Most people pay whatever the pharmacy shows them. They hand over their insurance card, see the number, and pay it. What they do not know is that the price on that screen is often not the lowest available price for that drug. Manufacturers run savings programs that most patients never find. Discount tools regularly beat insurance copays. Patient assistance programs exist specifically to get people medications they cannot afford. Take Synthroid, a common thyroid medication. AbbVie, the company that makes it, runs a savings program for patients that brings the monthly cost well below what most people pay at the counter. It is on their website. It has always been there. Most people on Synthroid have never heard of it and keep paying full price every single month. The price at the counter is where most people stop. It does not have to be where you stop. Here is every option available to you and how to get prescription drugs cheaper.

Why Your Copay Is Sometimes Higher Than the Cash Price

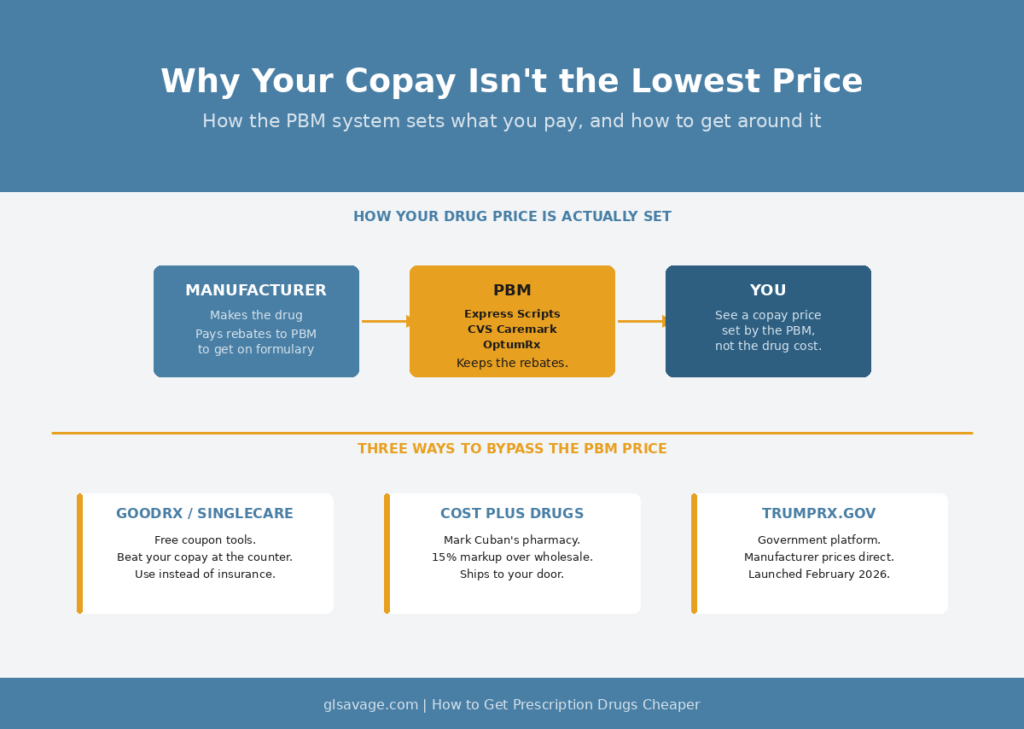

When you hand over your insurance card, your cost is not based on what the drug costs to make. It is based on a deal set by a company most people have never heard of called a pharmacy benefit manager, or PBM. Three companies control the majority of the U.S. PBM market: Express Scripts, CVS Caremark, and OptumRx. They sit between drug manufacturers, insurance companies, and pharmacies. They negotiate deals with manufacturers, collect payments called rebates, keep a cut of those payments, and set what shows up as your copay.

The result is that your copay is sometimes higher than the straight cash price of that same drug. One Texas pharmacist described selling Simvastatin, a common cholesterol medication, for $19 cash while his customers with insurance paid $42 because their plan had a fixed copay set at that number. The extra money did not go to the pharmacy. It went back to the PBM in what is called a clawback. For years, pharmacists were under contract rules that prevented them from telling you the cash price was lower. Federal legislation passed in 2020 removed those restrictions. The gap still exists. You just have to ask now.

A University of Toledo study of 20 commonly prescribed generics found that about 40 percent were cheaper through a discount tool like GoodRx than through insurance. That is not rare. It is common enough that checking before every fill is worth the two minutes it takes.

Your Doctor Probably Does Not Know What Your Drug Costs

This part most articles skip entirely. Your doctor writes prescriptions all day. They learned drug names in medical school, and pharmaceutical sales reps come to their offices regularly, bring food, and market their specific brand by name. That is part of why your doctor writes “Synthroid” instead of “levothyroxine.” Not because the brand is medically necessary. Because that is the name in their head. The brand version and the generic have the same active ingredient. The generic typically costs a fraction of the price.

Ask your doctor directly: is there a generic for this? If a generic exists, is there any medical reason I need the brand? Most of the time the answer is no. One question at the appointment can cut your monthly cost by 80 percent or more.

There is also a line on your prescription that most people have never noticed. A doctor can write “dispense as written,” which tells the pharmacy to give you exactly the drug written, brand name only. If that line is not on your prescription, the pharmacist can substitute a generic. If it is on there and you want the generic, ask your doctor to remove it. They often do not realize it is there or why it matters to your cost.

Prescription Discount Tools: GoodRx, SingleCare, and Cost Plus Drugs

GoodRx, SingleCare, and Cost Plus Drugs let you look up your medication, see a price, and pay that price at the counter instead of running it through your insurance. They work through a completely different pricing channel than your PBM. The price is often lower than your copay, sometimes by a lot.

Using them takes two minutes. Go to GoodRx.com, type in your drug name, and compare the price to your copay. Tell the pharmacist which one to run. You can use insurance one month and GoodRx the next. There is no membership and no commitment for the basic version. Prices sometimes differ between GoodRx, SingleCare, and Cost Plus Drugs, so on an expensive medication it is worth checking all three.

TrumpRx.gov launched in February 2026 as a government-run platform where manufacturers list direct-to-patient prices. You look up your drug, get a coupon from the manufacturer, and bring it to the pharmacy or use a mail delivery option the manufacturer sets up. Prices vary by drug and manufacturer. It is worth checking alongside GoodRx and SingleCare because some manufacturers offer deeper discounts through TrumpRx than through other channels.

Mark Cuban’s Cost Plus Drugs is built on a different model. It is an online pharmacy that publishes exactly what it pays for each medication, adds a 15 percent markup, and charges a $5 pharmacy fee. You need a prescription sent directly to them and the drug ships to your door. For certain generics the savings are hard to believe. A cancer medication called imatinib runs around $2,500 per month at a standard pharmacy. Cost Plus Drugs lists it at $13.40. It covers over 2,000 generics. It does not cover most brand-name drugs.

The catch on all discount tools: when you pay through GoodRx or Cost Plus Drugs instead of your insurance card, that purchase typically does not count toward your deductible or out-of-pocket maximum. Whether that matters depends entirely on your own situation. If your deductible is $4,000 and you have only paid $300 toward it this year, you are unlikely to hit that number anyway. The money you save on this fill is real. Take it. But if it is November, you have upcoming medical expenses, and you are $300 away from your out-of-pocket maximum, paying through insurance even at a higher copay could actually save you more overall. Once you hit your out-of-pocket maximum, your insurance covers everything at 100 percent for the rest of the year. GoodRx does not count toward that. There is no one right answer. You have to run your own numbers.

Manufacturer Copay Cards

For most major brand-name medications, the company that makes the drug offers a savings card directly on their website. You bring it to the pharmacy and the manufacturer covers part or all of your out-of-pocket cost. This is not charity. Pharmaceutical sales reps visit doctors’ offices regularly, bring meals, and market their specific brand by name. That is a large part of why your doctor writes “Humira” instead of looking up whether a biosimilar costs less. The card is how the manufacturer keeps you on the drug once you are on it.

Here are some of the most widely prescribed brand-name drugs in the country and what their programs currently offer:

Humira, used for rheumatoid arthritis, Crohn’s disease, psoriasis, and other conditions, lists at several thousand dollars per month at retail. AbbVie’s HUMIRA Complete Savings Card lets most commercially insured patients pay as little as $5 per month. Contact: abbvie.com/patients or 1-800-4HUMIRA.

Jardiance, used for type 2 diabetes and heart failure, has no generic. Without any program, the cash price runs around $596 per month. The Jardiance Savings Card from Boehringer Ingelheim can bring commercially insured patients to as little as $10 per fill. Contact: jardiance.com.

Eliquis, a blood thinner, averages over $800 per month at retail. For commercially insured patients, the Eliquis Savings Card brings the cost to as little as $10 per prescription. For Medicare patients, 2026 brought a significant change: Eliquis was one of the first drugs selected for government price negotiation under the Inflation Reduction Act, and Medicare Part D now has a $2,100 annual out-of-pocket cap on all covered prescriptions. Once you hit that cap, Eliquis costs you nothing for the rest of the year. There is also a free 30-day trial offer for new patients. Contact: eliquis.bmscustomerconnect.com or 1-855-354-7847.

Xarelto, another blood thinner, is covered through Janssen CarePath for both commercially insured and Medicare patients. Contact: janssencarepath.com or 1-877-227-3728.

Trulicity, a weekly injection for type 2 diabetes, has a list price around $1,000 per month. The Lilly Savings Card brings commercially insured patients to as little as $25 per fill. Contact: trulicity.lilly.com.

Synthroid, a brand-name thyroid medication, has a copay assistance program through AbbVie for commercially insured patients. People who qualify typically pay significantly less than the standard insurance price, in some cases roughly half. Contact: synthroid.com or abbvie.com/patients.

To find a savings card for any drug not listed here, go to the drug’s website or the manufacturer’s website and look for “patient support,” “savings card,” or “copay assistance.” Or search the drug name plus “savings card” in Google and the manufacturer’s page comes right up. Most major brand-name drugs have one.

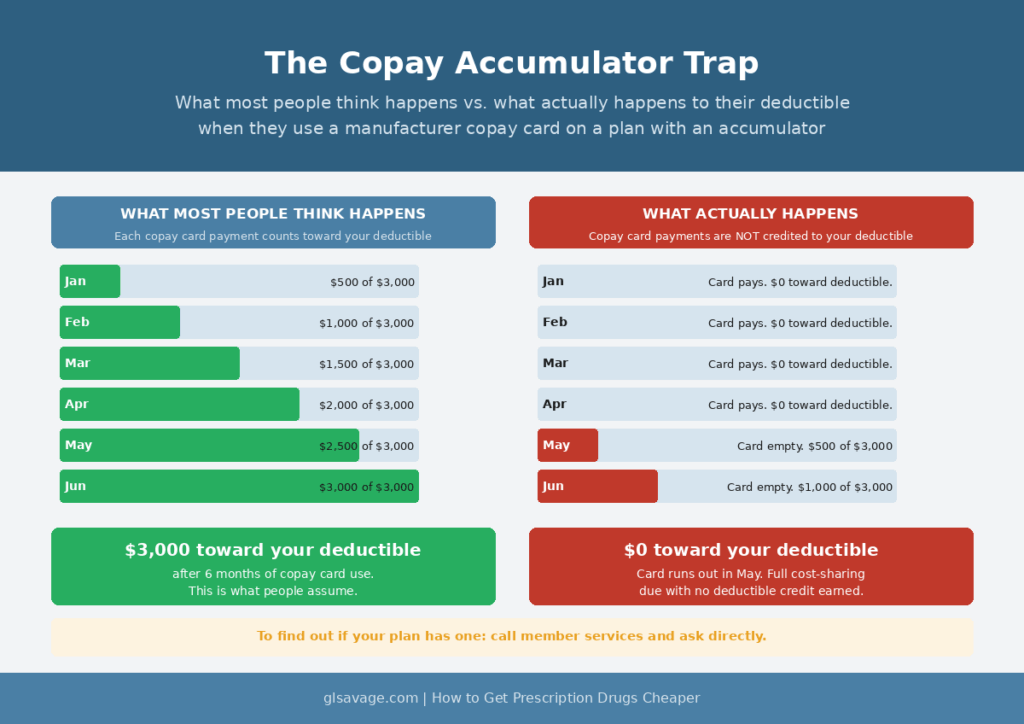

The catch on copay cards: a lot of insurance plans now run something called a copay accumulator program. Under these programs, the money the manufacturer pays through your copay card does not count toward your deductible or out-of-pocket maximum. You use the card all year paying low amounts, the card’s annual limit runs out, and you find out your deductible has not moved at all. People who run into this call it a complete blindside. To find out if your plan has one, call the member services number on your insurance card and ask directly. Look in your plan documents for language like “benefit plan protection program,” “copay adjustment program,” or “out-of-pocket protection program.” Nineteen states have passed laws limiting these programs, but those laws do not cover most employer-sponsored plans, which is where most working people get their insurance. If your plan has an accumulator and you still use the copay card, your monthly cost at the counter is lower. Your deductible is not moving. Go in knowing that.

Medicare and Medicaid enrollees cannot use manufacturer copay cards in the traditional sense, because federal law prohibits manufacturers from subsidizing cost-sharing for government program patients. However, a January 2026 HHS guidance opened a new option: manufacturers can now sell drugs directly to patients in cash, including Medicare and Medicaid patients, as long as the purchase is not billed to any federal program. That means you pay out of pocket, not through Medicare, but at a price the manufacturer sets directly. This does not count toward your Medicare out-of-pocket maximum, so weigh it carefully. For Medicare patients specifically, the bigger development in 2026 is that ten drugs had government-negotiated prices take effect under the Inflation Reduction Act, cutting costs by about 50 percent on average for Part D patients. Eliquis is one of those ten. If you have Medicare Part D, check your plan’s current pricing on these drugs before assuming you need another program.

Patient Assistance Programs

Patient assistance programs are for people who are uninsured, underinsured, or on Medicare and cannot afford their medication. Most are run directly by the drug manufacturer. The income limits are higher than most people expect. These programs are not only for people in poverty.

Ozempic costs over $900 per month without coverage. Novo Nordisk’s patient assistance program covers it for uninsured patients with household income at or below 200 percent of the federal poverty level. For most other Novo Nordisk medications, including Victoza and Saxenda, the income limit is 400 percent of the federal poverty level. Contact: novocare.com.

Trulicity is available through the Lilly Cares Foundation at no cost for qualifying patients who are uninsured or on Medicare Part D and spending at least 4 percent of their gross annual income on prescriptions. The income limit is 300 percent of the federal poverty level. Contact: lillycares.com or 1-800-545-6962.

Humira without commercial insurance is available at no cost to qualifying patients through the AbbVie Patient Assistance Foundation. Contact: 1-800-222-6885.

Eliquis without coverage is available through the Bristol Myers Squibb Patient Assistance Foundation for people who are uninsured or on Medicare and have spent at least 3 percent of their annual household income on out-of-pocket prescription costs. Contact: bms.com or 1-800-736-0003.

Insulin, any brand: Novo Nordisk has capped widely used products including NovoLog and Tresiba at $35 per month. Sanofi expanded its Insulins ValYOU Savings Program in January 2026 to cap all of its insulin products at $35 per month for every patient in the U.S., regardless of insurance status. Eli Lilly’s insulin programs are at lillycares.com. To enroll in Sanofi’s program, call 1-888-847-4877 or go to their website directly. If you are paying more than $35 a month for any insulin, there is a program you have not found yet.

The catch on patient assistance programs: there is no standard process. Every manufacturer runs their own program differently. Some have a 15-minute online application. Others require your doctor’s office to complete a portion of the paperwork, which can add a week or two. Most programs do not backdate. If you enroll in March, you do not get credit for what you paid in January and February. Start the process as soon as you know you need help.

How to Find a Program for Any Medication

Three free tools exist specifically to find assistance programs by drug name. Use all three because they pull from different databases and one will sometimes find a program the others miss.

NeedyMeds.org covers more than 5,000 programs. Type your medication name in the search bar. A PAP symbol next to the drug name links directly to eligibility guidelines, income requirements, and how to apply. NeedyMeds also runs a phone helpline at 1-800-503-6897 for people without internet access.

RxAssist.org lets you search by drug name, brand name, or manufacturer. It is one of the oldest and most consistently updated databases in this space.

MedicineAssistanceTool.org is run by PhRMA, the pharmaceutical industry’s own trade group. It is built to find manufacturer programs specifically. Enter your drug name, answer a few questions about your insurance situation, and it returns what you may qualify for.

Everything Else That Can Lower Your Cost

Ask about a 90-day supply. Most insurance plans and most discount programs charge less per dose on a 90-day fill than a 30-day one. You pay more in one transaction but less across the year, and you make fewer trips to the pharmacy.

Call around to different pharmacies before you fill. The same drug can cost a lot more at one pharmacy than another. Chain pharmacies, independent pharmacies, and warehouse stores like Costco often charge different prices for the same medication. Costco’s pharmacy is open to the public for prescription purchases in most states with no membership required. Independent pharmacies sometimes have more flexibility on pricing than chains because they operate under different PBM contracts. Calling two or three pharmacies takes ten minutes.

Ask your doctor for samples. Drug companies give large quantities of samples to doctors’ offices every year. For a new prescription especially, your doctor may be able to give you enough to last while you figure out the best long-term option. Most people never ask.

If you have Medicare and are struggling with drug costs, look into the Extra Help program through Social Security. It helps cover Part D premiums, deductibles, and copays based on income and resources. The application is free at SSA.gov. If you qualify for Extra Help automatically through Medicaid or Supplemental Security Income, you are already enrolled.

Ask your pharmacist directly what the lowest price they can offer is. Since the 2020 gag clause legislation, pharmacists are allowed to tell you. A lot of them will look for a better option if you ask. Most people never ask.

The system is not going to walk you through any of this. The price on the screen is what the industry expects you to pay, because most people do.

Frequently Asked Questions

Go to the drug’s website or the manufacturer’s website and search for “patient support,” “savings card,” or “copay assistance.” You can also search the drug name plus “savings card” in Google and the manufacturer’s page comes right up. Most major brand-name drugs have one. The main limit is that most require commercial insurance. Medicare and Medicaid enrollees cannot use manufacturer copay cards because federal law prohibits it. If you have Medicare or Medicaid, patient assistance programs are the route to look into.

Yes. GoodRx is not insurance. It is a discount tool you use instead of your insurance card for a given fill. Compare the GoodRx price to your copay and tell the pharmacist which one to run. The thing to know is that GoodRx purchases typically do not count toward your deductible or out-of-pocket maximum. If you are close to hitting those limits, factor that in before you decide. If you are far from them, the GoodRx price is usually the better deal on that fill.

Generally people who are uninsured, underinsured, or on Medicare and cannot afford their medication. Income limits vary by manufacturer and by drug. Novo Nordisk covers most of its medications for households at or below 400 percent of the federal poverty level. The Lilly Cares Foundation uses similar thresholds. Many households that would not call themselves low-income still qualify. The only way to know for your specific drug is to search it on NeedyMeds.org or check the manufacturer’s website directly.

Yes, and it happens more often than most people expect. If the GoodRx or SingleCare price is lower than your copay and you are not close to hitting your deductible or out-of-pocket maximum, paying cash saves you money on that fill with no real downside. If you are near your out-of-pocket maximum and every dollar through insurance pushes you toward that limit, the higher copay through insurance can actually be the better move because once you cross the maximum your insurance pays 100 percent. It depends on your plan, your numbers, and where you are in the plan year.

A copay accumulator is a policy where the money a drug manufacturer pays through your copay card does not count toward your deductible or out-of-pocket maximum. Your insurer takes the manufacturer’s payment at the pharmacy counter but does not apply it to what you owe toward your plan limits. When the card’s annual limit runs out mid-year, you suddenly owe your full cost-sharing with no progress made toward your deductible. To find out if your plan has one, call the member services number on your insurance card and ask directly. Also look in your plan documents for language like “benefit plan protection program,” “copay adjustment program,” or “out-of-pocket protection program.”