The freelancing pitch has been running for years and it has never once led with the math. It leads with the freedom. The laptop on a beach. The client who pays $150 an hour. The idea that you can finally stop trading your time for someone else’s benefit and start building something for yourself. That is not a lie. It is just the version of the story that ends before the costs start. Freelancing real pay is not your rate multiplied by your hours. It is what is left after the IRS takes its cut, the health insurance market takes its cut, the platforms take their cut, and the clients who pay late or not at all take the rest. That number is almost always lower than the number people plan around. Sometimes significantly lower. This article runs the full calculation, including the parts the freelance industry would rather you not think about until you are already in.

The Tax System Was Not Built With You In Mind

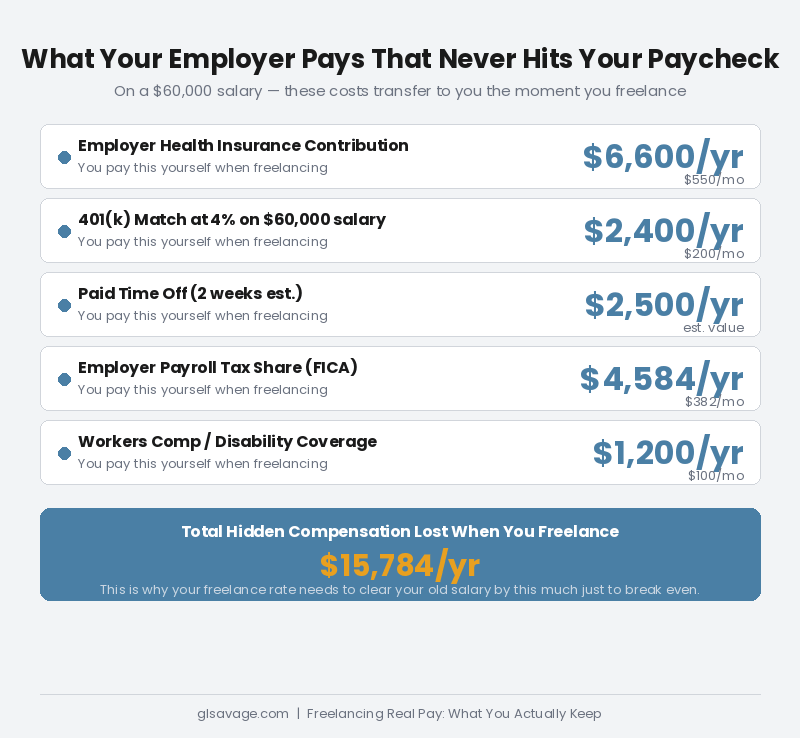

When you work for a company, your employer pays half of your Social Security and Medicare taxes. You never see it. It never touches your paycheck. It is just a cost the company absorbs because the law requires it. That cost is 7.65 percent of your wages, paid on your behalf, invisible to you the entire time you are employed.

The moment you go freelance, that cost transfers to you. All of it. You are now the employee and the employer, which means you pay both halves. The total is 15.3 percent. That is 12.4 percent for Social Security and 2.9 percent for Medicare. This is called self-employment tax, and it applies on top of your regular federal income tax, not instead of it. Two separate tax bills. Both owed. Both due.

In 2026, the Social Security portion applies to your first $184,500 in net earnings. Above that, no Social Security tax. The Medicare portion has no ceiling at all. And if your net earnings from self-employment exceed $200,000 as a single filer, you owe an additional 0.9 percent Medicare tax on top of the 2.9 percent. The government does not ease up as you earn more. It adds.

There is one offset worth understanding. The IRS lets you deduct half of your self-employment tax from your adjusted gross income, which is your income before most deductions are applied. Adjusted gross income is the starting number the IRS uses before it calculates your income tax bill. The logic is that employers can write off their half of payroll taxes as a business expense, so freelancers get a version of the same break. On $35,000 in net profit, you would owe roughly $4,945 in self-employment tax and could deduct about $2,473 from your income before calculating income tax. It helps. It does not come close to making you whole.

Most accountants who work with self-employed clients tell them to set aside 25 to 35 percent of every payment for freelancer taxes. That range exists because the right number depends on your income level, your state, and your deductions. In a state with no income tax you might land closer to 25. In California or New York with meaningful state income tax layered on top of federal, you are closer to 35 or higher. If you are setting aside nothing and planning to figure it out in April, you are heading for a bill that can take months to recover from.

You also pay four times a year. The IRS does not allow self-employed workers to wait until April to settle up. Freelancer taxes are not a once-a-year event. If you expect to owe more than $1,000 when you file, you are required to make quarterly estimated tax payments. The due dates are April 15, June 16, September 15, and January 15. Miss one and you owe a penalty on the unpaid amount on top of the taxes themselves. An employee never thinks about this because it is handled automatically on every paycheck. When you freelance, it is your job to know the dates, calculate the amounts, and make the payments. Every quarter. Every year.

One more thing almost no one knows until it surprises them: the minimum net earnings that trigger a tax filing requirement for a freelancer is $400. Not the standard deduction amount, which for employees runs over $14,000. Four hundred dollars. Do a few small jobs on the side and think you are below the radar. You are not. You may also find yourself owing self-employment tax on that amount even if you owe no income tax. The IRS calculates them separately.

Also new for 2026: the threshold for clients to send you a 1099-NEC form, which is the form that reports what they paid you, jumped from $600 to $2,000. That means if a client paid you $1,500, they are no longer required to send you a form. The IRS still expects you to report and pay taxes on that income. The form not arriving does not make the income disappear. It just means you have to track it yourself.

None of this was hidden from you by accident. The cost your employer absorbed on your behalf was real compensation that never showed up in a salary conversation.

Every Hour You Work Is Not an Hour You Get Paid For

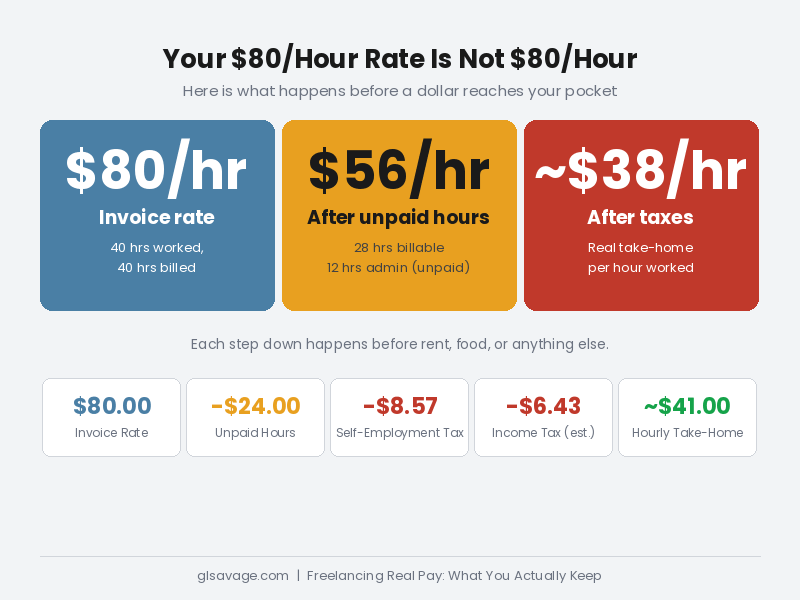

Here is the number the freelance industry never shows you. Freelancing real pay per hour is not your billing rate. It is your billing rate multiplied by the percentage of your working time that someone actually pays for. And that percentage is not 100. It is not close.

When you freelance, you run a business. Running a business takes time no client pays for. Finding clients. Writing proposals. Following up on proposals that go nowhere. Negotiating contracts. Sending invoices. Chasing late payments. Doing bookkeeping. Filing quarterly taxes. Managing your portfolio. Answering emails that are not attached to a paying project. All of that is your time. None of it goes on an invoice. The industry calls this non-billable time. You can call it the part of the job nobody warned you about.

Most established freelancers bill between 60 and 75 percent of their total working hours. The rest runs the operation. In a 40-hour week that is 25 to 30 billable hours. The other 10 to 15 hours are real work that produces zero direct income.

Put that in numbers. You bill $80 an hour and work 40 hours a week. If 30 percent of your time is non-billable, you are billing 28 hours. Your weekly gross is $2,240, not $3,200. Your effective hourly rate counting all the hours you actually worked is $56. Before taxes. Before health insurance. Before anything else. The number on your invoice and the number you actually earn are not the same, and the gap opens from the first week.

When work is slow, that gap gets worse. A week with two billable hours and fifteen administrative hours means your two billable hours are carrying the full cost of all fifteen hours of your time. Slow periods do not eliminate overhead. They just make it more expensive per dollar earned. This is one of the reasons Why a Second Job Often Costs More Than It Pays applies directly to freelancing taken on as supplemental income. The overhead time cost is real whether you bill five hours a week or forty.

Health Insurance Is the Cost That Ends the Conversation

Most people who leave a traditional job for freelancing underestimate exactly one cost more than any other. It is not taxes. It is health insurance.

When you have an employer-sponsored health plan, you pay a portion of the premium and your employer covers the rest. The total cost of that plan might be $700 a month for a single person. You pay $150. Your employer absorbs $550. That $550 is real compensation that shows up nowhere on your pay stub and nowhere in your salary negotiation. When you leave that job, you do not just lose the salary. You lose the $550 a month that was covering your medical coverage.

When you freelance, you buy your own coverage on the individual market. A comparable plan for a healthy person in their 30s can cost $400 to $600 a month before any subsidies. In your 50s, meaningfully more. At 64, the individual market can charge you three times what a 21-year-old pays for the same coverage in the same city. That is how age rating works under the Affordable Care Act, commonly called the ACA. It is legal. It is the structure of the market you are entering.

The ACA marketplace, found at healthcare.gov, is the primary option for most freelancers. Premium tax credits, which are government subsidies that reduce your monthly cost, are available based on your income and household size. At lower income levels you may qualify for Medicaid, which is free or very low cost. The complication is that freelance income is irregular, which means you are estimating your annual income when you apply. If you underestimate and receive more in subsidies than your actual income qualifies for, you repay the difference when you file your taxes. In a strong earning year, that repayment can land in the thousands.

Something changed in 2026 that most freelancers are not prepared for. The enhanced premium tax credits put in place during the pandemic in 2021 and extended through 2025 expired on January 1, 2026. Those credits made coverage significantly more affordable, particularly for people earning above 400 percent of the federal poverty level, which is roughly $63,000 for a single person. Above that threshold under the original ACA rules, you receive no subsidy at all. The enhanced credits softened that cliff for five years. As of this writing, the House has passed a three-year extension, but it has not cleared the Senate. Unless and until that extension passes, premium costs in 2026 are substantially higher than they were in 2025 for many freelancers. KFF, a nonpartisan health policy organization, estimated that subsidized enrollees’ out-of-pocket premium costs would more than double on average if the enhanced credits are not restored. A 60-year-old couple earning $85,000 could face annual premiums of over $22,600. Check KFF’s ACA subsidy calculator to estimate your own costs for 2026 based on your income and location.

Alternatives exist. Professional organizations in many fields offer group coverage to members that can undercut individual market rates. The Freelancers Union provides access to group options, some of which require forming a business entity with an EIN first. An EIN is an Employer Identification Number, essentially a Social Security number for a business. Health sharing plans also exist, but they are not regulated insurance products, can deny coverage for pre-existing conditions that an ACA-compliant plan would be required to cover, and carry different legal protections. Know exactly what you are and are not buying before you drop real insurance.

The self-employed health insurance deduction is one of the most valuable available and one of the least talked about. If you are self-employed and not eligible for coverage through a spouse’s employer plan, you can deduct the full cost of your health insurance premiums directly from your gross income. No itemizing required. That reduces your taxable income and the income tax you owe on it. You still pay the premium in full before the deduction helps you, but the government is not taxing you on money you spent to stay insured.

If Your Clients Do Not Pay, the IRS Does Not Wait

One of the structural facts about freelancing that nobody includes in the pitch is that you extend credit to your clients every time you work before you get paid. You deliver the work. You send the invoice. Then you wait. Sometimes a very long time.

Remote’s Contractor Management Report 2025 found that 85 percent of freelancers have their invoices paid late at least some of the time. More than one in five freelancers are paid late or not at all more than half the time. Not occasionally. More than half the time.

The financial damage is documented. One in five freelancers have found themselves without money to cover rent or bills because of a slow-paying client. Nearly a quarter have had to use a credit card or go into overdraft while waiting. A third of freelancers have completed work and received nothing. Not late. Nothing. The work was done, the client kept it, the money never came.

Here is what makes this worse specifically for freelancers: the IRS does not wait for your clients to pay you. You may owe taxes on income you have not yet collected depending on how the timing falls across tax years. You might be making a quarterly estimated payment out of personal savings on money that is sitting in someone else’s accounts receivable, which just means their pile of bills they owe but have not paid yet.

The protections exist but must be set up before the problem starts. A written contract with a clear scope of work, a defined payment date, a late fee clause, and a deposit requirement before work begins are standard business practices. They feel aggressive to freelancers who are new and afraid of losing a client. A client who refuses standard written payment terms before work begins is already showing you something worth knowing in advance.

New York State expanded its Freelance Isn’t Free Act statewide in 2024. It requires a written contract for work valued at $800 or more, mandates payment within 30 days of completing the work unless otherwise specified, and gives freelancers legal standing to pursue non-payment. Other states have similar protections at various stages of adoption. Knowing what your state offers before you take on a client costs you nothing. Finding out after you are owed money costs considerably more.

The Safety Net Does Not Exist for You

When an employee is laid off, there is a system. Unemployment insurance provides partial income replacement while they look for work. It is not generous. It is not permanent. But it exists, and it creates a financial buffer between losing a job and finding another one.

That system does not cover you. Self-employed workers, independent contractors, and freelancers cannot collect standard unemployment insurance in most states because the program is funded by employer contributions, and when you freelance, there is no employer contributing on your behalf. If your biggest client drops you, if your industry hits a slow period, if you get sick and cannot work for two months, there is no government program waiting. Five states currently offer a Self-Employment Assistance Program as a limited alternative: Delaware, Mississippi, New Hampshire, New York, and Oregon, per the U.S. Department of Labor. For everyone else, the safety net is whatever you have saved. If you have not saved enough because the math was tighter than expected, there is nothing.

There is no paid sick leave. There is no paid vacation. Every day you do not bill is a day your income is zero. Employees build unpaid time into their compensation because employers factor it into the cost of keeping them. When you freelance, you build your own paid time off by earning enough during working weeks to cover the ones when you are not. Most people do not do this consistently until they have already taken the hit of a week lost to illness or a holiday season when all the clients go quiet at once.

The misclassification exception is worth knowing. If a company controls not just the result of your work but how you do it, directs your schedule, provides your tools, and treats you functionally like an employee while calling you a contractor, you may legally be an employee regardless of what the contract says. The IRS has a process called Form SS-8 that asks the agency to determine your worker classification. Some workers who pursued this route have been awarded unemployment benefits and back protections they did not know they were entitled to. It is not a fast process and it carries the real risk of ending the client relationship. But if the situation fits, the option exists.

Retirement Is Entirely Your Problem

An employee with a 401(k) match is receiving compensation they rarely fully account for. If the company matches 4 percent of salary on a $60,000 income, that is $2,400 a year going into an account every pay period, compounding for decades, paid by someone else. It does not appear on the paycheck. It is easy to forget it exists. When you freelance, it stops existing.

No employer means no match. Retirement savings come entirely out of what you earn, which means they compete directly with every other cost this article describes. The tax-advantaged accounts are real and worth using. A SEP-IRA, which stands for Simplified Employee Pension Individual Retirement Account, lets you contribute up to 25 percent of your net self-employment income. A Solo 401(k) lets you defer up to $23,500 in 2025 with total contributions as high as $70,000 depending on your net income. Both knock dollars directly off your taxable income, which reduces your income tax and can reduce your self-employment tax. For higher earners, maxing one of these accounts changes the tax math in a meaningful way.

The catch is consistency. Contributing requires cash on hand, the discipline to set it aside instead of spending it, and the willingness to keep doing it through slow months when every dollar is already allocated. Most freelancers mean to fund retirement consistently. Most do not. The result is that someone who billed $90 an hour for fifteen years can end up with less in retirement than a salaried employee who earned $50 an hour for the same period, because the salaried employee had employer contributions, automatic enrollment, and no option to skip. Nobody told them to save. The system did it for them.

Income Does Not Come In Evenly and That Is a Structural Problem

The financial stress of freelancing is not only about how much you make. It is about when it arrives. A strong month followed by a dead month does not average out cleanly in real life. Your rent is due the same amount every month. Your utilities do not pause. Your insurance premium does not care that nobody paid you this week.

Volatile income creates compounding problems. Slow months draw from savings. Good months cover the tax liability that built up in the meantime. The cushion never quite rebuilds. Freelancers who have done this long enough learn to build a float, which is a pool of money large enough that monthly variation in income does not touch the monthly budget. Getting there requires either starting with significant savings or spending years earning more than you spend to build it. Neither is simple when the math is already tight. Build an Emergency Fund Living Paycheck to Paycheck covers the mechanics of building that cushion when there is nothing left at the end of the month. The same principles apply to building the freelance buffer.

Quarterly tax payments are hard to calculate accurately when income swings. A freelancer who earns $12,000 in January, nothing in February, $4,000 in March, and $9,000 in April has to make a first-quarter estimated payment based on a projected annual income they cannot possibly know yet. Underpay and there is a penalty. Overpay to be safe and cash is tied up during a month when you needed it. There is no clean answer. It requires a dedicated tax savings account that is not touched for anything else and the discipline to keep funding it when income is low and every dollar feels needed.

The Deductions That Help and the Ones That Do Not Help As Much As You Think

The deduction conversation is where freelancing promoters do their most effective damage. Write off your home office. Write off your laptop. Write off your internet. The subtext is that the tax code will make everything affordable. That is not how deductions work.

A deduction reduces your taxable income, not your tax bill directly. If you deduct $1,000 in business expenses and you are in the 22 percent federal bracket, you save $220 in federal income tax. The $1,000 expense still cost you roughly $780 after the tax benefit. Deductions make things cheaper. They do not make them free.

The home office deduction is real but has specific requirements that most people overlook. The space must be used exclusively and regularly for business. A dedicated room qualifies. A corner of a shared living space does not. The simplified method gives you $5 per square foot up to 300 square feet, which is a maximum of $1,500 per year. The regular method calculates the actual percentage of your home’s total expenses that correspond to the business space, which can be larger but requires more documentation and calculation. If you qualify, take it. If you are stretching the definition of exclusive use to make it fit, the risk is not worth the deduction.

The self-employed health insurance deduction is one of the most impactful available. If you are self-employed and not eligible for coverage through a spouse’s employer plan, you deduct the full cost of your premiums directly from gross income with no itemizing required. It is a straight reduction to your taxable income, and most freelancers underuse it or do not know it exists at all.

The Qualified Business Income deduction can move the number for freelancers at certain income levels. It allows eligible self-employed workers to deduct up to 20 percent of their net freelance profit from their taxable income. Think of it as the government saying: you are running a business, so you get to exclude a fifth of what that business earns before we calculate your income tax. For 2025, single filers with total taxable income at or below $197,300 are more likely to receive the full benefit. Above that level it phases out and the calculation gets complicated depending on your type of work. If your income is in that range, this deduction is worth understanding in detail with a tax professional who works regularly with self-employed clients.

Retirement contributions are the deduction with the most leverage because they serve two purposes at once. Every dollar contributed to a SEP-IRA or Solo 401(k) comes directly off taxable income, reducing both income tax and potentially self-employment tax. It also builds the retirement savings that freelancing forgot to mention you would need to fund entirely yourself. This is one of the rare cases where the financially responsible thing and the tax-reducing thing are the same action.

One thing the tax conversation often skips: deductions only help you if you are actually profitable. In a slow year with low net income, a home office deduction does not generate a refund. It reduces taxable income that may already be low. Understanding the difference between reducing a tax bill and generating a credit is part of not being misled by the deductions pitch.

Platform Fees: The Cut Before the Cut

If you find clients through Upwork, Fiverr, or similar marketplaces, you are paying for that access out of your earnings before anything else is calculated.

Upwork changed its fee structure in May 2025. The old tiered system, which charged 20 percent on your first $500 with a client, 10 percent up to $10,000, and 5 percent above that, is gone. In its place is a variable fee ranging from 0 to 15 percent per contract, determined by their algorithm based on supply and demand. The exact rate is shown before you accept a contract and is locked for its duration. Most freelancers report paying around 10 percent in practice, but the rate can vary by contract and cannot be predicted until it appears. That makes rate-setting harder because you are bidding against a cost you cannot always calculate in advance.

Fiverr charges 20 percent on every transaction. Flat. No adjustment based on relationship history or volume.

These fees are deductible as business expenses, which reduces your taxable income. They are not refunded. A freelancer billing $60,000 through Upwork at 10 percent is paying $6,000 in platform fees before taxes are calculated. Through Fiverr, $12,000. That money is gone before the self-employment tax calculation starts.

Upwork also uses a system called Connects, which are credits you spend to submit proposals to job listings. Credits cost money. If you submit ten proposals and land one client, you paid proposal costs for all ten. The winning project carries that overhead. Across a month of active prospecting, the Connects expense is real even when each individual charge is small.

Many experienced freelancers use platforms to find initial clients and then work to transition those relationships to direct arrangements over time, where they keep the full rate. Platforms often have contract terms restricting or prohibiting this for a defined period after the initial hire. Understanding those terms before pursuing that path matters. The point is this: platforms charge you to find clients, and that cost never stops. They are not a neutral marketplace where you show up and keep your full rate.

Scope Creep Is a Pay Cut You Give Yourself

You agree to a project. The scope is clear. The price is set. Then the client asks for something that was not in the original agreement. You do it because the relationship feels fragile and the money feels at risk. Then they ask for more. Six weeks later you divide your total pay by your actual hours and realize you worked for considerably less than your stated rate.

This is scope creep, and it is one of the most consistent ways freelancers reduce their own income without noticing it happening in real time. The problem is structural. Once the price is agreed and the work has started, every incentive to contain the scope sits on your side of the table. The client has no financial reason to think carefully about whether a request is extra work. From their position, they paid for a result and they are asking for help reaching it. You are the one who knows where the agreed boundary is, and you are the one who decides whether to enforce it.

A written contract with a defined scope, a specified number of revision rounds, and explicit language stating that work outside the scope will be billed separately is the standard protection. A change order process formalizes it further: any out-of-scope request gets a written estimate and written approval before the work begins. Most clients who are not trying to take advantage of you will accept this because it is how professional service relationships work at every level. The discomfort of enforcing it is real and fades with experience. The cost of not enforcing it accumulates quietly for as long as you avoid the conversation.

The Upside Is Real Too: What the Math Looks Like When It Works

Every cost and every trap here is real. But so is the other side of the calculation, and leaving it out would be the same selective math the freelancing pitch uses.

Freelancing is the only working arrangement where raising your income does not require asking anyone’s permission. You raise your rate, you find clients who will pay it, and your income goes up. No annual review cycle. No salary band. No waiting for a manager to decide your effort is worth more. For people with in-demand skills, that ceiling removal is real. The income potential above what comparable employment would pay is also real, and for some people it is substantial.

The deductions, while not magic, are more extensive than what a salaried employee can access. An employee cannot deduct their home office, their professional development, their equipment, or their health insurance premiums off the top of their income. Freelancers can. Those deductions reduce the tax gap. Not to zero. But meaningfully.

The flexibility has economic value that does not show up in any income comparison. The ability to work from anywhere, choose clients, drop a relationship that is not working, and build something that belongs to you is worth something real. How much it is worth varies by person. Only you can weigh it against the trade-offs this article describes.

Research from Upwork found that 60 percent of freelancers who left traditional employment report earning more than they did in their previous salaried positions. That number refers to gross income. This article shows what happens between gross income and take-home. The freelancers who do well financially are the ones who ran the full math first, set rates high enough to clear every cost, and treated it as a business rather than a billing arrangement. The ones who struggle are the ones who went in on the pitch without the numbers. Both outcomes are common. Neither is inevitable.

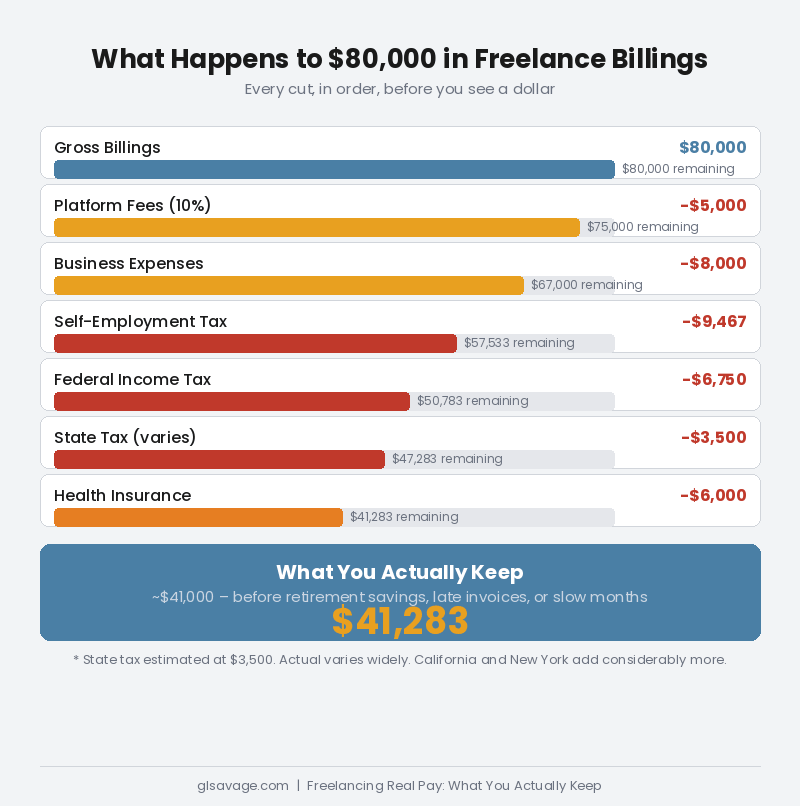

The Real Number: What $80,000 in Billings Actually Pays

Here is what freelancing real pay looks like when every cost is in the calculation. Take a freelancer billing $80,000 in a year through a mix of direct clients and a platform charging 10 percent on the platform-sourced work. That billing number sounds like financial stability. Here is what happens to it.

Platform fees on the portion billed through the marketplace: roughly $5,000, assuming half the work runs through the platform at 10 percent. Remaining gross: $75,000.

Legitimate business expenses including software, equipment, professional development, and a home office deduction: $8,000. Taxable net business income: $67,000.

Self-employment tax on 92.35 percent of $67,000: approximately $9,467. The 92.35 percent figure exists because the IRS does not tax your full net income at 15.3 percent. It first subtracts the employer-equivalent half of the tax, which gives you a slightly smaller base. On $67,000, that base is about $61,875. The deductible half of the self-employment tax, about $4,734, reduces adjusted gross income to roughly $62,266 before the standard deduction.

Federal income tax for a single filer after the 2026 standard deduction of approximately $15,000 leaves taxable income around $47,266. Federal income tax on that amount runs roughly $6,000 to $7,500 depending on exact brackets.

Total federal taxes: approximately $15,500 to $17,000. That is federal only. State income tax adds more depending on where you live. In California, New York, or Illinois, add several thousand dollars on top of that number. Remaining after federal taxes and platform fees, before state tax: roughly $53,000 to $55,000.

Health insurance on the individual market for a single person in their 30s to 40s: $5,000 to $7,200 per year depending on age, location, and plan. After health insurance: approximately $46,000 to $50,000.

That is before retirement savings. Before the weeks lost to illness with no income coming in. Before the invoice that arrived 90 days late. Before the one that never arrived. Before the slow month where you billed $2,000 instead of your normal $6,500.

A salaried employee earning $62,000 with employer-sponsored health insurance and a 4 percent retirement match is receiving total compensation worth roughly $70,000 to $75,000 when the full benefit package is counted. The freelancer billing $80,000 gross may net less real purchasing power when everything is in the calculation.

That does not make freelancing a bad deal. For many people it is exactly the right deal, and for some it pays considerably more than comparable employment once rates and client relationships are established. Understanding freelancing real pay at each stage, not just gross billings, is what tells you where you actually stand. The rate you need to charge to come out ahead of a salaried position is higher than most people calculate when they start. The break-even is above the salary number. How far above depends on your health situation, your state, your platform mix, and how efficiently you bill your time. Most people do not run those numbers until after they have already made the leap.

What To Do With This Information

If you are thinking about going freelance, calculate your total current compensation first. Salary plus the market value of your health insurance plus any retirement match plus the dollar value of paid time off. That full number, not just your salary, is what freelancing needs to beat at minimum. Then calculate the rate you would need to charge, assuming you can realistically bill about 65 percent of the hours you actually work, to net that number after self-employment tax and health insurance costs. Whatever you come up with is your floor. Not your starting rate. Your floor. Go below it and you are earning less for more uncertainty than you had in a job.

If you are already freelancing and the math has been uncomfortable, the single most effective immediate step is a dedicated savings account for taxes and moving a fixed percentage of every payment into it the day it arrives. Thirty percent is a starting point. Higher if you are in a high-income or high-tax state. Make your quarterly payments from it on schedule. Do not touch it for anything else. This one habit prevents the worst version of the tax surprise that ends freelance careers before they find their footing.

Build contracts before you need them. Scope of work, deposit requirement, payment due date, late fee clause. These are not aggressive demands. They are standard terms in any professional services relationship. A client who refuses standard written contract terms before work begins is showing you something you need to know before you start, not after.

Treat health insurance as a fixed non-negotiable expense, the same category as rent. The months you let it lapse to manage a cash shortfall are the months you are one medical event away from a financial crisis that makes the cash shortfall look minor. If you also qualify for tax credits or benefits based on your income, make sure you are collecting what is available. The Government Set Aside Thousands of Dollars for You. One in Five People Who Qualify Never Collect It. covers the credits and programs that lower-income and moderate-income households routinely miss.

Freelancing real pay is a real number. It is just not the number on the pitch. The people promoting freelancing are not lying about what is possible. They are telling the story from before the costs land. This is the version from after. Run your numbers before you decide, not after.

Frequently Asked Questions

A freelancer billing $80,000 per year can expect to pay roughly $15,000 to $17,000 in combined self-employment and federal income tax before state taxes, health insurance, and platform fees. After all of those costs, take-home in the $45,000 to $50,000 range is realistic for many freelancers depending on age, state, and expenses. The gap between gross billings and actual take-home is almost always larger than people expect going in.

The self-employment tax rate is 15.3 percent, made up of 12.4 percent for Social Security and 2.9 percent for Medicare. It applies to 92.35 percent of your net self-employment earnings after business deductions. The Social Security portion applies only to the first $184,500 in net earnings in 2026. Medicare applies to all earnings with no cap. An additional 0.9 percent Medicare tax applies above $200,000 for single filers. This tax is owed on top of regular federal and state income tax, not instead of it.

Yes, in most cases. An employee pays 7.65 percent in Social Security and Medicare taxes and their employer pays the other 7.65 percent. A freelancer pays the full 15.3 percent themselves. The IRS allows freelancers to deduct half of the self-employment tax from their adjusted gross income, which partially closes the gap but does not eliminate it. State income taxes add further depending on where you live.

In most states, no. Unemployment insurance is funded by employer contributions and is only available to employees. Self-employed workers are not part of that system. Five states currently offer a Self-Employment Assistance Program as a limited alternative: Delaware, Mississippi, New Hampshire, New York, and Oregon, according to the U.S. Department of Labor. If you believe you were misclassified as a contractor when you should legally have been an employee, you can apply for unemployment and the state will make its own determination on your classification based on how the work relationship actually functioned.

On the individual market, a single person in their 30s can expect to pay $400 to $600 per month depending on location, plan, and any income-based subsidies available through the ACA marketplace. Costs rise significantly with age. The enhanced premium tax credits that reduced costs for many freelancers from 2021 through 2025 expired January 1, 2026, causing out-of-pocket premiums to increase sharply for people above certain income thresholds. A House-passed extension is pending in the Senate as of this writing. Check the KFF ACA subsidy calculator for a current estimate based on your income and location. If you are self-employed and not covered through a spouse’s employer plan, your health insurance premiums are generally deductible from your gross income without itemizing.

Remote’s Contractor Management Report 2025 found that 85 percent of freelancers experience late invoice payments at least some of the time, and more than one in five are paid late or not at all more than half the time. A third of freelancers report completing work and never receiving payment. A written contract with a deposit requirement, a clear payment due date, and a late fee clause established before work begins is the standard protection. New York State’s statewide Freelance Isn’t Free Act, expanded in 2024, requires written contracts and timely payment for work valued at $800 or more.

Since May 2025, Upwork charges a variable service fee ranging from 0 to 15 percent per contract based on supply and demand factors. Most freelancers report an effective rate around 10 percent. The exact fee is shown before you accept a contract and is locked for the duration. Upwork also uses a Connects credit system for submitting proposals, where credits cost money whether or not you win the job. Fiverr charges a flat 20 percent on every transaction. These fees are deductible as business expenses but are not refunded, and they come out of earnings before any tax calculations begin.

The most impactful are the self-employed health insurance deduction, which comes off gross income without itemizing; retirement contributions to a SEP-IRA or Solo 401(k), which reduce both income tax and potentially self-employment tax while building savings no employer is funding for you; the Qualified Business Income deduction, which can reduce taxable income by up to 20 percent for eligible freelancers below certain income thresholds; and the deduction of half your self-employment tax from adjusted gross income. Equipment and home office deductions help but typically carry smaller total values. Every deduction reduces your taxable income, not your tax bill directly. A $1,000 deduction saves you a fraction of $1,000 depending on your tax bracket, not the full $1,000.

It depends entirely on your rate, your field, your health situation, your state, and whether you run the full math before you start. Research from Upwork found that 60 percent of freelancers who left traditional employment report earning more than before, measured in gross income. This article shows what happens between gross income and take-home. The freelancers who do well financially are those who charged enough to clear the full cost picture, built systems to manage the volatility, and approached it as a business rather than a billing arrangement. The ones who struggle are those who went in on the pitch without the numbers. Neither outcome is inevitable.