Payday loans charge up to 400 percent interest and it is completely legal. Not legal in a gray area. Not legal with exceptions. Openly, plainly, by design legal in 26 states. If you borrowed money from a friend at that rate you would lose the friendship. If a credit card charged that rate the company would face federal prosecution. But a payday lender can do it in a storefront on the corner, to the most financially vulnerable people in the country, and the government has known about it for decades. This is not a loophole someone accidentally fell through. It is a system that was carefully built to work exactly this way. Once you understand how it was built, you stop being the easiest person in the room to take advantage of.

How Payday Loans Stay Legal When the Math Looks Like a Crime

Laws that protect borrowers from predatory interest rates were written around mortgages, car loans, and credit cards. Those are products that run for months or years, so the rules measure interest annually. That annual measurement is the key. Payday lenders built their entire product around avoiding it. Instead of charging interest, they charge a flat fee. Instead of a loan that runs for months, the loan runs for two weeks. Borrow $300, pay a $45 fee, repay everything on your next payday. On paper that looks like a service charge, not a loan. But if you convert that $45 fee on a $300 two-week loan into an annual rate, it is 391 percent. In states with looser rules it goes above 600 percent. The fee structure fits inside the legal definition of what a short-term service fee is allowed to be. The industry lobbied for years to make sure those definitions stayed exactly where they are. The product was engineered around the law, not the other way around.

The Business Model Is Not the Loan. It Is Getting You to Roll It Over.

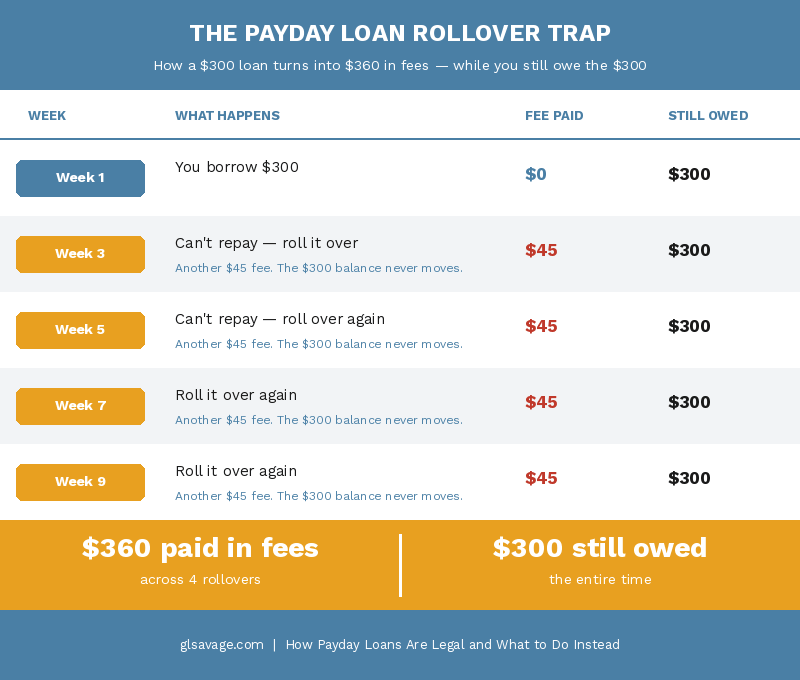

Here is what the industry absolutely does not want you to know. They do not make their money from borrowers who take one loan and pay it back. Those borrowers are almost irrelevant. The money comes from borrowers who cannot repay on time and roll the loan over, paying a new fee every two weeks while the original balance never moves.

The Consumer Financial Protection Bureau, which is the federal agency that watches over lenders, studied more than 12 million payday loans. More than 80 percent were rolled over or renewed within two weeks of the due date. Three out of five went to borrowers who took seven or more loans in a row. The average payday borrower spends five months of the year in debt and ends up paying $520 in fees on a loan that started at $375. They paid more in fees than they originally borrowed, and they still owed the original amount the entire time. The CFPB also found that lenders in some cases actively talked borrowers out of repayment options that would have ended the cycle, because ending the cycle ends the revenue.

This is not what borrowing is supposed to look like. It is a debt trap with a fee structure built to keep you in it.

What a Payday Lender Can Do to Your Bank Account Without Asking You Again

When you take out a payday loan, you sign over permission for the lender to pull money from your bank account on the due date. What almost nobody explains is that this permission does not go away when the due date passes. The lender keeps it. If the money is not there, they try anyway. If that fails, they try again. And again.

The CFPB found that after a failed withdrawal attempt, lenders try again 75 percent of the time. Most of those second and third attempts fail too. Every attempt, successful or not, can trigger a fee from your bank. A returned payment fee, a non-sufficient funds fee, an overdraft fee. Each one typically runs around $34. These hit your account at the same time the lender’s own fees hit. Half of online payday borrowers end up paying an average of $185 in bank penalty fees on top of everything they already owed the lender.

One in three of those borrowers ends up with their bank account closed involuntarily because of the overdrafts. When a bank closes your account that way, it reports the closure to a database called ChexSystems. ChexSystems works like a credit report but for bank accounts. Most banks and credit unions check it before letting anyone open a new account. A bad ChexSystems record can get you turned down at bank after bank for up to five years. You went in needing $300 for rent. You came out with no bank account, debt to both the lender and the bank, and a record that makes it harder to open a new account anywhere. What it actually costs to live without a bank account goes well beyond what most people expect, and it starts compounding immediately.

There is a new federal rule that is supposed to stop this spiral. As of March 30, 2025, the CFPB’s two-strikes rule officially took effect. Under that rule, after two failed withdrawal attempts, a payday lender cannot try again unless you specifically give them new written permission. It was a real protection, eight years in the making, that the industry fought in court all the way to the Supreme Court and lost. Here is what they do not tell you: two days before it took effect, the current administration announced it would not prioritize enforcement of the rule. The rule is technically law. The agency responsible for enforcing it has said it is not a priority. That means the protection exists on paper and may or may not be applied in practice depending on who the lender is and whether they decide to follow it anyway. Do not count on this rule protecting you. Use your own rights instead, which still apply regardless of what the CFPB enforces.

You can stop the withdrawal attempts yourself without paying off the loan first. Call your bank and tell them in writing that you are revoking the lender’s authorization to debit your account. Federal law gives you this right regardless of what the CFPB does or does not enforce. The debt does not disappear but the spiral of overlapping fees stops. Do it before the next scheduled attempt, not after. Banks almost never reverse fees that have already processed. How banks handle overdraft fees is a separate system working against you at the same time, and understanding both helps you protect what little is left in the account.

There Is a Free Way Out That Lenders Are Required to Offer and Almost Never Mention

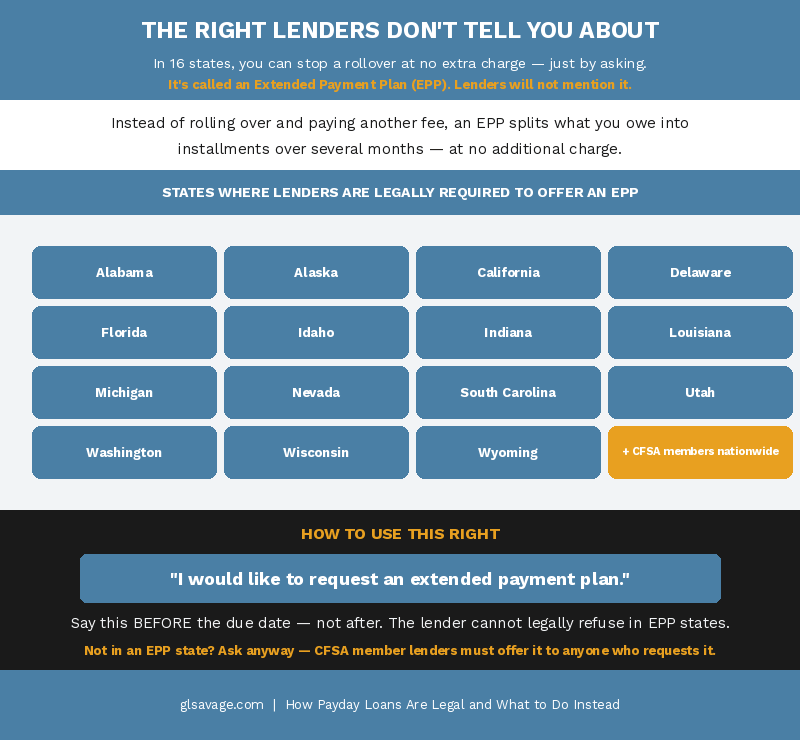

In 16 states, payday lenders are legally required to give you a way out of the rollover cycle at no extra charge. It is called an extended payment plan, sometimes shortened to EPP. Instead of rolling the loan over and paying another fee, you ask to split what you owe into smaller payments spread over several months, with no additional fees added. On a $300 loan where the rollover fee is $45 every two weeks, an extended payment plan could save you several hundred dollars depending on how long you would have stayed in the cycle.

The CFPB found that lenders routinely fail to tell borrowers this option exists. Some actively talk people out of it. In Washington State, which has the strongest extended payment plan rules in the country, only 13 percent of eligible borrowers ever use one. Not because it is hard to access. Because almost no one knows it is there.

The states that require lenders to offer extended payment plans are Alabama, Alaska, California, Delaware, Florida, Idaho, Indiana, Louisiana, Michigan, Nevada, South Carolina, Utah, Washington, Wisconsin, and Wyoming. If you are in one of those states and you cannot repay your payday loan on the due date, call the lender before the due date and say these exact words: I would like to request an extended payment plan. Not after the due date. Before. The lender cannot legally refuse. They will not bring it up on their own.

Even if your state is not on that list, ask anyway. Any lender that belongs to the Community Financial Services Association of America, which is the industry’s main trade group, is required by the group’s own rules to offer an extended payment plan to any borrower who requests one. The worst they can say is no. That costs you nothing.

A Lot of Payday Loan Websites Are Not Actually Lenders

When you search online for a payday loan and fill out an application form, there is a real chance you are not applying with a lender. Many of the top results for payday loan searches are lead generation companies. Their business is collecting your personal information and selling it. Your name, address, income, bank account details, and Social Security number go out simultaneously to multiple lenders the moment you hit submit. That is why people sometimes get flooded with calls and texts within minutes of filling out what they thought was one application. You were never the customer. You were the product being sold to whoever would pay the most for you.

The lenders who buy those leads tend to be the ones with the most aggressive collection tactics and the least transparent terms. If you are going to use a payday lender at all, go directly to a lender’s own website or walk into a physical location. Do not fill out any form on a site that claims to compare your options or find you the best rate.

Why These Stores Are Exactly Where They Are

Payday lender locations are not random. They cluster in neighborhoods with lower average incomes, fewer bank branches, and more financial instability. Research has shown consistently that payday lenders are far more concentrated in Black and Latino communities than in white communities with similar income levels. This is a deliberate business decision. The product was designed for places where cash emergencies happen frequently, alternatives are hard to access, and people are less likely to have seen the fine print explained clearly. The Center for Responsible Lending estimates that borrowers in states that allow payday lending, earning around $25,000 a year, pay more than $2.2 billion in fees annually. That money comes disproportionately from specific communities. The store locations are chosen to make sure of it. The poverty premium is the name for the broader pattern that creates these conditions, and payday lending is one of its most profitable expressions.

Why Banning Them Has Not Made Them Disappear

Around 20 states and Washington D.C. have either banned payday loans or capped interest rates at 36 percent per year, which makes the traditional payday loan model unprofitable enough that lenders stop offering it. The federal Military Lending Act puts the same 36 percent cap on loans to active-duty service members and their families no matter what state they live in. But payday lenders do not disappear when a state tightens the rules. They reorganize. Online lenders operate across state lines and argue that only the laws of the state they are chartered in apply to them, not the laws of the state where you live. Some lenders have set up operations under tribal agreements to claim they are exempt from state rate caps entirely. The two-week payday loan gets repackaged as a six-month installment loan with payments spread out but a fee structure that produces a nearly identical annual rate. The shape of the product changes. The cost tends to stay. If you are in a state that restricts payday lending and someone is offering you something that works exactly like a payday loan, ask what law governs the agreement before you sign anything.

Why People Take Them, and Why That Is Not the Real Problem

The standard explanation for why people use payday loans is that they are not thinking clearly or they do not understand the math. That explanation is wrong and it is convenient for the industry. The real reason people take payday loans is that something cannot wait and there is nothing else fast enough. Rent is due tomorrow or the landlord files. The car needs a repair today or the job disappears. A utility gets shut off before the kids get home. The payday loan is not appealing because people are impulsive. It is appealing because it is fast, it does not check your credit, and it makes a problem with a hard deadline go away today. The problem it creates two weeks later is real. It is just not today’s problem, and when you are in crisis you are solving today’s problem. The borrowers who get trapped are not people who did bad math. They are people who had no cushion, took the only available option, and could not absorb the lump-sum repayment when it came due. The alternatives below are not perfect. But some of them are faster than people expect, and all of them are cheaper than a loan designed to keep you in it.

What to Do Instead When You Need Money Now

These options are not as fast as a payday loan. That is the honest truth. But they are dramatically cheaper, and some move faster than people expect. Know them before you need them, because finding them at midnight before a due date is harder than finding them on a calm Tuesday.

Call whoever you owe before you do anything else. Utility companies, landlords, hospitals, and some government agencies have hardship arrangements that are not listed anywhere on their website. They exist and they get used, but only by people who call and ask specifically whether a hardship deferment or payment plan is available. This costs nothing. Most people never make this call because they assume the answer is no. It frequently is not. Utility assistance programs in particular go massively underused because no one tells you to look for them.

Federal credit unions offer emergency loans designed specifically as payday loan alternatives. They are called payday alternative loans, or PALs, and there are two versions. PAL I lets you borrow up to $1,000 with a repayment term of one to six months, but you need to have been a credit union member for at least one month before applying. PAL II lets you borrow up to $2,000 with a term of one to twelve months, and you can apply the day you join. Both versions cap the interest rate at 28 percent per year by federal law, and the application fee cannot exceed $20. A PAL on $300 at 28 percent costs a few dollars. A payday loan on $300 at 391 percent costs you the original $300 again in fees before you are out. If you are not already a credit union member, many have free or very low-cost membership. Find one near you at ncua.gov. PAL II in particular is worth knowing about because the day-one eligibility removes the main barrier people assume exists.

Cash advance apps are genuinely better than payday loans but they are not free, and the way the costs are presented is worth understanding before you download anything. Apps like Dave, EarnIn, and Brigit let you advance a small amount against your next paycheck, usually $100 to $500, with no interest. That part is true. What they do not put in the headline is that most of them charge a fee for instant delivery, anywhere from $1.99 to $13.99 depending on the amount, and most of them push you to leave a tip on every transaction. On a $100 advance where you pay a $4 instant fee and tip $2, you have paid $6 to borrow $100 for two weeks. That is not 400 percent, but it is not free either. Dave also requires you to open a Dave checking account to get the largest advance amounts. EarnIn requires employer verification and sometimes GPS location access to confirm you are actually going to work. Brigit charges a monthly membership fee. These are all better options than a payday loan. Just read the actual terms before you decide which one works for you.

Ask your employer directly. Some workplaces offer paycheck advances or have early wage access programs. A direct advance from your employer with no fees attached is the best version of this option. It exists more often than people realize and almost no one asks.

Call 211. This is a free national helpline that connects people to local emergency assistance programs including rent help, utility assistance, food, and sometimes direct financial aid. It runs 24 hours a day. You can also search online at 211.org. If you are staring at a bill with a shutoff date and considering a payday loan, call this number first. Most people have never heard of it. That is exactly why it is underused.

If You Are Already in the Cycle Right Now, Do These Things in Order

First, call the lender before the next due date and say you want an extended payment plan. Those exact words. If you are in one of the 16 states listed above, they cannot legally say no. Even outside those states, ask anyway. Getting one rollover stopped saves you a fee immediately and stops the spiral from getting worse.

Second, if the lender refuses or you have already missed the due date, contact your bank today and revoke the lender’s authorization to withdraw from your account. Put it in writing. This stops the bank fee spiral while you work out the rest, and you have the federal right to do it regardless of what the lender says.

Third, contact the National Foundation for Credit Counseling at nfcc.org. They are a nonprofit. The conversation costs nothing. They can negotiate with payday lenders on your behalf, help consolidate the debt into a manageable payment plan, and tell you specifically what options exist under your state’s laws.

Fourth, if the balance has grown to where repayment feels impossible, contact a legal aid organization in your area. Legal aid is free. They can tell you whether the debt can be negotiated, settled, or in some cases discharged. If your bank account was closed as a result of the overdraft spiral, a legal aid attorney can advise you on disputing the ChexSystems record so you can open a new account. Find legal aid in your area at lawhelp.org. The negotiation principles that apply to payday loan debt are similar to what works with other kinds of debt, and understanding them gives you a clearer picture of what is actually possible.

The cycle feels permanent when you are in it. It is not.

This Is a System. Not a Personal Failing.

Everything about how payday loans work was designed on purpose. The fee structure that sidesteps interest rate laws. The two-week term that makes repayment nearly impossible for anyone living paycheck to paycheck. The bank account access that lets lenders keep pulling even after the account runs empty. The location strategy that targets communities with the fewest alternatives. The lead generation websites that sell your Social Security number to the most aggressive lenders in the market. The extended payment plans that legally exist but that lenders will not tell you about. The federal rule that is technically in effect but that the agency responsible for it has said is not a current priority. None of this happened by accident. It was built to be profitable, and it is most profitable when people stay in it the longest.

The average payday borrower is not someone who made a careless decision. They are someone who was handed a product engineered to be hard to escape, with information deliberately withheld that would have changed what they signed.

Now you have that information. Use it.

Frequently Asked Questions About Payday Loans

How is a payday loan legal when it charges 400 percent interest?

Payday lenders charge flat fees instead of annual interest and structure loans as two-week advances rather than standard loans. The laws that protect borrowers from predatory interest rates were written for longer products like mortgages and credit cards and measure costs annually. Payday loan fees were deliberately designed to fit inside the legal definition of a short-term service charge rather than loan interest. The result is an effective annual rate of 300 to 400 percent or higher that is technically legal in the 26 states that permit payday lending.

What happens if you don’t pay a payday loan back on time?

The lender will attempt to withdraw the full balance from your bank account on the due date. If the money is not there, the withdrawal fails, your bank charges a fee, and the lender typically tries again. Multiple failed attempts trigger fees from both the lender and the bank at the same time. Under a federal rule that took effect March 30, 2025, lenders are supposed to stop after two failed attempts unless you give new written permission. The agency responsible for enforcing that rule has said it is not currently a priority. The lender may then roll the loan over for another fee or send the debt to collections. In states that require it, you can request an extended payment plan before the due date at no extra charge.

Can a payday lender take money from your bank account without permission?

When you take out a payday loan, you give the lender permission to debit your account as part of the loan agreement. That permission does not expire on the due date. The lender keeps it and can keep trying even after failed attempts. You can revoke it at any time by contacting your bank in writing and instructing them to block the lender’s withdrawals. Federal law gives you this right. The debt still exists but the automatic withdrawals stop. Do it before the next scheduled attempt, not after the fees have hit.

What is an extended payment plan for a payday loan?

An extended payment plan, or EPP, lets you split your payday loan balance into smaller installments paid over several months instead of one lump sum, usually at no added charge. Sixteen states require payday lenders to offer them. Ask for it by name, using the words “extended payment plan,” before your due date. Lenders will not mention it on their own. In states where EPPs are required by law, the lender cannot refuse your request.

What states have banned payday loans?

Around 20 states and Washington D.C. have either banned payday loans outright or capped interest rates at 36 percent per year, which makes the standard payday loan model unworkable. The remaining states permit payday lending under varying levels of regulation. Active-duty military members and their families are protected by a federal 36 percent rate cap regardless of which state they live in.

Are cash advance apps like Dave and EarnIn better than payday loans?

Yes, meaningfully so. Cash advance apps typically charge a fraction of what payday loans cost. The catch is that the costs are presented in ways that make them look free when they are not entirely free. Most apps charge a fee for instant delivery, ranging from around $2 to $14 depending on the advance amount. Most also prompt you for a tip on every transaction. On small advances these fees add up to significant annual rates, though still well below the 391 percent a traditional payday loan charges. Dave requires you to open a Dave checking account for the largest advance amounts. EarnIn requires employer verification. Brigit charges a monthly subscription. Read the specific terms for whatever app you are considering before linking your bank account.

What is the difference between a payday loan and a payday installment loan?

A payday loan is repaid in one lump sum, usually in two weeks. A payday installment loan is repaid in multiple smaller payments over a longer period. Some lenders repackaged their products as installment loans when states began restricting single-payment payday loans. The spread-out payments feel more manageable but the annual interest rates on many payday-style installment loans remain extremely high. Paying less per installment over more months does not necessarily mean you pay less in total. Always convert the fees to an annual rate to make a fair comparison.

Can you negotiate a payday loan you cannot pay back?

Yes. Contact the lender directly and ask for a settlement or repayment plan. Lenders would often rather negotiate than pay the cost of sending debt to collections. Starting a settlement offer at 40 to 60 percent of the balance owed is a commonly cited starting point. Get any agreement in writing before paying anything. Nonprofit credit counselors at nfcc.org can negotiate on your behalf at no cost to you.

What happens to your credit and bank account if you default on a payday loan?

Payday lenders do not typically report to the major credit bureaus, so a default may not hurt your credit score directly. But if the lender’s repeated withdrawal attempts cause your bank to close your account involuntarily, that closure gets reported to ChexSystems. ChexSystems is a database banks check before opening new accounts. A negative record can prevent you from opening a standard checking account for up to five years. If the debt goes to a collection agency, that agency may report it to the credit bureaus, which does affect your credit score.

What is the fastest way out of a payday loan cycle?

Call the lender before your next due date and request an extended payment plan. This stops the rollover fee cycle at no additional cost if you are in a state that requires lenders to offer one. At the same time, contact your bank in writing and revoke the lender’s authorization to withdraw from your account. That stops the bank fee spiral while you work out the rest. Then contact the National Foundation for Credit Counseling at nfcc.org. They can negotiate with the lender on your behalf and build a repayment plan, often at reduced or zero additional cost.