Every month a bill arrives with two numbers on it. The full balance and a smaller number at the bottom. The smaller number is what the card company wants you to look at. It is designed to feel manageable, like responsibility, like you are doing the right thing. What the bill does not say is that paying only that number is one of the most expensive financial decisions most people make every month, repeated for years, sometimes decades, and that the number itself was calculated by people whose financial interest is the opposite of yours. Minimum payments keep you in debt because they were built to. That is not a side effect. That is the business model.

What a Minimum Payment Actually Does

Most minimum payments are calculated as one to three percent of your outstanding balance, or the interest charge plus a small slice of principal, whichever is higher. Either way, the formula exists to keep the balance declining as slowly as the law allows.

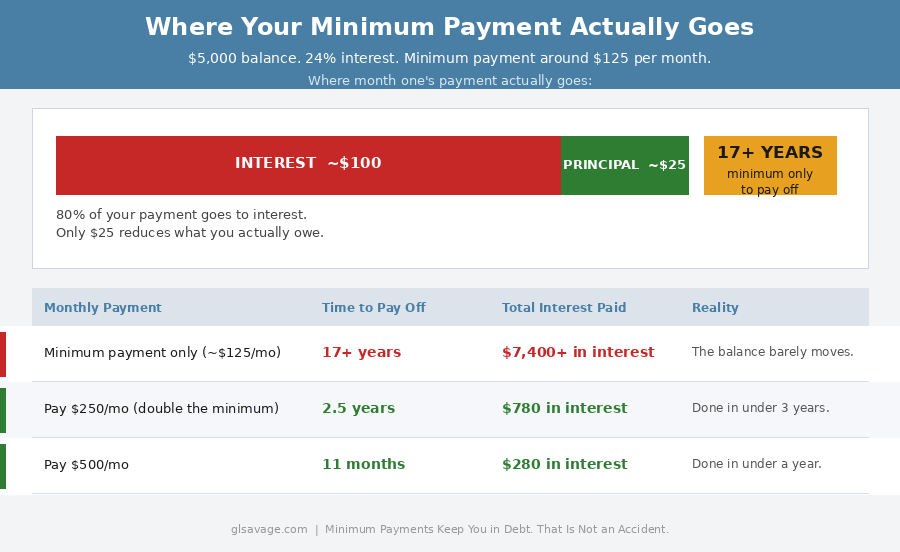

On a $5,000 balance at 24 percent interest, a minimum payment of around $125 to $150 sends the vast majority of that money straight to interest in the early months. The principal barely moves. The account stays current. The balance lingers.

That is the point. A balance that lingers generates revenue. A balance that gets paid off does not. Minimum payments keep you in debt because a paid-off account is worth nothing to the lender. An account that stays open, carries a balance, and generates monthly interest income is worth a great deal.

What most people do not know is that credit card interest is not calculated once a month. It compounds daily, based on your average daily balance. Every day you carry a balance, interest accrues. The monthly interest charge on your statement is the sum of 30 days of daily interest calculations. That means the balance grows faster than most people intuitively expect, and minimum payments that barely cover the monthly interest charge are fighting a compounding machine with a bucket.

The Disclosure That Should Have Changed Everything

In 2009, Congress passed the Credit CARD Act. One of its requirements: card issuers must print a payoff disclosure box on every statement showing how long it will take to pay off the balance making only minimum payments, and how much total interest will be paid. They must also show how much you would need to pay each month to clear the balance in three years.

Read that box on your next statement. The timeline is usually uncomfortable. On a $5,000 balance at 24 percent interest, making only minimum payments, payoff can stretch to 17 years or more. Total interest paid can exceed the original balance several times over.

The fact that a law had to be passed to require that disclosure tells you everything about what was happening before it existed. Card issuers were not volunteering the information. Regulators had to force it onto the statement. That is not how a system designed in the consumer’s interest behaves. Minimum payments keep you in debt longer when you cannot see the actual timeline, which is exactly the situation that existed before 2009.

The Psychology Behind the Number

Research on consumer payment behavior found that the minimum payment displayed prominently on a credit card statement acts as an anchor. People do not calculate what they can afford to pay and then compare it to the minimum. They see the minimum, they treat it as a reference point, and they pay close to it. A study found that when the minimum payment amount was hidden or made less prominent on the statement, people increased their monthly payments by an average of 70 percent. The same financial situation. More money toward the balance. Simply because the anchor was removed.

Card issuers know this. The minimum payment is not placed prominently on the statement because it is the most important number. It is placed prominently because making it the most visible number keeps payments low and keeps balances alive longer. That is a design decision, not a formatting accident.

The minimum payment trap works because it feels like enough. It keeps the account current. It avoids late fees. It does not trigger any immediate negative consequences. Minimum payments keep you in debt quietly, in the background, while nothing alarming is happening on the surface. Survivable is not the same as solvable. The minimum payment makes debt survivable. That is what it was built to do.

The Math Behind the Minimum Payment Trap

Credit card interest rates currently average around 21 to 23 percent, with many cards running higher. At those rates, interest compounds daily. When the minimum payment barely covers the monthly interest charge, the principal shrinks at a pace that can stretch repayment into years. Sometimes longer than a car loan. Sometimes longer than a mortgage. On a large balance at a high rate, sometimes longer than you have been working.

The situation compounds further when new charges land on the card while only the minimum is being paid. Groceries. A car repair. A medical bill. The balance stops declining. Sometimes it grows. And because minimum payments keep you in debt by design, once the balance starts climbing it takes significantly more than the minimum just to hold it steady, let alone reduce it. This is how people end up carrying credit card debt for years while paying their bills on time every single month without missing a payment. The account is current. The debt is permanent. Many people making consistent minimum payments discover years later that the balance barely moved. That is not unusual. That is what the minimum payment trap produces. The same system that makes money from your overdraft fees makes money from this too. The mechanisms are different. The design philosophy is identical.

What the Card Company Does Not Want You to Ask For

Most people in financial hardship do not know that hardship programs exist. Card issuers offer them. They do not advertise them. They are not listed on the website. You find out about them by calling the number on the back of your card and asking directly.

Hardship programs can temporarily reduce your interest rate, lower your minimum payment, waive fees, or restructure your payment schedule. The terms vary by issuer and by how long you have been a customer. Some require you to close the card while enrolled. Some do not. None of this will be offered to you unless you ask. The account is profitable as it is. There is no incentive to offer you a better deal until you request one.

Call. Tell them: “I am having financial difficulty and I would like to know if there is a hardship program available on my account.” If the first representative does not know, ask for a supervisor. It costs nothing. It sometimes works.

Balance Transfers: The Exit With a Catch

A balance transfer moves your existing balance to a new card with a promotional zero percent interest rate, typically for 12 to 21 months. During that window every dollar you pay goes toward the principal. No interest. The math changes completely.

The catch is real and it needs to be said plainly. Balance transfer cards charge a transfer fee, typically 3 to 5 percent of the amount moved. On a $5,000 balance that is $150 to $250 upfront. The zero percent rate is promotional. When the period ends, the rate typically jumps to whatever the card’s standard rate is, which may be just as high as the card you came from. If you have not paid off the balance by then, you are back in the same situation on a different card.

This option works when you have a concrete payoff plan and can execute it within the promotional window. Before you transfer, do the math. Divide the balance plus the transfer fee by the number of months in the promotional period. That is what you need to pay each month to clear it before the rate expires. If that number is realistic, do it. If it is not, you are moving the problem, not solving it.

Avalanche vs. Snowball: Both Work, One Costs Less

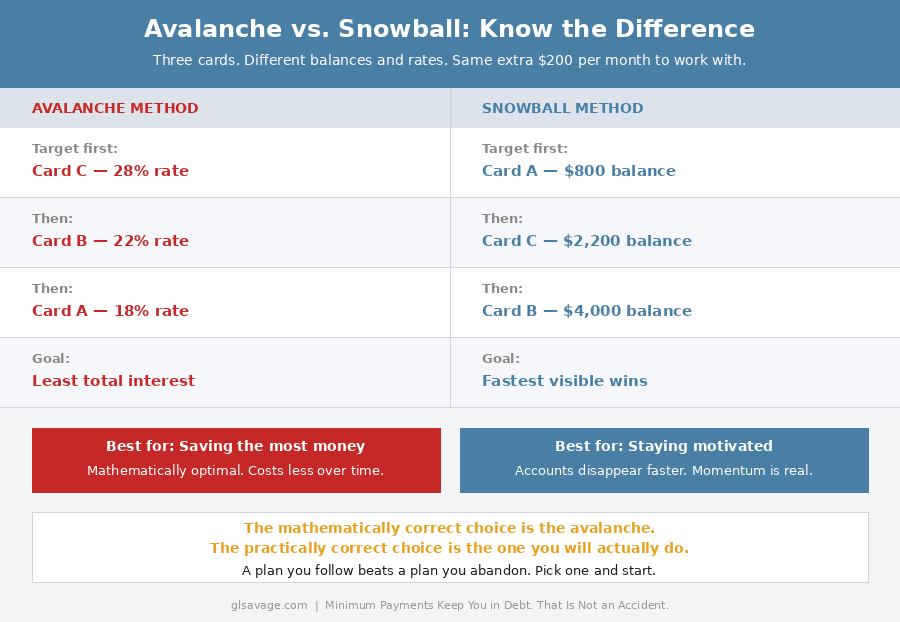

The avalanche method targets the card with the highest interest rate first. Make minimum payments on every other card and put every extra dollar toward the highest-rate balance. When it is gone, roll that payment to the next highest rate. This is the mathematically efficient path. It minimizes the total interest paid over the life of the debt.

The snowball method targets the smallest balance first regardless of interest rate. Pay it off, eliminate it, and roll the freed payment to the next smallest. The wins come faster. Accounts disappear. The psychological momentum is real and for a lot of people it is the difference between staying with a plan and abandoning it.

The mathematically correct choice is the avalanche. The practically correct choice is the one you will actually do. If you need to see progress to stay motivated, the snowball is not a worse strategy. It is a better one, because a strategy you follow is always more effective than a theoretically optimal one you quit.

What Nonprofit Credit Counseling Actually Is

Most people in credit card debt confuse nonprofit credit counseling with something predatory.

Nonprofit credit counseling agencies are not debt settlement companies. Debt settlement companies charge fees, damage your credit, and negotiate to pay creditors less than you owe, which sounds appealing until you understand the tax implications, the credit damage, and the fees involved. Nonprofit credit counselors operate differently.

The National Foundation for Credit Counseling, at nfcc.org, connects consumers with accredited nonprofit agencies that offer debt management plans. A debt management plan consolidates your credit card payments into one monthly payment, negotiates lower interest rates with your creditors on your behalf, and gives you a structured timeline to pay off the debt in full, typically three to five years. Fees are low or waived entirely based on financial hardship. The debt gets paid. The creditors get paid. The interest rate is lower. The plan is structured. It is not fast, but it is real.

What to Actually Do

Before anything else: protect your income first. Credit card debt is expensive. Losing the job or the car that generates the money to pay any of it is worse. Your rent or mortgage, your car payment if the car gets you to work, your utilities, your phone, your insurance. These come before extra credit card payments. Every time. A credit card balance can be managed, negotiated, or restructured. A repossessed car or an eviction puts you somewhere harder to come back from. Do not sacrifice the thing that produces income to accelerate the payoff of the thing that costs interest.

Once the essentials are protected and there is actual margin, put it to work.

The minimum payment is sometimes the only option. When cash runs out, paying the minimum protects the account, preserves the payment history, and keeps the credit score intact. Use it for that when you have to. There is no shame in it. That is what it is there for. The financial pressure that leads people to carry balances and pay minimums is real and systemic. The poverty premium means that being short on cash costs you more at almost every turn. Credit card interest is one of the most expensive of those costs.

The problem is treating it as a permanent strategy, which is exactly what the system is designed to encourage you to do.

If there is any margin at all after the essentials, put it toward the balance. Even $20 or $30 extra a month makes a measurable difference because every dollar of principal reduced is a dollar that interest stops being calculated on. The math compounds in your favor when the balance drops faster than the minimum requires.

Check whether your card issuer has a hardship program. Most do. None of them advertise it. Call and ask.

If you are carrying balances on multiple cards, pick a method and work it. Avalanche if you want to minimize total interest. Snowball if you need the psychological momentum of eliminating accounts. Either one moves the needle. The minimum payment on every card while adding new charges does not.

If the debt feels unmanageable, contact a nonprofit credit counselor through nfcc.org before you contact a debt settlement company. They are not the same thing and the difference is significant. And if any of your accounts have already gone to collections, understanding how collection accounts affect your credit report separately from the original debt is important before you make any payment decisions.

Understanding how credit scores work matters here too. A high credit card balance relative to your limit hurts your score even if you never miss a payment. Paying down the balance is not just about the interest. It improves your utilization ratio, which is 30 percent of your FICO score. Debt reduction and credit building are the same action. If you are also working on building an emergency fund, even a small one, the goal is to create enough margin that the next emergency does not go on a card that will then sit at minimum payment for years.

The System Is Counting On One Thing

The minimum payment is low because a low number feels manageable. It feels manageable because it was designed to feel manageable. The anchor is placed where you will see it. The payoff timeline is placed where you probably will not. The hardship program is not mentioned at all. The daily compounding is not explained. The anchoring research exists and card companies know it and the statement design has not changed.

Minimum payments keep you in debt because a debt that is serviced but never retired is a permanent revenue stream. A borrower who pays the minimum every month on time for twenty years is, from the card company’s perspective, the ideal customer. Not because they are irresponsible. Because the system was built around their reliability.

Now you know how it works. What you do with that is up to you.

Frequently Asked Questions

Because a low minimum payment keeps accounts active, reduces defaults, and extends the period during which interest accumulates. It is a revenue model built on the borrower staying current without paying off the balance. Research shows that displaying the minimum payment prominently on a statement causes people to anchor to that number and pay close to it, which benefits the issuer. When the minimum is made less visible, monthly payments increase significantly.

It depends on the balance and rate, but it can stretch to 17 years or more on a $5,000 balance at 24 percent interest. Your statement is required by the CARD Act of 2009 to include a payoff estimate. That disclosure box exists because card companies were not volunteering the information before the law required it. Read it on your next statement.

Paying on time protects your payment history, which is the largest factor in your score. The problem is that carrying a high balance relative to your credit limit raises your utilization ratio, which is 30 percent of your score. A balance that stays high because you are only making minimum payments quietly drags your score down even when every payment is on time.

Research has found that displaying the minimum payment prominently on a statement causes consumers to treat it as a reference point for how much to pay, rather than calculating what they can actually afford. Studies found that when the minimum payment was made less visible, average monthly payments increased by around 70 percent. Card companies know this. The placement of that number on the statement is not accidental.

A hardship program is an arrangement offered by most major card issuers that can temporarily reduce your interest rate, lower your minimum payment, or restructure your payment schedule. They are not advertised. You find out about them by calling the number on the back of your card and asking directly. Some require you to close the card while enrolled. None of them will be offered until you ask.

It can be, if you have a realistic payoff plan. Divide the balance plus the transfer fee by the number of months in the promotional period. That is the monthly payment required to clear the balance before the zero percent rate expires. If that number is achievable, the transfer makes sense. If it is not, you are moving the debt without solving it, and the rate that kicks in at the end may be just as high as the one you came from.

The avalanche method targets the highest interest rate balance first, which minimizes total interest paid. The snowball method targets the smallest balance first, which produces faster visible wins and momentum. The avalanche is mathematically optimal. The snowball is psychologically powerful. The correct one is the one you will actually stick with. A plan you follow beats a plan you abandon.

Nonprofit credit counselors, such as those connected through the National Foundation for Credit Counseling at nfcc.org, offer debt management plans that consolidate payments, negotiate lower interest rates with creditors, and structure a payoff timeline, typically three to five years. Fees are low or waived. The debt gets paid in full. Debt settlement companies, by contrast, charge significant fees, negotiate to pay creditors less than you owe, and can cause credit damage. They are not the same thing and the distinction matters significantly.

Because interest is charged on the outstanding balance every day, and when the balance is large and the rate is high, the monthly interest charge consumes most of a small payment. What remains after interest is applied to the principal, and on a minimum payment that remainder is tiny. This is why minimum payments keep you in debt so effectively. The interest machine is running faster than the payment is reducing what feeds it.

When cash is not available. The minimum payment protects the account, preserves the payment record, and keeps the credit score from taking a late-payment hit. It is a short-term survival tool. The problem is not using it in a tight month. The problem is when it becomes the permanent default, which is exactly what the card company is hoping for.