Not having a bank account is expensive. Not in one big obvious charge, but in a hundred small ones that never stop. A fee to access your own paycheck. A fee to pay your rent. A fee to pay your electric bill. A fee to pay your phone bill. None of them are large enough on their own to feel like an emergency, so they keep happening, month after month, while the banking system that caused most of them collects money from other people for free. The people paying this tax are almost always the people who can least afford to pay it, and the system was designed that way, not by accident, but because the gap between the banked and the unbanked is profitable for everyone except the people living in it.

How Many People Are Actually Living Without a Bank Account

The most recent FDIC survey puts the number at 4.2 percent of U.S. households, roughly 5.6 million households with no checking or savings account at any bank or credit union. That is the lowest rate since the FDIC started tracking it in 2009. It is still 5.6 million households. On top of that, around 19 million households are underbanked, meaning they have an account somewhere but still rely on check cashers, money orders, and alternative financial services to get through the month because the account they have does not actually serve their needs. Together that is closer to one in five American households navigating financial life with limited or no access to the infrastructure everyone else takes for granted. The cost of not having a bank account is not a niche problem. It is one of the most widespread financial penalties in the country.

You Pay to Access Money You Already Earned

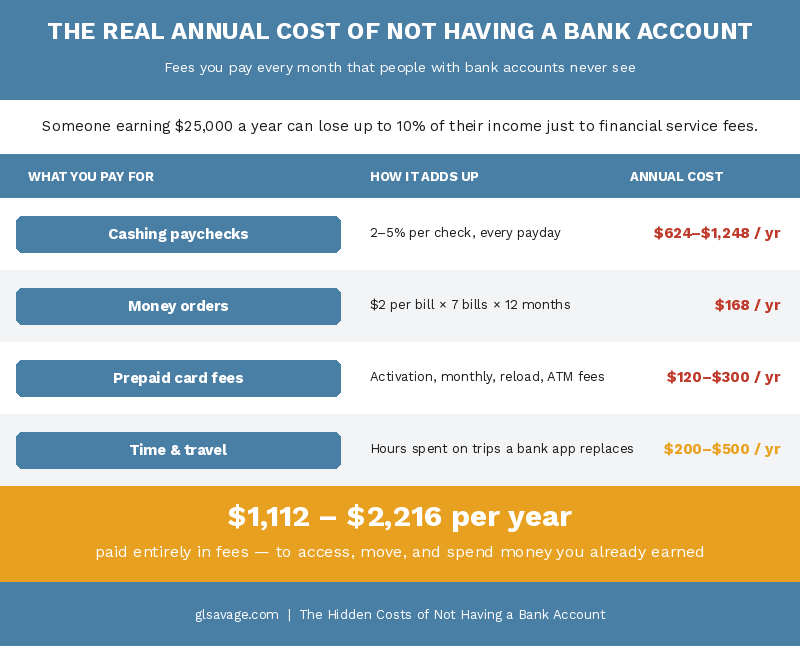

When a paycheck hits a bank account via direct deposit, the money is available immediately. You spend it, move it, or save it without paying a single fee to touch it. Without a bank account, that same paycheck has to be converted into cash first, and converting it costs money. Check-cashing services, grocery store desks, and payday lenders that double as check cashers all charge a fee for the transaction. That fee typically runs between two and five percent of the check amount. An $800 paycheck at three percent costs $24 just to access. Do that every two weeks for a year and you have paid somewhere between $600 and $1,200 just to touch money you already earned. Walmart charges $3 on checks up to $1,000, which is on the low end. Some storefront check cashers charge up to ten percent. That is not a financial mistake. That is the price of being outside the system.

Then Every Bill Payment Gets More Expensive Too

Once the paycheck becomes cash, the next layer starts. Most major bills are not designed for cash. Landlords want checks or electronic transfers. Utility companies want automatic payment or online payment. Insurance companies want the same. Without a bank account, the workaround is the money order, and money orders cost money every single time. The U.S. Postal Service charges up to $2.35 per money order. Private services charge more. Count how many bills require one: rent, electric, gas, water, phone, car insurance, renter’s insurance. Seven bills at $2 each is $14 a month, $168 a year, paid just to send money you already owe. That does not include the time spent buying them, addressing them, and mailing or delivering each one separately. Someone with a bank account pays all seven in ten minutes on a phone for free, and the bank profits from offering that convenience in ways most people never see. How Banks Make Money From Overdraft Fees and Everything Else They Are Not Telling You is worth reading alongside this one.

The Name for What Is Happening Here

Economists call this the poverty premium. It describes the pattern where people with the least financial flexibility pay the most for basic financial services, and banking is one of the clearest examples of it in American life. The Financial Health Network estimated that unbanked and underbanked Americans spend around $189 billion in fees and interest on alternative financial products in a single year. Spread across those households, that works out to roughly $3,000 per household annually going entirely to friction costs, not savings, not debt paydown, not anything that builds toward stability. Just the price of operating outside a system that was not built to include everyone. Research from the New York Federal Reserve found that unbanked households can spend as much as ten percent of their income on financial services. Someone earning $25,000 a year is handing $2,500 of it to check cashers and money order windows. Someone earning $100,000 pays virtually nothing for the same transactions. Read The Poverty Premium Explained: How to Fight Back to see how this same pattern plays out across housing, insurance, food, and credit. Banking is one piece of a much larger structure.

The Wall the Banking System Built to Keep People Out

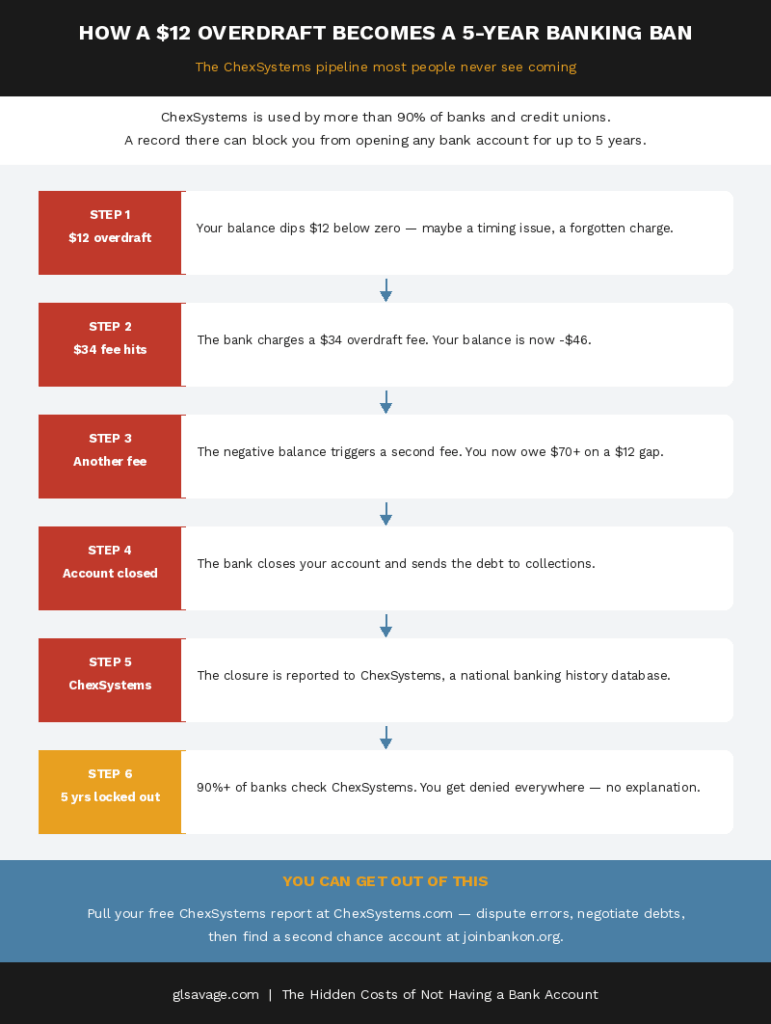

A lot of people who are unbanked are not there by preference. They are there because the banking system pushed them out and then made it hard to get back in. That wall has a name most people have never heard: ChexSystems. It is a consumer reporting agency, which means it works like a credit bureau but for bank accounts instead of loans. It collects negative banking history, and more than 90 percent of banks and credit unions check it before approving any new account application. If you have a record there, showing unpaid overdraft fees, a forced account closure, a history of bounced checks, or suspected fraud, most institutions will deny you on the spot without explanation and without telling you what to do next.

The pipeline that creates ChexSystems records is worth understanding because it starts smaller than most people expect. An overdraft of $12 generates a $34 fee. The fee pushes the balance negative. The bank charges another fee. The account gets closed. The closure gets reported to ChexSystems. The person is now flagged in a system used by more than 90 percent of financial institutions, locked out of standard banking for up to five years, over a debt that started as $12. Most people do not know this system exists until they are already in it and have no idea why every bank is turning them down.

What most people never find out: you are entitled to a free copy of your ChexSystems report every 12 months, exactly the same way you can pull a free credit report. Request it at ChexSystems.com, by calling 800-428-9623, or by mail. If there are errors on that report, you have the right to dispute them under the Fair Credit Reporting Act. ChexSystems must investigate within 30 days. Errors are more common than the system makes it seem, and an inaccurate record can block your banking access for years based on information that was never correct. Negative information stays on file for five years from the date of each incident, and multiple incidents each start their own five-year clock, which means overlapping problems can chain-lock your access longer than you would expect. If you have a legitimate debt on there, paying it off does not automatically remove the entry, but ChexSystems is required to update the record to show it was resolved. Some debts can also be negotiated for removal as part of a pay-for-delete agreement, the same concept used in credit repair.

The Door That Is Already Open

Here is what most people in this situation are never told: there is an entire category of bank account specifically designed for people with ChexSystems records, and many are available right now at major banks and credit unions. They are called second chance checking accounts, and they are more accessible than they used to be.

Chase offers Secure Banking, a second chance account with no overdraft fees and a flat $4.95 monthly fee. Wells Fargo offers Clear Access Banking at $5 a month with no overdraft fees and no minimum balance. Varo Bank offers a second chance account with no monthly fee at all. Many credit unions offer their own versions, often with lower fees and a clear path to upgrading to a standard account after six to twelve months of responsible use.

The Bank On program, run by the Cities for Financial Empowerment Fund, has established national standards for safe, low-cost checking accounts. As of 2023, more than 400 financial institutions offering Bank On-certified accounts operate at over 45,000 branches, and 97 percent of low-to-moderate income households live near a branch that carries one. Bank On-certified accounts have monthly fees capped at $5, no overdraft fees, and no minimum balance requirements. They do not all use ChexSystems in the traditional way. You can find participating institutions at joinbankon.org. If you have been denied a standard account and did not know these options existed, you have been navigating a system that assumed you would give up. If you apply for a second chance account and still get denied, ask to speak with the branch manager. Managers at many institutions have discretion to approve accounts that the automated system rejected. Most people never ask.

The 54 Percent Nobody Talks About

The FDIC’s own data shows that about 54 percent of unbanked households say they are not interested in opening a bank account at all. That number is worth sitting with for a moment because it tends to get used as evidence that the unbanked are fine where they are. That reading is wrong. The people in that 54 percent are not mostly people who evaluated the banking system and preferred operating outside it. They are mostly people who tried the banking system, got burned by it, absorbed real financial damage from overdraft fees and account closures, and decided the risk of going back was not worth it. That is a rational response to a bad experience, not indifference to the costs of being unbanked. The banking system created the distrust and then points to the distrust as evidence that the people it excluded do not want to be included. The second chance account options and Bank On-certified accounts above exist specifically to address the overdraft and fee concerns that drove most of those people out in the first place.

The Risk of Living Entirely in Cash

Operating in cash creates a category of risk that people inside the banking system almost never think about. Cash can disappear without recourse. A lost wallet, a theft, a fire, cash kept at home because there is nowhere else to put it. When money lives in a bank account it has fraud protection, FDIC insurance up to $250,000, and a transaction record that can be used to dispute errors. When money lives in cash, losing it means losing it. There is no dispute process, no insurance, no recovery. This is not a character flaw in people managing money in cash. It is a structural risk that the unbanked carry and the banked do not, and it almost never gets counted in the cost comparisons.

The Credit History You Cannot Build

The modern financial system runs on documented history. Credit scores, loan approvals, apartment applications, utility deposits, and in some states even employment screenings all use recorded financial behavior as a signal. Cash transactions leave almost none of that record. Someone who pays rent in cash or money orders for years, covers every utility on time, and manages their finances responsibly may still look completely invisible when they apply for credit. The system cannot measure behavior it was not built to see. This is one of the quieter long-term costs of not having a bank account: not just the fees paid today, but the credit history that cannot be built, the rates paid when credit is eventually needed, and the deposits required because there is no documented track record. Without a credit history or a bank account, the options for emergency borrowing narrow to exactly the products built to exploit that gap. How Payday Loans Are Legal and What to Do Instead is a direct consequence of this invisible credit problem, and understanding both helps explain why the same people end up in both traps.

The Cashless Economy Is Making This Worse

The problem is accelerating. More businesses move toward card-only transactions every year. Some venues, stadiums, and restaurants in major cities no longer accept cash at all. Online purchases, app-based services, ride-sharing, and digital subscriptions all require a card or a linked bank account. Even some government benefit systems now default to electronic payment. Someone without a bank account or a prepaid card linked to one is not just paying more for the services they can access. They are being locked out of transactions that everyone else treats as routine. The gap between what is available to the banked and what is available to the unbanked grows wider every year, and the system generates almost no friction when it does.

Why People End Up Here

The story that unbanked people simply prefer cash or distrust banks is incomplete and convenient for the institutions that benefit from the status quo. The FDIC’s own data shows that the top reason people give for not having a bank account is that they do not have enough money to meet minimum balance requirements. Around 42 percent of unbanked households cite this as their primary barrier. A third cite high fees. Research from the Philadelphia Federal Reserve found that a household experiencing job loss is about 18 percentage points more likely to become unbanked, which tells you exactly how people end up here. It is not a preference. It is usually a consequence of something that happened to them, and then the banking system makes it structurally difficult to recover. The FDIC data also shows that 11 percent of Black households and 9 percent of Hispanic households are unbanked, compared to 2 percent of white households. That gap is not explained by preference either. It is explained by the same pattern that shows up everywhere in the poverty premium: the people with the fewest alternatives pay the most to operate inside a system that was not built with them in mind.

What to Do If You Are Currently Unbanked

Start by pulling your free ChexSystems report at ChexSystems.com. Find out exactly what is on it. Errors are common and disputable. Legitimate debts may be negotiable or removable through a pay-for-delete arrangement. Knowing precisely what the barrier is gives you something to work with instead of a rejection with no explanation. This is step one in figuring out how to get a bank account with bad history: you cannot fix what you cannot see.

Then look specifically for Bank On-certified accounts at banks or credit unions near you using the directory at joinbankon.org. These accounts were built for this situation: monthly fees capped at $5, no overdraft fees, no minimum balance, and a path to a standard account after six to twelve months of good standing. If the major banks near you are not an option, credit unions often have more flexibility and lower barriers. Many offer second chance checking with a clear upgrade timeline.

If you are using prepaid cards in the meantime, read the fee structure before loading money onto one. Activation fees, monthly maintenance fees, reload fees, ATM withdrawal fees, and inactivity fees can stack up to nearly as much as a bank account annually. Some prepaid cards are genuinely low cost. Others are not. Compare the full annual cost of any prepaid card directly against a Bank On-certified account before committing to it.

If you apply somewhere and get denied, ask to speak to the branch manager directly. Ask specifically whether they have a second chance account or any account designed for people rebuilding their banking history. Many institutions do. Almost no one asks.

Not Having a Bank Account Is Expensive. The System Designed It That Way.

The cost of not having a bank account is not a personal failing. It is a structural feature of how the banking system was built. Check cashers, money order windows, prepaid card issuers, and payday lenders all exist in the gap between the people the banking system wants to serve and the people it does not. That gap is profitable. It is funded entirely by the people who can least afford to fund it. The second chance accounts, Bank On-certified accounts, ChexSystems dispute rights, and credit union options above are all real. Most people who need them have never been told they exist. Now you have been.

Frequently Asked Questions About Not Having a Bank Account

How much does it cost per year to not have a bank account?

The numbers add up faster than most people expect. Check cashing fees at two to five percent per paycheck, money order fees of one to three dollars per bill payment, and prepaid card fees for everyday spending can combine to several hundred to over a thousand dollars a year depending on income and how many bills require payment. The Financial Health Network estimated that unbanked and underbanked Americans collectively spend around $189 billion annually on fees and interest for alternative financial services, roughly $3,000 per household.

What is ChexSystems and why does it matter for opening a bank account?

ChexSystems is a consumer reporting agency used by more than 90 percent of banks and credit unions to screen new account applicants. It tracks negative banking history: unpaid overdraft fees, forced account closures, bounced checks, and suspected fraud. A record there can get you denied at bank after bank without any explanation of why. Negative information stays on file for five years from the date of each incident. You are entitled to a free report every 12 months at ChexSystems.com and have the right to dispute errors under the Fair Credit Reporting Act.

Can you open a bank account if you have been reported to ChexSystems?

Yes. Second chance checking accounts are specifically designed for people with ChexSystems records. Chase Secure Banking, Wells Fargo Clear Access Banking, and Varo Bank all offer them with low or no monthly fees and no overdraft fees. Bank On-certified accounts, available at more than 400 financial institutions across the country, are another option with capped fees and accessible approval standards. Most of these accounts offer a clear path to upgrading to a standard account after six to twelve months of responsible use.

What is a Bank On account and how do you find one?

Bank On is a national program run by the Cities for Financial Empowerment Fund that certifies checking accounts meeting standards for safety, low cost, and accessibility. Bank On-certified accounts have monthly fees capped at $5, no overdraft fees, no minimum balance requirements, and are designed to be accessible to people who have been turned down for standard accounts. As of 2023, these accounts are available at more than 45,000 bank branches across the country. Find participating institutions at joinbankon.org.

Why do so many unbanked people say they don’t want a bank account?

About 54 percent of unbanked households report they are not interested in opening an account, according to the FDIC. That number is widely misread as indifference. Most of the people in it tried the banking system, experienced overdraft fees, account closures, or ChexSystems denials, and concluded the risk was not worth it. That is a rational response to a bad experience. Second chance accounts and Bank On-certified accounts eliminate overdraft fees specifically to address the concern that drove most people to that conclusion.

How do you dispute an error on your ChexSystems report?

Request your free report at ChexSystems.com, by phone at 800-428-9623, or by mail. Review it for inaccuracies: wrong amounts, accounts you do not recognize, or entries that should have aged off after five years. Submit a dispute through ChexSystems online, by mail, or by fax. Include documentation: bank statements, payment receipts, or correspondence. ChexSystems must investigate within 30 days under the Fair Credit Reporting Act and correct confirmed errors. Keep copies of everything and use certified mail if disputing by post.

Are prepaid debit cards a good substitute for a bank account?

They solve some problems and create others. Prepaid cards allow electronic payments and online purchases without a bank account, which is useful. But many carry activation fees, monthly maintenance fees, reload fees, and ATM withdrawal fees that add up to nearly as much as a bank account annually. Some prepaid cards are genuinely low cost or free with direct deposit. Others are not. Read the full fee schedule before loading money onto any prepaid card and compare the annual total directly against the cost of a Bank On-certified account or a second chance checking account.

Does not having a bank account hurt your credit score?

Not directly. Bank accounts are not reported to credit bureaus and do not appear on credit reports. But the indirect effect is significant. Without a bank account it is much harder to get a credit card, build a payment history, or qualify for loans. Cash and money order payments leave no record with credit bureaus regardless of how reliably you pay. You can manage finances responsibly for years and still appear invisible to the credit system because the system was not built to see those transactions.

What is the fastest way to get a bank account after being denied?

Pull your ChexSystems report first at ChexSystems.com to understand exactly what the barrier is. Then look for Bank On-certified accounts at joinbankon.org or search specifically for second chance checking at credit unions in your area. Credit unions tend to have more flexible approval criteria than large banks and are often willing to work with applicants who have a difficult banking history. If you are denied at one institution, ask the branch manager directly whether they have discretion to reconsider, and ask specifically whether they offer any account for people rebuilding their banking history. Many do. Most people never ask.