When a debt collector calls, most people do one of two things: panic and pay, or panic and ignore. Neither is the right move. There is a third option that most people have never heard of, and it is built directly into federal law. You can demand that the collector prove the debt is real, that the amount is accurate, and that they actually have the legal right to collect it. This is called debt validation, and it costs you nothing but a certified letter. What it can cost the collector is everything, because a surprising number of them cannot produce the proof.

What Debt Validation Actually Is

Debt validation is the legal right, under the Fair Debt Collection Practices Act, to demand that a debt collector verify the details of a debt before you pay it or engage with it any further. It is not a loophole. It is not a trick. It is a federal consumer protection that has existed since 1977 and that most people carrying debt have never used.

The law works in two directions. First, within five days of first contacting you, a collector is legally required to send you a written notice containing the amount of the debt, the name of the creditor, and notice of your right to dispute the debt within 30 days. This is called the validation notice. If a collector contacts you and does not send this notice, they have already violated the law.

Second, if you dispute the debt in writing within 30 days of receiving that notice, the collector must stop all collection activity, including calls and letters, until they provide you with adequate verification. Under the CFPB’s rules, credit reporting is also treated as a collection activity that should pause during a pending dispute. Not a printout. Not a form letter. Verification of the debt: documentation that the debt exists, that the amount is accurate, and that they have the right to collect it. If they cannot provide that, collection stops.

Most people never send the letter. They assume the collector has the paperwork. Frequently, especially when dealing with debt buyers, the collector does not have the paperwork, and they are counting on you not asking for it. For more on who is actually calling when a collector contacts you, read The Debt Collector Is Not Who You Think It Is.

Why Debt Buyers Often Cannot Validate

Debt buyers often cannot validate because they never had the paperwork to begin with.

When a debt gets sold, the buyer typically receives an electronic file with basic information: your name, an account number, a balance. They rarely receive the original credit agreement, the complete payment history, or signed documentation proving the debt was yours to begin with. The more times a debt has changed hands, the thinner the paper trail gets.

A debt buyer who paid four cents on the dollar for a portfolio of ten thousand accounts does not have the original contract for each one. They have a spreadsheet. When you demand debt validation, you are asking them to produce documentation they may have never had. Many cannot do it. When they cannot do it, they cannot legally continue collecting. They cannot call you. They cannot send letters. They cannot report the debt to the credit bureaus. They cannot sue you. The collection stops.

This does not mean the debt disappears. If the original creditor has the paperwork, the account can be sent to a different collector who can validate. But the specific collector who contacted you, operating on a purchased portfolio with no documentation, has no legal standing to pursue you further if they cannot verify what you owe.

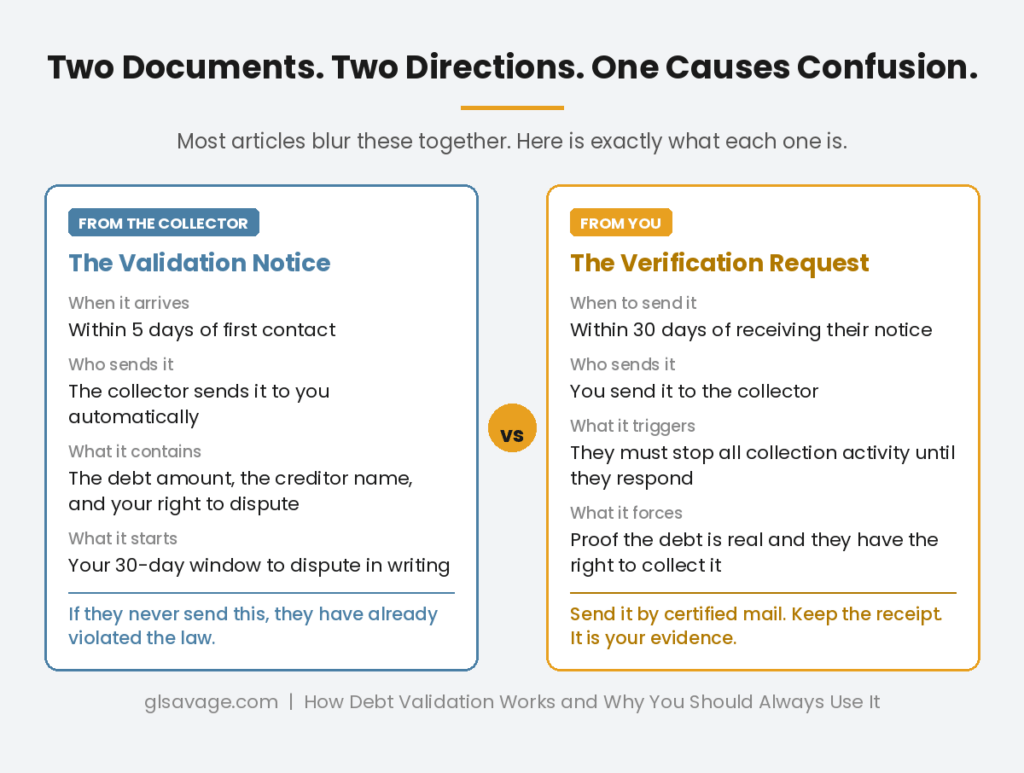

The Validation Notice vs. the Verification Request: Two Different Things

Most articles about debt validation use the terms validation and verification interchangeably, which creates genuine confusion about who does what and when. They are two different documents going in two different directions.

The validation notice comes from the collector to you. It is the initial notice they are legally required to send within five days of first contact, telling you the amount owed, the creditor’s name, and your right to dispute. You receive this. You did not ask for it. The collector is required to send it.

The verification request comes from you to the collector. This is the letter you send within 30 days of receiving the validation notice, formally disputing the debt and demanding that the collector prove it. You send this. The collector did not ask for it. Your sending it triggers their legal obligation to stop all collection activity until they respond.

Knowing which document does what matters because the 30-day window runs from when you receive the validation notice from them, not from when the collector first calls you. If a collector only calls and never sends a written notice, the 30-day clock has not started. But the collector has also already violated the FDCPA by failing to provide the required validation information within five days of first contact.

What the Collector Must Actually Prove

When you send a verification request, what are you entitled to receive? The FDCPA does not define verification precisely, and courts have interpreted the standard more narrowly than most people expect. The majority rule, established in federal circuit courts, is that verification requires the collector to confirm in writing that the amount being demanded is what the creditor claims is owed. That is a lower bar than most consumers assume. The collector is not legally required to produce the original signed contract, detailed account statements, or a chain of ownership history simply because you asked.

That said, the verification must come from the creditor, not just from the collector’s own files. A printout of what is already in the collector’s system, generated internally without any confirmation from the original creditor, does not satisfy the requirement. The response must connect back to what the original creditor is claiming. If the collector sends you something that clearly does not do that, you can dispute the adequacy of the response in writing. And critically, if a collector cannot produce even this basic level of confirmation and continues collecting anyway, every contact after your verification request is a separate FDCPA violation you can sue over.

If a collector fails to validate and continues to collect anyway, reporting the debt to the credit bureaus during a pending dispute is a violation. Under the CFPB’s Regulation F, credit reporting is treated as a collection activity that must pause when a timely dispute is pending. Separately, the Fair Credit Reporting Act requires any disputed account to be marked as disputed in any credit bureau report. If a collector reports without the dispute notation, or continues reporting an account it cannot validate, that is a potential violation of both laws. Document every contact and every credit report pull after sending your verification request. That documentation is evidence.

The 30-Day Window and What Happens If You Miss It

The 30-day dispute window is real and it matters, but missing it is not the end of your options.

Within 30 days of receiving the validation notice, your verification request triggers the legal obligation for the collector to stop collection activity until they respond. After 30 days, the collector is allowed to assume the debt is valid and continue collection. You lose the automatic pause on collection activity that comes with a timely dispute.

However, you can still send a verification request after 30 days. The collector is not required to stop collecting while they respond, but they are still legally obligated not to collect on a debt they cannot verify. Many collectors, especially unsophisticated debt buyers, will still be unable to produce documentation regardless of when you ask. A late verification request can still expose the same documentation problems. It just does not come with the automatic pause that a timely request provides.

If the 30-day window has passed and a collector contacts you about a debt you believe is invalid, inaccurate, or past the statute of limitations, send the verification request anyway. Note in the letter that you are disputing the debt, request all documentation of ownership and the basis for the amount claimed, and send it by certified mail with return receipt. The collector’s response, or failure to respond adequately, still determines what they can legally do next. For a refresher on your rights around the statute of limitations, read Statute of Limitations on Debt: The Clock They Hope You Do Not Know About.

How to Send a Debt Verification Request That Works

The letter does not need to be complicated. What it needs to be is written, specific, sent within the 30-day window if possible, and documented with proof of delivery.

Address it to the collection company by name and include the account number or reference number from their notice to you. State clearly that you are disputing the debt and requesting verification. Ask for the name and address of the original creditor, documentation that they have the right to collect this debt, an itemization of the amount including how interest and fees were calculated, and confirmation of the date of first delinquency on the original account. You are not required to explain why you are disputing or provide any additional information about yourself beyond what is needed to identify the account.

Send it by certified mail with return receipt requested. Keep the receipt and the green card when it comes back. Those two documents are your proof that the letter was sent, when it was sent, and that the collector received it. If you later need to file a complaint with the CFPB, the FTC, or your state attorney general, or if you need to sue the collector for FDCPA violations, those documents are the foundation of your case.

The CFPB provides sample letters at consumerfinance.gov that you can use as a starting point. You do not need an attorney to send a verification request. The letter is straightforward and your right to send it is absolute within the 30-day window.

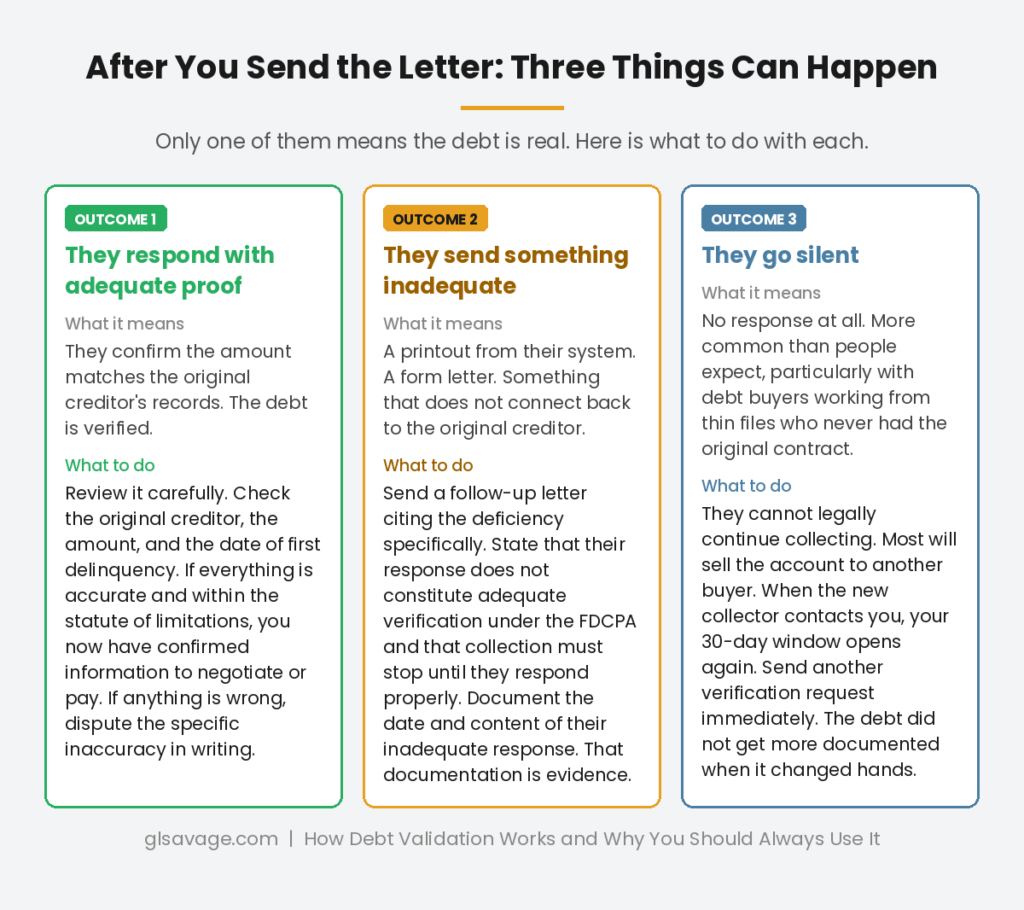

What Happens After You Send the Letter

Three things can happen after a collector receives your verification request.

They provide adequate documentation. They confirm the debt belongs to you, the amount is accurate, and they have the right to collect it. If the debt is legitimate and within the statute of limitations, you now have to decide what to do with confirmed information. That might mean disputing specific inaccuracies, negotiating a settlement, or setting up a payment plan. But you made them prove it first, which is always worth doing. A verified debt is harder for a scammer to produce and harder for an error-prone debt buyer to get right.

They provide inadequate documentation. A printout, a form letter, or a generic notice that does not actually confirm the details. This is not verification under the law. You can send a follow-up letter specifically citing the deficiency and reiterating that they must stop all collection activity until they respond adequately. Note the date and method of their inadequate response. Document everything.

They do not respond at all. This is more common than people expect, particularly with debt buyers working from thin files. A collector who cannot produce documentation simply goes quiet. They cannot legally continue collecting. Most will sell the account to another buyer and the process starts over with a different company. When that happens, your 30-day window opens again with the new collector. Send another verification request. The debt did not get more documented when it changed hands.

When Validation Is Especially Important

Debt validation matters every time a collector contacts you, but it is particularly important in specific situations.

When you do not recognize the debt. Collectors contact the wrong people regularly, either because of similar names, old addresses, or errors in the data they purchased. Demanding validation before engaging with the debt at all is the only way to confirm whether it belongs to you.

When the debt is old. Old debt changes hands repeatedly and the paper trail gets thinner with each sale. A collector working from a seven-year-old account has almost certainly never seen the original contract. Validation will expose that.

When the amount does not look right. Debt buyers sometimes add fees and interest that were not in the original contract or that exceed what state law allows. Demanding an itemization forces them to show their math. If the math does not hold up, the amount is wrong and you do not owe what they are claiming.

When you suspect a scam. Fake debt collectors are a documented and growing problem. They use real personal data from breaches to sound credible. A legitimate collector can validate. A scammer cannot. The verification request is your filter. If they cannot produce documentation from the original creditor, the call is not legitimate. For more on how to identify scam collectors versus legitimate ones, read The Debt Collector Is Not Who You Think It Is.

Debt validation is not a way to avoid paying debts you legitimately owe. It is a way to make sure you are only paying debts that are real, accurate, and legally collectible. The collector knows what they have in the file. Using debt validation means you will too. That changes who holds the power in the conversation.

Frequently Asked Questions

What is debt validation and how does it work?

Debt validation is your federal right under the Fair Debt Collection Practices Act to demand that a debt collector prove a debt is real and accurate before you pay it. When you send a written verification request within 30 days of receiving the collector’s initial notice, they must stop all collection activity including credit bureau reporting until they provide adequate documentation. If they cannot verify the debt, collection stops entirely.

What must a debt collector send me when I request debt validation?

Courts have interpreted the verification standard narrowly. The majority rule requires the collector to confirm in writing that the amount being demanded is what the creditor claims is owed. They are not legally required under federal law to produce the original signed contract or a chain of ownership documents simply because you asked. However, the confirmation must come from the original creditor, not just from the collector’s own internal records. A printout of the collector’s own files without any verification from the creditor does not satisfy the requirement. And if the collector cannot produce even that basic confirmation and continues collecting, they are violating the FDCPA.

What happens if a debt collector cannot validate the debt?

If a collector cannot provide adequate verification, they must stop all collection activity. They cannot call you, send letters, report the debt to the credit bureaus, or file a lawsuit while the debt is disputed and unverified. Many debt buyers, who purchase large portfolios of old accounts with minimal documentation, genuinely cannot produce the paperwork for every account they hold. When they cannot validate, collection stops.

Do I have to send a debt validation letter within 30 days?

Sending the letter within 30 days of the collector’s initial notice gives you the strongest protection, including the automatic pause on collection activity while they respond. After 30 days, the collector can assume the debt is valid and continue collecting. However, you can still send a verification request after 30 days and the collector is still not allowed to collect on a debt they cannot verify. It just does not come with the same automatic pause.

What is the difference between a debt validation letter and a debt verification letter?

They are two different documents. The validation notice comes from the collector to you, sent automatically within five days of first contact, telling you the debt amount and your rights. The verification request, sometimes called a debt verification letter, comes from you to the collector, demanding proof that the debt is real and legally collectible. These go in opposite directions and have different legal consequences.

Can a debt collector still sue me after I request validation?

If a lawsuit has already been filed, the legal process continues regardless of your validation request. A verification request pauses collection activity, not an active lawsuit. If you receive a court summons, you must respond to it separately and by the deadline on the summons regardless of whether you have sent a validation letter. The two processes run in parallel. Filing a new lawsuit while a dispute is pending is a gray area. The FDCPA’s cease-collection requirement does not explicitly bar a collector’s attorney from initiating legal action during the validation period. If you are sued on a debt you have disputed and not received validation for, raise that dispute as a defense in your response to the court and consult a consumer law attorney.

What should I do if a debt collector validates the debt?

Review the documentation carefully against your own records. Confirm the original creditor is correct, the amount matches what you believe you owed including any interest and fees, and the date of first delinquency is accurate. If you find inaccuracies, dispute them specifically in writing. If the debt is accurate, you now have confirmed information to work with, including the ability to negotiate a settlement or payment plan with the collector. A verified debt is also useful for checking the statute of limitations, since you now have the original dates.

Can I use debt validation to get a collection account removed from my credit report?

If a collector cannot validate the debt, they cannot report it to the credit bureaus. If they have already reported an unvalidated debt, that is a violation you can dispute directly with the bureaus by sending them a copy of your debt validation request and the collector’s failure to respond adequately. The bureau is required to investigate. If the collector cannot verify accuracy with the bureau, the account must be removed. For more on how collection accounts affect your credit and how to dispute them, read How Collection Accounts Affect Your Credit Report.