Car insurance is a rigged game, and it is rigged in one very specific direction: toward the people who never question it. The bill shows up, gets paid, and life moves on. Year after year, even as the number quietly climbs. That is not an accident. That is the business model. When money is already stretched, this bill can feel untouchable, like it is just what it costs. But car insurance is one of the most negotiable recurring expenses you have, and the industry is built entirely on the assumption that you will not do anything about it. This article is not going to give you the same tired tips you have seen a hundred times. It is going to show you how car insurance pricing actually works, what the industry keeps quiet, and exactly what to do about every single piece of it.

The Loyalty Penalty: How Staying Costs You More

Most people assume that being a long-term customer earns them a better rate. That is the opposite of how it works.

Insurance companies use something called price optimization. They collect data on your payment behavior, your shopping habits, and your history with the company. Then they use that data to figure out the highest price you are likely to tolerate before you finally leave. If their data says you are not a shopper, your rate goes up. Not because you became a riskier driver. Because they calculated they can charge you more and you probably will not notice.

Consumer Reports called it the “schmo tax.” The Consumer Federation of America investigated it and found that two drivers with identical risk profiles, same car, same record, same everything, can pay up to 30 percent different rates simply because one shops around and one does not.

Some states have banned price optimization. Most have not. Which means the best defense is the same thing the industry hopes you will not bother doing: shopping your rate every single year.

And here is the part that really stings. Those loyalty discounts your insurer offers can be a sleight of hand. An insurer may raise your rate 25 percent and then offer you a 10 percent loyalty discount. You feel rewarded. You are still paying 15 percent more than you were. The discount exists to make you feel like staying is working in your favor. Often it is not.

Step 1: Shop Your Car Insurance Rate Every Single Year

This is the single highest-impact thing you can do to cut what you pay. Get quotes from at least three companies every year, before your renewal date.

The same coverage on the same car with the same driver can vary by $300 to $800 per year depending on which company you are with. There is no consistently cheapest option. Which one is cheapest for you depends on factors specific to your situation, which is exactly why you have to shop every year without exception.

Where to get quotes:

- Direct from insurers: State Farm, GEICO, Progressive, Allstate, USAA if you are military or a veteran

- Independent agents: They quote multiple companies at once, which saves time

- Comparison sites: The Zebra, NerdWallet, and similar tools pull multiple quotes at the same time so you are not filling out the same form over and over

Set a reminder 30 days before your renewal date. That is when you have the most leverage. You can switch without any gap in coverage, and your current insurer knows it.

Before you switch, call your current insurer and tell them what you found. Ask them to match it. Many will, especially if you have been a customer for a while and have a clean record. You do not have to threaten to leave. Just tell them what you found and ask what they can do. That conversation takes ten minutes and can save you hundreds.

Step 2: Raise Your Deductible Once You Have a Small Cushion

Your deductible is the amount you pay out of your own pocket before insurance covers the rest. A higher deductible means a lower monthly premium.

Moving from a $500 deductible to a $1,000 deductible can reduce your collision and comprehensive premiums by 10 to 20 percent.

The catch is real: you need to actually have that amount accessible if you ever make a claim. This step only makes sense once you have a small cushion saved. If you are still working on building that buffer, this guide on building an emergency fund while living paycheck to paycheck walks through how to do it when money is already tight. Once that $1,000 is sitting there, raising your deductible becomes one of the simplest ways to lower what you pay every month.

Step 3: Review What Coverage You Actually Need

Not all coverage is equally valuable for every driver, especially if you are driving an older car. Here is how to think through it without getting talked into paying for things that do not make sense for your situation.

Liability coverage is required in almost every state. It covers damage you cause to other people and their property. Do not reduce this one. It is what stands between you and being financially wiped out if you cause an accident that seriously injures someone. State minimums are often dangerously low, and here is why that matters: a single serious injury claim can easily run $200,000, $400,000, or more. If your coverage tops out at $25,000, you owe the rest personally. That debt does not go away. Most people would be far better protected with at least $100,000 per person and $300,000 per accident. The difference in cost between bare minimum coverage and that level of protection is usually small, somewhere between $10 and $30 a month. The difference in what it protects you from is not small at all. That is not a place to cut corners.

Collision coverage covers damage to your own car when you are in an accident. If your car is older and low in value, run the math before you keep paying for it. If your car is worth $2,500 and you are paying $600 per year for collision with a $500 deductible, the most you could ever collect from a total loss claim is $2,000, and that is if the insurer agrees with your valuation. Paying $600 a year for a maximum payout of $2,000 looks different when you put it on paper. Before you drop it, though, understand exactly what you are giving up: if the car is totaled or stolen, you walk away with nothing from your insurer. For some people with older low-value cars that is a reasonable trade. For others it is not. Run the number on what your car would actually sell for today before you decide.

Comprehensive coverage covers theft, weather damage, a tree falling on your car, and anything else that is not a collision. Same math applies as collision when the car is older and low in value. Same warning applies too. Drop it and you are self-insuring for those losses.

Personal injury protection and medical payments coverage pays your medical bills after an accident regardless of who was at fault. Worth keeping if you do not have solid health insurance. Less critical if you do, but worth knowing what your health plan actually covers before you make that call.

A simple rule of thumb: if your car is worth less than ten times the annual premium for collision and comprehensive combined, dropping those coverages is worth considering. But consider the full picture, not just the monthly savings.

One important exception: if you are still making payments on the car, this decision may not be yours to make. Most lenders require you to carry both collision and comprehensive coverage for the entire life of the loan. It is written into your loan agreement. Drop those coverages without telling your lender and you are technically in default, which means they can force-place their own insurance on the car, charge you for it, and add it to your loan balance. That forced coverage protects the lender, not you, and it costs significantly more than a standard policy. If the car is financed, check your loan agreement before you touch anything in this section.

What “Full Coverage” Actually Means and Why the Term Is Designed to Confuse You

“Full coverage” is not a legal term. It is not a defined category. It is industry shorthand, and it means something different depending on who says it.

Two people can both have “full coverage” and have completely different actual protection. The term typically refers to liability plus collision plus comprehensive. But it does not automatically include uninsured motorist coverage, personal injury protection, medical payments, rental reimbursement, or roadside assistance. Those are all separate add-ons.

When someone tells you they have full coverage, or when you think you have full coverage, pull out your declarations page, which is the summary document your insurer sends you that lists every coverage you are actually paying for, and read what is on it. The false confidence that comes from thinking you are fully covered is something the industry rarely corrects, because it keeps people from asking hard questions. Do not be that person. Read the page.

The Truth About Bundling: It Is Not Always Cheaper

Bundling your auto and home or renters insurance with the same company gets pushed hard. Agents bring it up constantly. Insurers advertise it everywhere. There is a reason for that, and it is not purely because it saves you money.

Bundling is sticky. When two policies are tied together, switching becomes more complicated and most people do not bother. That reduced likelihood of shopping is worth a lot to an insurer. The discount they offer you for bundling is often less than what they gain by making you less likely to leave.

That does not mean bundling is always a bad deal. Sometimes it genuinely is cheaper. But here is what the industry does not tell you: sometimes two separate policies from two separate companies is cheaper than the bundle, even after the discount.

The only way to know is to price it both ways every single time. Get a bundled quote. Then get separate quotes for auto and home or renters individually. Compare the total. Do not assume the bundle wins just because there is a discount attached to it. A discount off an inflated rate is not necessarily a good deal.

What Your Credit Score Is Really Doing to Your Car Insurance Bill

This is one of the most important things to understand about how car insurance actually works, and it is almost never explained plainly.

In most states, your credit score can affect your car insurance premium more than your actual driving record. Read that again. A poor credit score can cost you as much as, or more than, having an at-fault accident on your record. Not a little more. Significantly more.

A study by the Consumer Federation of America found that drivers with poor credit can pay 50 to 100 percent more for car insurance than drivers with excellent credit, even with identical driving records. In some states the gap is even wider.

Insurance companies use what is called an insurance risk score. It is built from your credit history but it is not the same number as your regular credit score. You have a legal right to know that this score is being used. You do not have a legal right to see the actual number. They run it quietly in the background when they quote you, and they are not required to tell you how much it moved your rate.

What that means practically: if your credit has improved since you last applied or renewed, shop your insurance immediately. Your updated credit history factors into any new quote automatically. Improving your credit is not just about getting approved for loans or cards. It directly affects what you pay for car insurance every single month. If you want to understand the full picture of how your credit score is being used against you, this breakdown of why your credit score exists and who it actually serves is worth reading. That connection between credit and insurance is rarely made explicit, and it costs people real money.

Your Secret Insurance File: The CLUE Report

Most people have never heard of this. That is exactly how the industry prefers it.

When an insurer sets your rate, they do not just look at your driving record. They pull something called a CLUE report. CLUE stands for Comprehensive Loss Underwriting Exchange. It is a database maintained by a company called LexisNexis that tracks up to seven years of your insurance claims history. Over 99 percent of auto insurers report to it and pull from it every time they quote you.

Here is what most people do not know: even claims where nothing was paid out, and even casual inquiries you made without officially filing anything, can show up on your CLUE report and be used to push your rate up.

You are entitled to one free CLUE report per year under federal law. Pull it before you shop your insurance every year. If there are errors, inaccurate claim information, or incidents listed that do not belong to you, you can dispute them. Errors on a CLUE report can raise your rate without you ever understanding why. You can request your report at the LexisNexis Consumer Portal or by calling 1-866-312-8076.

Think Carefully Before You File Small Claims

This is one of the most counterintuitive things about car insurance, and almost no one explains it when you sign up.

Filing a claim, even a small one, even one where you are not at fault, goes on your CLUE report and can raise your rate at renewal. Insurers treat frequent claims as a signal of future claims, regardless of fault or circumstance. A small fender bender claim that pays out $800 can end up costing you significantly more in increased premiums over the next three to five years than if you had simply paid for the repair yourself.

Before filing any claim, run the math. How much is the damage? What is your deductible? What is the likely rate increase if you file? For smaller incidents, paying out of pocket and keeping your record clean is often the smarter financial move over the long run.

If you want to think it through before deciding, call your insurer and ask a general question about the process without formally opening a claim. Be explicit that you are making an inquiry only. Some insurers log inquiries regardless, so ask directly whether an exploratory call will be noted on your record before you say anything else.

The Discounts You Are Probably Not Getting

Insurance companies have discounts most customers never use simply because they never ask. Some are applied automatically. Many are not, and no one volunteers them.

- Safe driver or clean record: Usually automatic after a clean period, but worth confirming you are actually receiving it

- Low mileage: The national average is around 13,500 miles per year. If you drive significantly less, ask about a low mileage discount specifically

- Paid in full: Paying your full annual premium at once often comes with a discount

- Paperless billing and autopay: Small, but easy

- Defensive driving course: Completing an approved course can reduce your rate

- Vehicle safety features: Anti-theft devices and newer safety technology may qualify

- Occupation or group affiliation: Some insurers offer discounts for certain employers, professional associations, or alumni groups. Worth asking even if you think it probably does not apply

- Good student discount: If you have a student on your policy, some insurers discount for a B average or better

Ask your agent directly: “What discounts am I currently receiving, and what might I qualify for that I am not getting?” That one question has caught savings people had no idea existed.

Usage-Based Insurance: The Discount That Can Backfire

Several insurers offer programs that track your driving through an app or a small device plugged into your car, and then base your rate on how you actually drive. If you drive conservatively and put in fewer miles than average, these programs can save you real money. Progressive’s Snapshot, State Farm’s Drive Safe and Save, and Metromile, which charges per mile driven, are examples worth looking into.

But here is what does not make it into the ads.

Some companies, including Allstate, GEICO, Liberty Mutual, Progressive, and Travelers, can raise your rate if the program determines you are a risky driver. Hard braking, late-night driving, phone detection, and even where you tend to drive can count against you. You are essentially handing them an audit of your driving habits with no guarantee the audit goes in your favor.

A Maryland study found that in 2023, only 31 percent of drivers enrolled in these tracking programs actually saw their premium go down. Twenty-four percent saw it go up. Forty-five percent saw no change at all. The savings advertised are usually the maximum possible discount, not what most people actually receive.

Before you sign up, ask your insurer one specific question: can this program raise my rate, or can it only lower it? That answer changes everything about whether it makes sense for you.

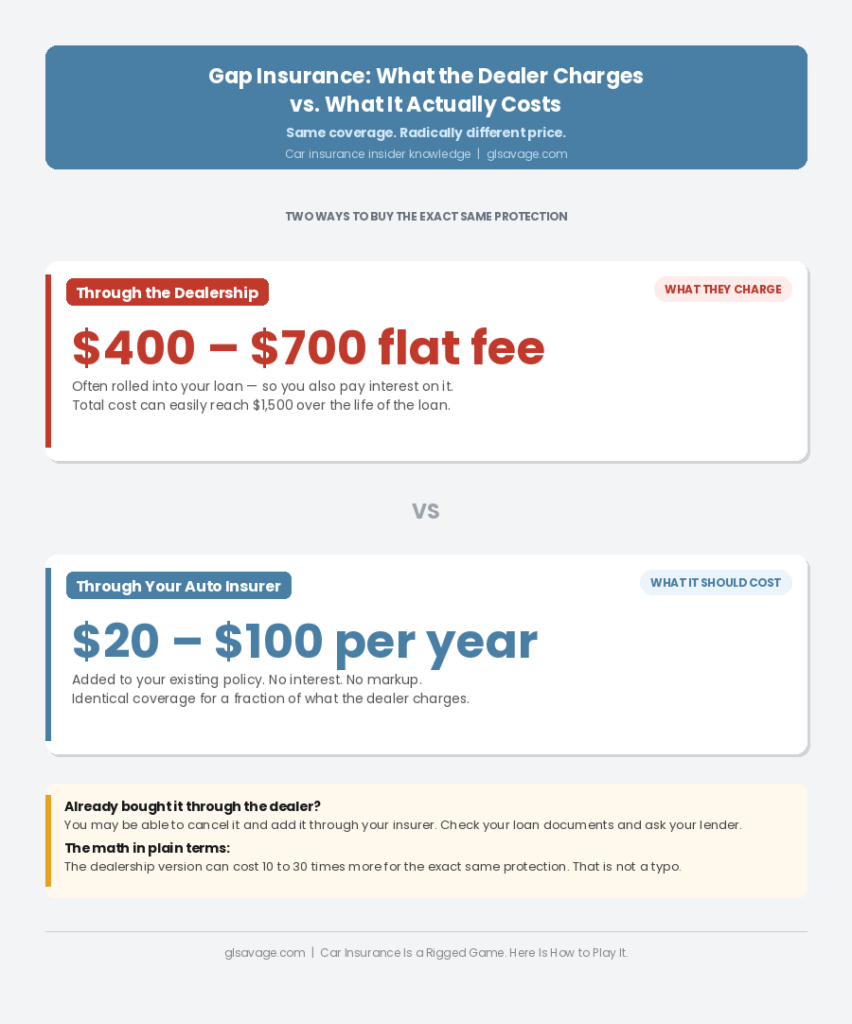

Gap Insurance Through the Dealer: One of the Biggest Markups You Will Ever See

If you financed a car and bought gap insurance through the dealership, this section is for you.

Gap insurance covers the difference between what your car is worth and what you still owe on your loan if the car is totaled. It is genuinely useful when you owe more than the car is currently worth, which is common in the first few years of a loan because cars lose value faster than loan balances drop.

Through a dealership, gap insurance typically costs $400 to $700 as a flat fee, often rolled into your loan. Which means you are also paying interest on it. Total cost can easily reach $1,500 depending on the dealer and the loan terms.

Through your auto insurer, the same coverage typically costs $20 to $100 per year. That is not a typo. The dealership version can cost ten to thirty times more for identical protection.

If you already bought it through the dealer, you may be able to cancel it and add it through your insurer instead. Check your loan documents and call your lender to ask. The refund on the dealer policy, combined with the lower annual cost through your insurer, can put real money back in your pocket. If you are carrying other debt on top of a car loan, understanding how minimum payments work is worth your time too, because the math is similar: what looks manageable month to month can cost you far more than you realize over the life of the debt.

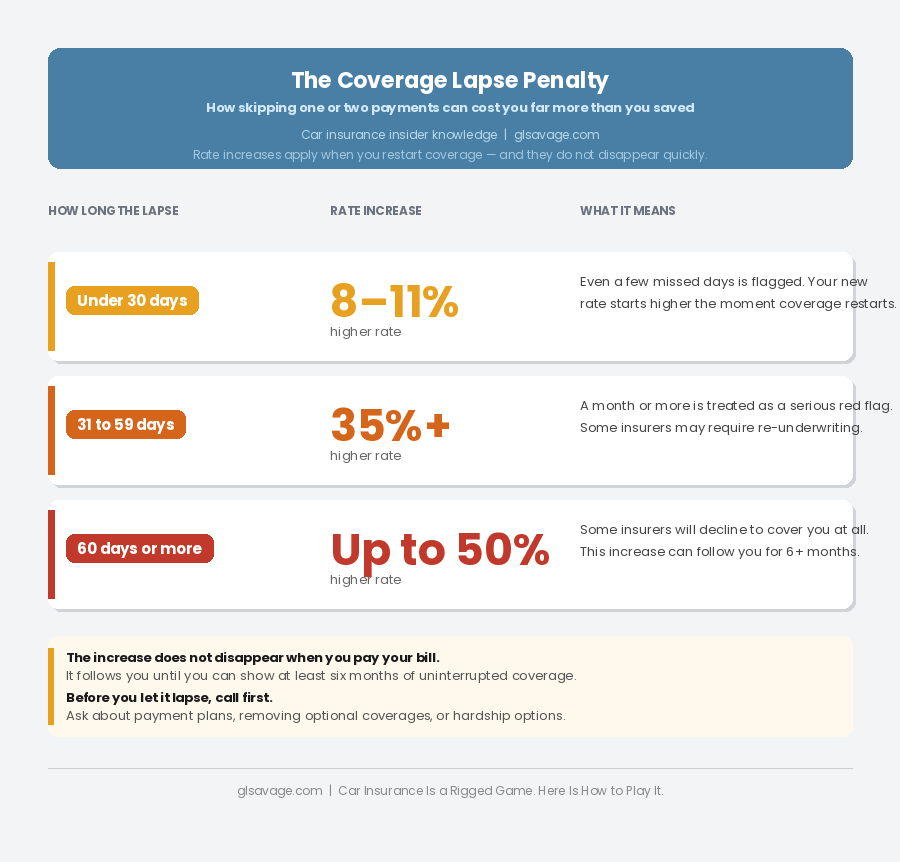

The Coverage Lapse Trap

When money gets tight, letting your insurance lapse for a month or two to save the premium can feel like a reasonable short-term move. It almost always costs more in the end.

A lapse of even a few days signals higher risk to every insurer you approach afterward. A lapse under 30 days can raise your new rate by 8 to 11 percent. A lapse of 31 days or more can raise it by 35 percent or more. A lapse of 60 days or longer can push increases toward 50 percent, and some insurers may decline to cover you at all.

That rate increase does not disappear when you pay your bill again. It follows you until you can demonstrate a consistent history of uninterrupted coverage, which typically takes at least six months of continuous insurance. When you are already stretched thin, the financial pressure that causes a lapse and the higher rates that follow it can become a cycle that is hard to break. If you are in that position, understanding how banks make money from the fees that hit hardest when money is tight is useful context for seeing how the whole system is designed to compound the problem.

If you are struggling to afford your premium, call your insurer before you let it lapse. Ask about payment plans. Ask about temporarily removing optional coverages. Ask whether they have any hardship options. A temporary reduction in coverage is almost always better than a lapse that costs you more every month for the next year.

Your Zip Code Is Affecting Your Rate More Than You Realize

Insurers price by location down to the neighborhood level. Crossing a zip code line can shift your rate by 20 to 30 percent. That is not a small difference. It is almost never discussed, and it is completely legal.

If you move, update your insurer immediately and get new quotes from competitors at the same time. Cheap car insurance in your old zip code is not automatically cheap car insurance at your new address. The market is different at every location. You want to know what it looks like before your renewal auto-processes and the decision gets made for you.

How to Play a Rigged Game

The car insurance industry counts on confusion, inertia, and the assumption that most people will not look too closely at how the pricing actually works. Shopping your rate every year, pulling your CLUE report, understanding what your credit score is doing to your premium, asking about every discount, and making one phone call before you renew can easily save $300 to $800 on coverage that does not change at all. For people who are already stretched thin, that is not a small number. That is a utility bill. That is groceries. That is breathing room. The bill does not have to stay where it is. You just have to be willing to look at it.

Frequently Asked Questions About How Car Insurance Actually Works

Every year, before your renewal date. The loyalty penalty is real and documented. Annual shopping is the single most effective defense against price optimization, and it consistently results in lower rates than staying with the same insurer indefinitely.

No. Insurance companies use a soft inquiry to check your credit, which does not affect your score. You can get as many quotes as you want without any impact.

Not always. Sometimes two separate policies from two separate companies is cheaper than the bundle even after the discount. Price it both ways every time. Get a bundled quote and separate quotes and compare the total. Do not assume the bundle wins just because a discount is attached to it.

More than most people realize. In most states, a poor credit score can raise your premium by 50 to 100 percent compared to someone with excellent credit and an identical driving record. Improving your credit is one of the highest-impact things you can do to lower your car insurance bill long term.

Yes. A CLUE report is your insurance claims history, maintained by a company called LexisNexis. Over 99 percent of auto insurers pull it when setting your rate. It covers up to seven years of claims, and errors on it can raise your rate without you ever knowing why. You are entitled to one free report per year. Pull it before you shop at the LexisNexis Consumer Portal or by calling 1-866-312-8076.

Yes, with some insurers it can. Before enrolling, ask your insurer specifically whether the program can increase your rate or only decrease it. That answer matters before you hand over your driving data.

Often it is not. A small claim goes on your CLUE report and can raise your rate at renewal by more than the claim paid out. For minor damage, run the math first. Paying out of pocket and keeping your record clean is sometimes the cheaper move over the long run.

Only once you have the deductible amount accessible in savings. If you raise your deductible to $1,000 and do not have $1,000 available, you are exposed to real financial strain after any accident. Build the cushion first, then make the move.

If the car is totaled or stolen, your insurer pays nothing toward replacing it. You absorb that loss entirely. For a car with very low value that math may make sense. For a car that you depend on and could not replace easily, think carefully before dropping those coverages just to save a few dollars a month.