A bill arrives. It looks official. It says “amount due” and sometimes “due upon receipt” in capital letters. Most people see that and reach for a way to pay it. That is exactly what the system is designed to make you do. Pay quickly, pay the full amount, and do not ask questions. The problem is that the bill you received may contain errors you were never meant to find, a price inflated beyond any reasonable connection to the cost of your care, and options you were never told exist. Medical debt is different from every other kind of debt, and understanding how it actually works is the difference between paying a number someone invented and paying what you actually owe.

The First Number on a Medical Bill Is Often Not the Real Price

Hospitals maintain internal price lists called chargemasters. These are not calm, market-based prices. They are inflated sticker prices designed to give hospitals room to negotiate with insurance companies and generate larger-looking discounts on paper. The list price on your bill and the real economic value of your care are often two very different numbers.

That means two people can receive the exact same treatment and get billed wildly different amounts. One gets the insurer’s negotiated rate. The other gets billed off the inflated list price. Patients who show up without insurance or without knowledge are usually the only ones in the room expected to treat that first number as fixed.

It is not fixed. It is the opening move.

The Bill You Received May Already Contain Errors

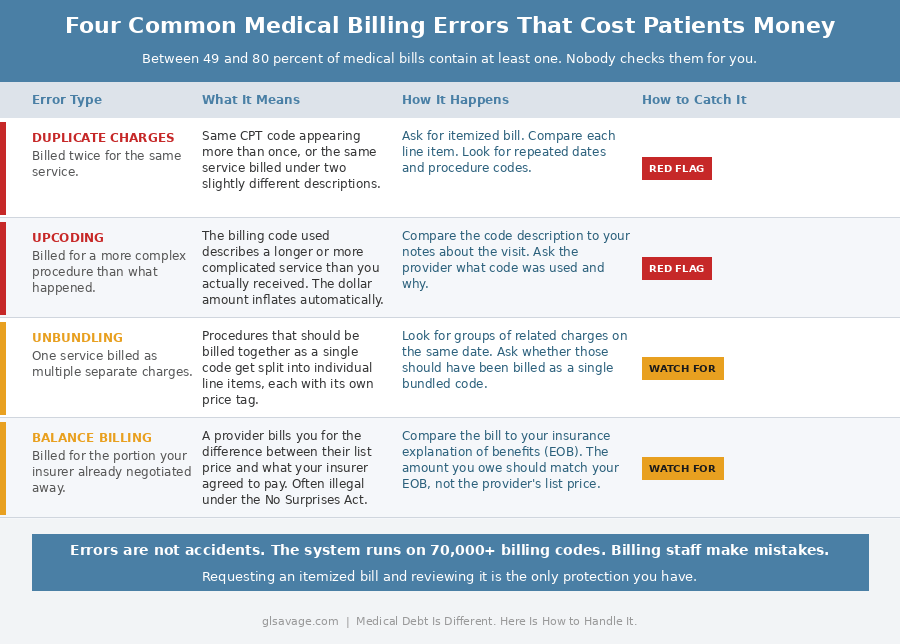

Before you pay anything, understand this: industry research consistently finds that between 49 and 80 percent of medical bills contain at least one error. That is not a fringe statistic. It comes from medical billing auditors, healthcare advocacy groups, and academic research. Billing errors are not the exception. They are close to the norm.

The errors follow predictable patterns. Duplicate charges bill you twice for the same service. Upcoding assigns a billing code for a more complex procedure than what actually happened, which inflates the dollar amount automatically. Unbundling separates procedures that should have been billed as a single charge into individual line items, each with its own price. A single emergency room visit can generate separate bills from the hospital facility, the attending physician, a radiologist, the lab, and an anesthesiologist who may be employed by a third-party staffing company entirely separate from the hospital. Each entity bills independently, often using different software and different coding staff.

The system runs on over 10,000 CPT procedure codes and 70,000-plus diagnosis codes. Errors are structurally inevitable. Asking for an itemized bill and checking it line by line is not paranoia. It is the basic due diligence the system requires of you because it is not doing it for you. You can look up CPT codes through the American Medical Association’s site at no cost, up to five lookups a day for free, to verify what you were actually billed for versus what actually happened in the room.

The Cash Price Can Be Lower Than the Insured Price

People assume insurance automatically gets them the best deal. Not always.

Hospitals and clinics sometimes offer self-pay pricing, prompt-pay discounts, or bundled cash rates that come in below what an insured patient owes after deductibles, coinsurance, and facility charges. Insurance billing is slow, complex, and expensive to process. Cash is clean and immediate. The savings sometimes get passed on.

That does not mean you should skip insurance. It means you should ask one specific question before paying anything: what is the self-pay price, and is it lower than my insured amount? A significant number of people never ask, because the system trains them not to. If you want to know what a procedure should reasonably cost before any of this, Healthcare Bluebook and Fair Health Consumer are free tools that show you what procedures actually cost in your area. That number is useful in any negotiation.

The Facility Fee Trap Is One of the Dirtiest Tricks in Medical Billing

A clinic gets bought by a hospital system. The sign outside may barely change. The doctor may be the same. The exam room may be the same. But the bill changes.

Now you may see a professional fee for the doctor and a separate facility fee for the location itself. Same visit. Larger bill. Most patients never agreed to that shift in any meaningful way. They find out after the fact that routine care is suddenly being billed through a hospital-owned structure that charges for the privilege of the building.

This is not a small technicality. It is one of the ways ordinary appointments quietly become much more expensive, and nothing in the system requires the provider to warn you before it happens. Ask before any appointment whether the practice is hospital-affiliated and whether a facility fee will appear on your bill. Ask what that fee covers. In some cases you can dispute it, particularly if you received no advance notice.

Being In-Network Does Not Always Mean You Are Protected

You chose an in-network hospital. You did everything right. Then the anesthesiologist, radiologist, assistant surgeon, or pathology lab shows up on the back end as out of network, and you get a bill for the difference.

That pattern got bad enough that federal law had to intervene. The No Surprises Act, which took effect January 1, 2022, now blocks many of these out-of-network balance bills for emergency care and for certain providers working inside in-network facilities. It also requires providers to give uninsured and self-pay patients a good-faith cost estimate before care is delivered. If the final bill comes in $400 or more above that estimate, you have the right to dispute it through a formal patient-provider dispute resolution process.

Most patients do not know this pathway exists. The law does not make the system clean, but it created a specific, usable dispute mechanism. If you were surprised by an out-of-network bill or a bill that significantly exceeded a pre-care estimate, the No Surprises Act may give you grounds to formally challenge it. That leverage exists whether or not the billing department volunteers it.

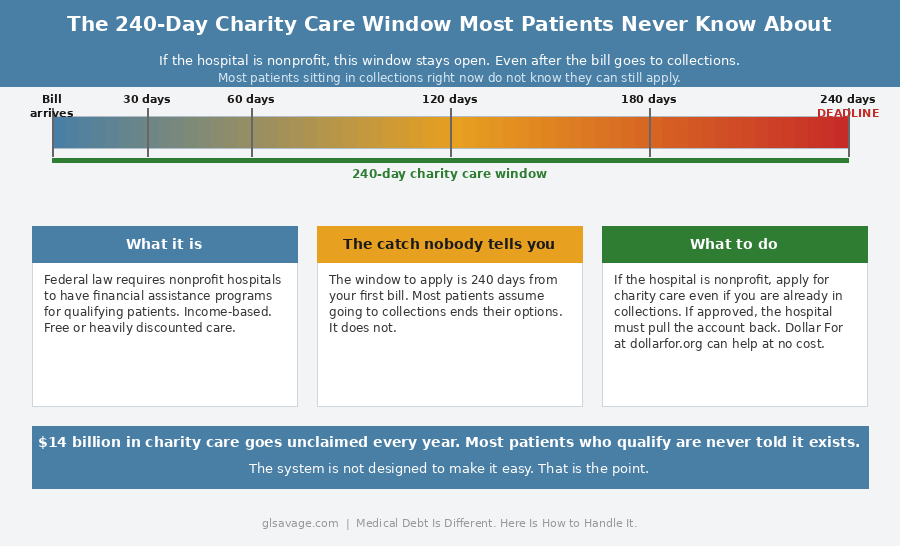

Nonprofit Hospitals Are Required to Have Financial Assistance Programs. Most Do Not Lead With That.

Under federal law, tax-exempt nonprofit hospitals are required to maintain written financial assistance policies, sometimes called charity care, as a condition of their nonprofit status. Some of them are legally required to provide free or steeply discounted care to qualifying patients.

The gap between what exists and what patients actually receive is enormous. A 2024 analysis found that hospitals fail to provide at least $14 billion annually in charity care to patients who would qualify if they applied. The CFPB has documented cases where patients whose bills had already been waived still ended up in collections because the internal systems failed and nobody told them.

The application process is deliberately difficult in many cases. Hospitals have invested resources in building seamless payment portals. The charity care application tends to be clunky, with unclear eligibility criteria and documentation requirements that vary by hospital. The system is not designed to make it easy to discover you do not owe the bill.

Patients typically have up to 240 days from the first bill to apply for charity care. That window does not close when the bill goes to collections. If a charity care application is approved after an account has already been sent to a collector, the hospital is required to pull it back. Most people sitting in collections right now do not know that.

If the hospital is nonprofit, financial assistance should be the first thing you check, not the last. Dollar For is a free nonprofit that helps patients navigate hospital financial assistance applications at no cost. They have helped patients discharge over $120 million in medical debt. That resource exists. Most people never hear about it.

If you are dealing with a serious or chronic condition, the Patient Advocate Foundation offers free case management services for patients navigating financial hardship related to medical treatment. Also free. Also underused.

Medical Debt and Credit Reporting: What the Rules Actually Say Right Now

The credit reporting rules around medical debt have been changing fast, and where they stand right now matters for real decisions people are making today.

In 2022, the three major credit bureaus, Equifax, Experian, and TransUnion, voluntarily stopped including paid medical collections on credit reports. They also agreed to stop reporting unpaid medical collections under $500, and to apply a one-year waiting period before reporting any unpaid medical collection. Those voluntary changes are still in effect.

In January 2025, the CFPB finalized a broader rule that would have removed all medical debt from credit reports entirely and barred lenders from using it in credit decisions. The agency estimated this would have erased $49 billion in medical debt from the reports of 15 million Americans, raising their credit scores by an average of 20 points. A federal court vacated that rule in July 2025. It is not currently in effect at the federal level.

However, fifteen states including California, New York, Colorado, and Illinois have passed their own versions of the protection. If you live in one of those states, medical debt may already be prohibited from appearing on your credit report regardless of what happens federally. Knowing whether your state is on that list before making any decision driven by credit score fear is worth five minutes of your time. Understanding how collection accounts affect your credit report is the broader context for why this distinction matters.

The practical reality right now: collectors use urgency because it works. A bill sitting in collections for medical debt is not the same financial emergency the language around it implies. Knowing the actual rules in your state, rather than the fear the bill is designed to create, is what gives you real information to act on.

Hospitals Often Recover Far Less Than the Original Bill

Once a medical debt account moves deep into collections, the economics change. Hospitals and collection agencies often recover a fraction of the face value. That is one of the structural reasons settlement is possible.

The original number on the statement can look immovable. The actual recovery math behind the scenes is often very different. Asking for the settlement amount, using those exact words, is a recognized signal in medical billing that you have cash available and want to close the account today. Patient advocates and billing experts consistently report that starting a settlement offer at 50 percent or less of the balance is a reasonable opening position. Get any agreed settlement in writing before a payment is made. Verbal agreements in this context are not practically enforceable. The sequence is: negotiate, get it in writing, then pay.

What to Do Before You Pay Anything

Slow down long enough to get the structure right.

Ask for an itemized bill. Verify that insurance processed the claim correctly. Ask whether there is a self-pay price that beats your insured amount. Ask whether the provider offers a prompt-pay discount. Ask whether the hospital is nonprofit and has a financial assistance policy, and whether you qualify. Ask whether a facility fee was added and what it covers. Check whether the bill reflects what actually happened, because errors are common and nobody is checking on your behalf.

Do not assume the first number is clean. Do not assume the billing department volunteered every option available to you. The same principle that explains how banks make money from overdraft fees applies here: the default outcome benefits the institution. Changing it requires asking questions the system is not going to prompt you to ask.

What to Do If Medical Debt Is Already in Collections

You still have options. You have more time than the collector wants you to think.

If the original hospital was nonprofit, apply for financial assistance even now. The hospital is required to pull the account back from the collector if you are approved. Most people in collections never try this because they do not know the window is still open.

If the debt is valid but inflated or contains errors, dispute the specific charges in writing. If the balance is real and you want to close it, ask for the settlement amount and start from 50 percent or less. Get whatever you agree to in writing before money moves.

The credit reporting rules in your state matter here too. If you are in one of the fifteen states with medical debt protections, collections urgency has less credit leverage over you than the collector implies. Find out where your state stands before you respond to pressure.

If the debt load is significant and involves multiple accounts, a nonprofit credit counselor can help you see the full picture before you make payment decisions that cannot be undone. The National Foundation for Credit Counseling at nfcc.org connects people with accredited agencies at low or no cost.

Medical Debt Is Different, Which Means the Playbook Is Different

Medical debt is different because the entire structure behind it is different from other debt. Inflated chargemaster prices. Billing error rates close to half of all bills. Cash-price loopholes. Facility fee traps. Surprise billing protections most patients do not know they have. Charity care programs hospitals are legally required to maintain but do not advertise. A 240-day window that stays open even after collections. Settlement math that looks nothing like the number on the statement. Credit reporting rules that vary by state and are actively shifting.

This is not just debt. It is a billing system designed to look more fixed than it actually is. The bill is not a verdict. It is an opening position.

Frequently Asked Questions About Medical Debt

Can medical debt still hurt your credit score?

Yes, though the rules have changed significantly. Paid medical collections no longer appear on reports from the three major bureaus. Unpaid collections under $500 are not reported, and larger unpaid collections have a one-year waiting period before appearing. A federal rule that would have removed all medical debt from reports was vacated by a court in July 2025. Fifteen states have passed their own versions of that protection. Whether you live in one of those states determines how much medical debt can currently affect your credit.

How common are errors on medical bills?

Very. Industry research and medical billing auditors consistently find that between 49 and 80 percent of medical bills contain at least one error. Common errors include duplicate charges, upcoding to a higher-complexity billing code than what actually happened, and unbundling of procedures that should have been billed together. Requesting an itemized bill and reviewing it line by line is the only reliable way to catch them.

Can you negotiate a medical bill before it goes to collections?

Yes, and that is usually the best time. Hospitals may offer discounts, payment plans, prompt-pay reductions, or financial assistance before an account moves further into the collection pipeline. Asking for the settlement amount directly signals that you have cash available and want to close the account, which often moves the conversation faster than explaining financial hardship.

What is a facility fee and can you dispute it?

A facility fee is a separate charge billed for the physical location when a clinic or office is owned by a hospital system. It can make a routine visit significantly more expensive, usually without any advance notice to the patient. You can ask the billing department to explain and justify the fee. If you were not informed of it beforehand, a dispute is worth attempting.

Can a nonprofit hospital reduce or erase your medical debt?

Yes. Tax-exempt nonprofit hospitals are required by federal law to maintain financial assistance policies for qualifying patients. Eligibility is based on income and varies by hospital. Patients typically have up to 240 days from the first bill to apply, and that window stays open even after the account has gone to collections. Most people eligible for this assistance are never clearly told it exists. Dollar For at dollarfor.org provides free help navigating these applications.

Should you ask for the cash price even if you have insurance?

Yes. Sometimes the self-pay or prompt-pay price is lower than what you owe through insurance after your deductible and coinsurance are applied. Ask before paying. The billing department will not volunteer this information.

What is the No Surprises Act and does it protect you from all unexpected medical bills?

The No Surprises Act, effective January 1, 2022, protects patients from many out-of-network balance bills, particularly in emergencies and for certain providers working inside in-network facilities. It also requires providers to give uninsured and self-pay patients a good-faith cost estimate before care. If the final bill exceeds that estimate by $400 or more, you have the right to dispute it through a formal process. The law does not cover every surprise billing situation, but it created a dispute pathway that most patients do not know they can use.

What does it mean to negotiate a medical debt settlement?

Settlement means paying a lump sum less than the full balance to close the account entirely. Hospitals and collectors often recover a fraction of the face value of a bill, which is why settlement is structurally possible. Start an offer at 50 percent or less of the balance. Always get the agreed terms in writing before making any payment. The sequence is negotiate, confirm in writing, then pay.

What is Dollar For and how does it help with medical debt?

Dollar For is a free nonprofit that helps patients apply for hospital financial assistance programs. They handle the paperwork and navigation at no cost to the patient. They have helped discharge over $120 million in medical debt. If the hospital is nonprofit and you think you might qualify for charity care, Dollar For at dollarfor.org is the fastest way to find out and apply.

Should you put medical debt on a credit card to pay it off?

Generally no. Most hospital payment plans do not charge interest, which makes them significantly cheaper than credit card debt. Putting a medical bill on a card converts non-interest-bearing debt into interest-bearing debt. Negotiate a direct payment plan with the hospital or provider first. If that fails and the balance must be addressed, a zero-percent introductory APR card with a realistic payoff timeline is a better option than a standard card. Either way, minimum payments keep you in debt and the math on medical credit card debt can get away from you fast.