

The Lender’s Ideal Customer Is Someone Who Always Carries a Balance

Inside the credit card industry there are two types of customers. Transactors pay their balance in full every month. Revolvers carry a balance and pay interest month after month.

Revolvers are far more profitable. They generate interest income every month. They generate late fees. They stay active in a way that keeps money flowing to the lender. The system does not reward carrying debt inside the scoring model, but the lending ecosystem is built around customers who do. The minimum payment structure, the interest rates, the way cards are marketed and designed, all of it is optimized for the customer who stays in the cycle. Understanding how minimum payments keep you in debt is the other side of understanding why your credit score exists.

760 Is Effectively the Ceiling. Most People Do Not Know That.

The maximum FICO score is 850. Most people treat that as the target. It is not.

Lenders generally treat scores of 760 and above the same way. Once you cross that threshold you are typically getting the best available rate that lender offers. Going from 760 to 820 to 850 does not get you a better deal. You have already crossed the finish line at 760. If your score is above that number, chasing a higher one is not a productive use of your energy. The lender does not care about the difference and neither should you.

Disputing Errors Is Harder Than It Should Be

Credit report errors are common. The FTC found that a significant percentage of reports contain errors serious enough to affect loan approvals or interest rates. Fixing them is harder than it should be, and understanding why requires knowing how the dispute process actually works.

Most disputes run through a system called e-OSCAR, operated by the bureaus themselves. When you file a dispute, the bureau does not investigate the account. It sends a coded message to the bank or lender that originally reported the data. The lender checks their records and responds electronically. If the lender confirms the information is correct, the bureau typically leaves it unchanged. Even if it is wrong.

The bureau is a middleman passing messages, not a judge reviewing evidence. If your dispute is rejected, you can add a statement to your file, escalate to the CFPB at consumerfinance.gov/complaint, or consult a consumer law attorney. Some errors are worth fighting harder than others, particularly when they are affecting your ability to get housing, employment, or a loan. Understanding how collection accounts affect your credit report is important context here, especially if the error involves a debt you do not recognize.

Collection Accounts Do Not Always Have to Stay on Your Report

If a debt has gone to a collection agency and that account is sitting on your credit report, you may have more options than you think.

Some debt collectors will agree to remove the collection entry from your report entirely in exchange for payment. This is called pay-for-delete. It is not a guaranteed right. Not all collectors will agree to it. But it is worth asking, and the ask has to happen before you pay anything. Once you pay without negotiating, the leverage is gone. The standard outcome is the account stays on your report marked paid, which is better than unpaid but still sitting there for years.

If a collector agrees to pay-for-delete, get it in writing specifically stating they will request deletion from all three bureaus before money changes hands. A verbal agreement in debt collection is worth nothing. Some collectors accept payment and leave the entry on the report anyway. Written agreement first. Payment after. That is the sequence that protects you. If you have collections showing, read the full breakdown of how collection accounts affect your credit report before you do anything else.

Your Score Can Drop Even When You Do Everything Right

A new inquiry. A lender quietly lowering your credit limit without telling you. A balance that reported slightly higher one month. The natural aging of your account mix. All of these can move your score without you doing anything wrong.

Score fluctuations are not always punishment for bad behavior. They are often the normal movement of a probability model constantly recalculating based on whatever data it can currently see. When you understand why your credit score exists as a prediction tool rather than a report card, the fluctuations become less alarming. The number was never a judgment of who you are. It was always just a snapshot of the signals available on a given day.

Once You Understand the System You Can Start Using It

Your credit score exists to serve lenders. It was built by lenders, maintained by private companies that sell your data to lenders, and designed to make the lending market more efficient for lenders. That is why your credit score exists. That is the system. You did not design it. But you have to live inside it.

Pay before your statement closes, not just before your due date. Keep old accounts open even if you never use them. Shop multiple lenders within a short window so the inquiries count as one. Use pre-qualification tools before you apply. Watch individual card utilization, not just your overall number. Ask about pay-for-delete before handing over money on any collection account. Check your actual FICO score at myFICO or through Experian before you apply for anything major. Know that 760 is effectively the ceiling for most lenders and stop chasing higher.

None of this changes the system. Knowing how it actually works is the only real advantage available to you inside it.

Frequently Asked Questions About Why Your Credit Score Exists

Why does your credit score exist at all?

Your credit score exists so lenders can estimate the probability that a borrower will repay debt, at scale, without relying on personal judgment. It was not designed for consumers. It was designed so banks could process millions of applications quickly using historical repayment data. The three companies that maintain your credit file make money by selling that data to lenders. You are the subject of the system, not its intended beneficiary.

Who actually benefits from the credit scoring system?

Lenders benefit most. Credit scores allow them to price loans based on predicted risk and sort borrowers efficiently. Credit bureaus also benefit because collecting and selling borrower data is their entire business. Consumers interact with the system because modern financial life requires it, not because it was designed with them in mind.

Why do people with no credit history struggle to get approved for anything?

Because scoring models rely on past borrowing behavior to make predictions. No credit history means no data. The model cannot make a prediction with no input, so it defaults to treating you as an unknown risk. This creates a catch-22: you need credit to get credit, and there is no clean way around it without deliberately building a file from scratch using a secured card or becoming an authorized user on someone else’s account.

Can your credit score affect things besides loans?

Yes. Insurance companies in most states use credit-based scoring to set premiums. Landlords pull credit reports before approving rental applications. Some employers check credit reports during background screenings, particularly for jobs involving financial responsibility. Utility companies and phone carriers can factor in credit history. The system reaches far beyond borrowing.

What is the fastest way to raise a credit score?

Paying down the balance that appears when your credit card statement closes. The statement close date is when your balance gets reported to the bureaus. Paying before that date, not just before the due date, lowers what gets reported. That change can move the score within a single billing cycle. It is faster than any other lever available.

Why does paying off a loan sometimes make your credit score go down?

Paying off a loan closes an active account and removes ongoing repayment data from your file. The model now has fewer signals to read. You are financially stronger, but the dataset is smaller. The score typically recovers on its own once the rest of your file adjusts.

Do credit bureaus know how much money you make or have in the bank?

No. Credit bureaus track borrowing behavior only: loans, credit cards, payment history, and collections. They do not have access to your income, bank balances, or savings. You can earn very little and have an excellent score, or earn a great deal and have a poor one. Income is not a factor in any major credit scoring model.

Is it true you need to carry a balance to build credit?

No. This is a myth that benefits credit card companies and costs consumers money. Scoring models reward on-time payment history and low utilization. They do not reward paying interest. Paying your full balance every month builds exactly the same credit history as carrying debt, at zero cost in interest.

Does applying to multiple lenders hurt your credit score more than applying to one?

Not if you do it within a short window. Multiple mortgage or auto loan inquiries within roughly 14 to 45 days are typically counted as a single inquiry by scoring models that recognize rate shopping. You can apply to several lenders to find the best rate without multiplying the score impact. The lending industry does not advertise this because shopping around costs lenders money.

What is the 760 credit score ceiling?

Most lenders treat scores of 760 and above the same way when pricing loans. Crossing that threshold typically means you qualify for the lender’s best available rate. Going from 760 to 820 or 850 does not improve your terms. If your score is already above 760, chasing a higher number is not a productive use of your energy. You have already reached the point where the score stops mattering to the lender.

What does the word educational mean when used to describe a free credit score?

When Equifax and others describe consumer-facing scores as educational, they mean those scores are approximations intended to give you a general sense of your standing, not to replicate the exact number a lender will use. The score you see on a free app may be calculated by a different formula, using different weights, than the score your mortgage lender pulls. The gap can be 20 to 40 points or more. The word educational is the bureaus’ way of acknowledging that discrepancy without advertising it.

Where can I check my actual FICO score for free before applying for a loan?

Experian offers a free FICO Score 8 on their site. American Express MyCredit Guide offers a free FICO Score 8 from Experian and you do not have to be an Amex customer. Many banks and credit unions provide free FICO scores to account holders. For mortgage-specific or auto-specific FICO scores that lenders actually pull, myFICO.com offers those on paid plans starting around $20 a month. For the underlying data your scores are built on, AnnualCreditReport.com is the only federally authorized source for free reports from all three bureaus.