There is a legal deadline on how long a debt collector can sue you to collect a debt. Once that deadline passes, the debt is called time-barred, and suing you to collect it is illegal. That protection exists for every person carrying old debt in this country. Most of them have never heard of it. The statute of limitations on debt is one of the most powerful consumer protections in the law and one of the least understood. Collectors know the clock exists. They are betting you do not. And when you do not know about it, you can lose everything, including in court, on a debt you had no legal obligation to pay.

What the Statute of Limitations on Debt Actually Is

The statute of limitations on debt sets a hard deadline on how long a creditor or collector has to sue you in court to recover what you owe. After that deadline passes, the debt is not erased. You still owe it. But the collector loses the legal right to take you to court over it. They cannot get a judgment against you, which means they cannot use the court system to garnish your wages, freeze your bank account, or place a lien on your property. The debt becomes, in legal terms, time-barred.

The length of that window varies by state and by debt type. Most states fall somewhere between three and six years. Some go longer. The clock typically starts ticking from the date of your last payment or the date the account first became delinquent, depending on your state’s specific rules. It does not start from when the account was opened, when it was charged off, or when it was sold to a debt buyer. Those are different dates entirely and collectors sometimes try to blur them.

Two types of debt work differently. Federal student loans have no statute of limitations at all. The government can pursue them indefinitely. Judgments, meaning court orders already entered against you, have their own separate window that is often much longer than the original debt’s limitation period, sometimes ten to twenty years, and can often be renewed.

The Protection Is Real but It Is Not Automatic

The statute of limitations on debt does not protect you automatically. You have to show up and use it.

The statute of limitations is an affirmative defense. That means you have to raise it in court for it to protect you. It does not fire automatically. If a collector sues you on a time-barred debt and you do not show up to court, the judge will enter a default judgment against you, no questions asked, no requirement that the collector prove the debt is within the statute. You simply did not respond, so the court assumes the debt is valid and awards the judgment.

This is not a theoretical problem. Debt buyers file lawsuits by the thousands on debts they know are near or past the statute of limitations, specifically because they know the overwhelming majority of people will not respond. When you do not show up to raise the statute of limitations as a defense, the debt buyer wins regardless. A default judgment then gives them the power to garnish wages and freeze accounts on a debt that was legally unenforceable the day they filed. The protection exists. It just does not work unless you use it.

If you receive a court summons about a debt, from any creditor, for any amount, you must respond by the deadline on the summons. That deadline is typically between 14 and 35 days depending on your state. If you think the debt might be time-barred, that is your defense to raise in your written response to the court. Ignoring the summons is not a strategy. It is how people end up with judgments against them on debts they did not legally owe. For more on how default judgments work and what collectors can do once they have one, read The Debt Collector Is Not Who You Think It Is.

The Clock Restart Traps Most People Fall Into

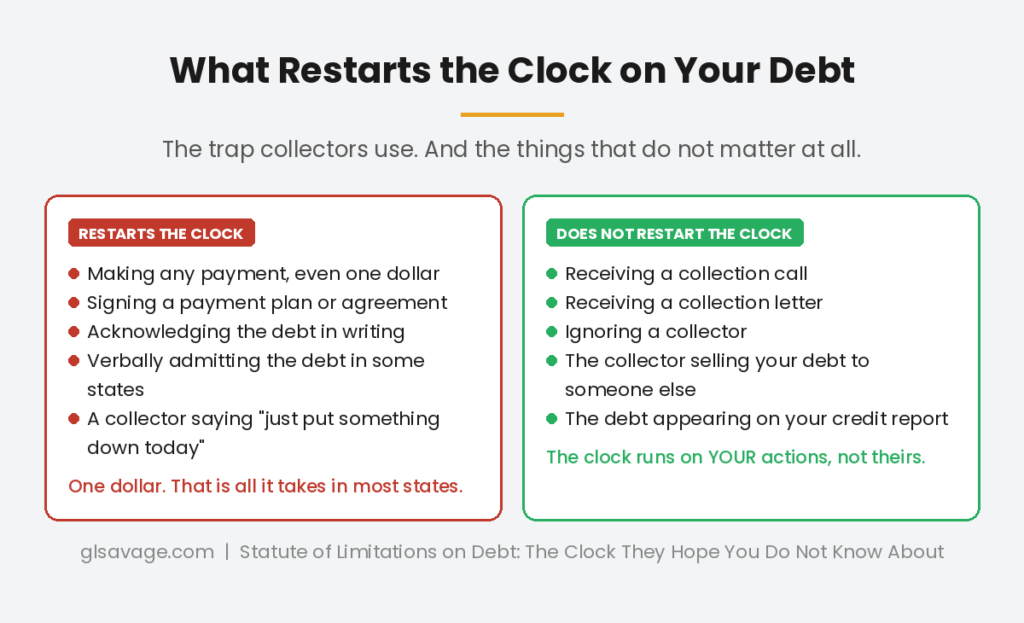

The statute of limitations clock can be reset. This is called reviving the debt. Once revived, the full limitation period starts over from the reset date, and a debt that was nearly or completely time-barred becomes legally enforceable again from scratch.

Making any payment restarts the clock in most states. Not the full balance, not a formal payment plan. One dollar. A single payment toward an old, time-barred debt can give the collector a fresh window to sue you for the entire remaining balance. This is exactly what collectors count on when they call and say something like “can you just put down something today to show good faith.” That payment does not show good faith. It resets the statute of limitations and hands the collector new legal standing.

Acknowledging the debt in writing restarts the clock in many states. Signing a payment agreement or responding in writing that you know you owe the debt can have the same effect as a payment. A verbal acknowledgment on the phone can restart the clock in some states as well, depending on state law.

What does not restart the clock: receiving a collection call or letter. A collector contacting you, even repeatedly, even aggressively, has no effect on the statute of limitations. The clock runs based on your actions, not theirs. You can receive a hundred calls from a collector without it changing the legal status of the debt by one day.

The practical rule: before you pay anything on an old debt, before you agree to anything in writing, before you acknowledge in any way that a debt is yours, find out when the statute of limitations in your state expires on that type of debt and when your last payment was made. Those two pieces of information tell you whether the clock has run out and whether any action on your part will restart it. If you are dealing with collectors calling about old accounts, How Collection Accounts Affect Your Credit Report covers what those accounts are doing to your credit in the meantime.

The Two Clocks People Confuse and Why It Matters

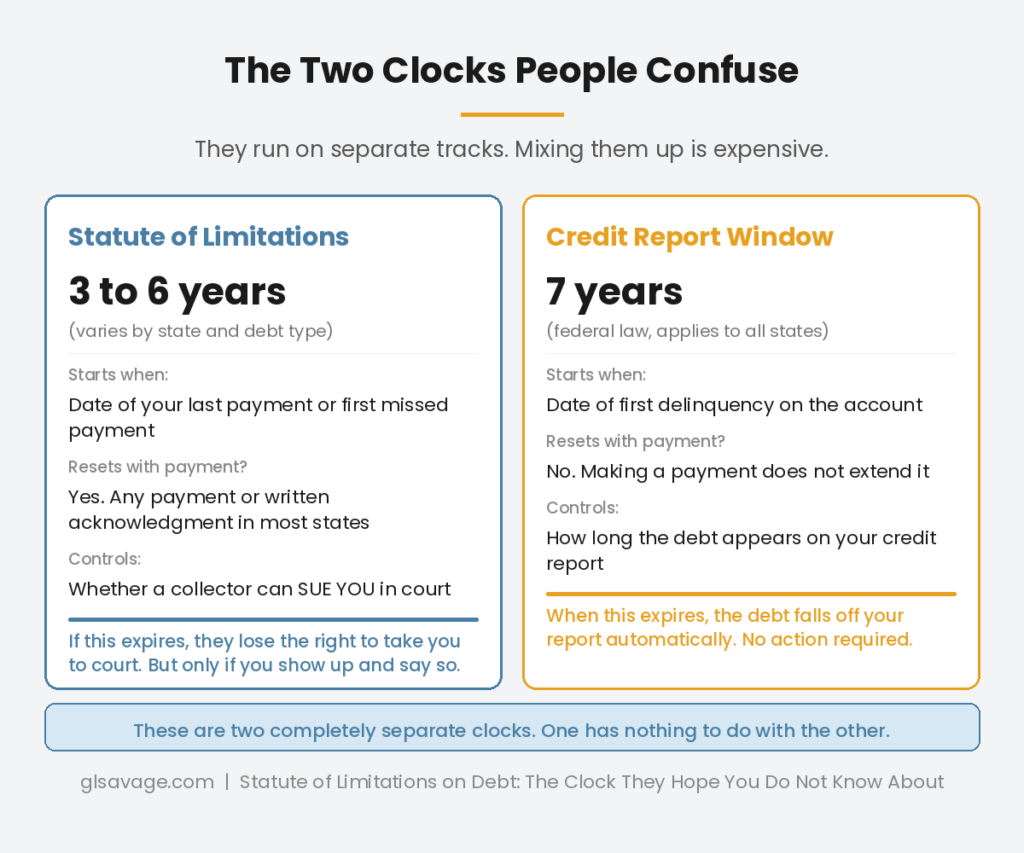

There are two separate legal timelines that govern old debt, and they have nothing to do with each other. Mixing them up is expensive.

The statute of limitations governs how long a collector can sue you in court. It typically runs three to six years depending on your state and debt type. Once it expires, they lose the right to sue.

The credit reporting window governs how long a debt can appear on your credit report. Under federal law, most negative items stay on your credit report for seven years from the date of first delinquency. This is a completely separate timeline from the statute of limitations. It does not reset when you make a payment. It does not affect whether a collector can sue you. It runs independently from everything else.

A debt can be time-barred, meaning past the statute of limitations, and still be on your credit report. A debt can be off your credit report entirely and still be within the statute of limitations. The two clocks run on different tracks and expire at different times. Understanding which clock you are on changes what your options are. Paying off a time-barred debt to clear your credit report may also restart the statute of limitations, giving the collector fresh legal standing just as the debt was about to leave your report on its own.

The Choice of Law Trap in Your Credit Card Agreement

The statute of limitations that applies to your credit card debt may not be the one for the state you live in, and your credit card agreement is likely the reason.

Your credit card agreement almost certainly contains a clause buried near the bottom specifying which state’s laws govern any dispute between you and the card issuer. This is called a choice of law clause. It means the clock on your debt may belong to a state you have never lived in.

Many major credit card issuers are incorporated in Delaware, which has a three-year statute of limitations on credit card debt. If your agreement designates Delaware law, that may be the clock that governs your debt regardless of where you live. Whether that clause will be honored depends on which court hears the case, the specific laws of your state, and how the judge interprets the agreement. Collectors know this and file in jurisdictions most favorable to them.

The practical step: if you are dealing with old credit card debt and trying to determine whether the statute of limitations has run out, pull out the original card agreement or look it up on the CFPB’s credit card agreement database at consumerfinance.gov. Look for a choice of law or governing law clause. If the agreement designates a specific state, look up that state’s statute of limitations on credit card debt alongside your own state’s, and consider consulting a consumer law attorney if you are close to the line.

What Collectors Can and Cannot Do After the Clock Runs Out

Once the statute of limitations expires, a collector loses the legal right to sue you for the debt. They cannot threaten to sue you either. Doing so is an explicit violation of the Fair Debt Collection Practices Act, which prohibits threatening legal action a collector does not actually have the right to take.

What they can still do: contact you. In most states, collectors can still call, write, and attempt to collect on time-barred debt as long as they do not threaten legal action. A smaller number of states prohibit contact on time-barred debt entirely. Either way, if calls become harassing or the collector threatens a lawsuit on a time-barred debt, that is a documented FDCPA violation you can sue over. If you win, you collect actual damages plus up to $1,000 in statutory damages plus attorney’s fees.

What they sometimes do anyway: file the lawsuit and hope for a default judgment. This is illegal when the debt is time-barred. It is also common. When you raise the statute of limitations as a defense in court, the case must be dismissed. The problem is that this only works if you raise it. Most people do not respond at all, which is exactly what the collector is counting on.

If you send a cease contact letter by certified mail, collectors must stop contacting you. After receiving it, they can only contact you one final time to confirm they are stopping or to notify you of specific legal action they intend to take. That letter does not erase the debt and does not prevent a lawsuit, but it stops the ongoing calls. If you think a collector has sued you on a time-barred debt, do not ignore the summons. Respond, raise the statute of limitations, and if you cannot afford an attorney, look for legal aid organizations in your area or consumer rights attorneys who take these cases on contingency.

How to Find Out Where You Stand

Figuring out whether the statute of limitations has run out on a specific debt requires three pieces of information: the type of debt, the state whose law governs it, and the date of your last payment or the date the account first went delinquent.

Pull your credit reports at AnnualCreditReport.com. All three bureaus are required to give you a free report. Your credit report will show the date of first delinquency for each account, which is the starting point for the statute of limitations in most states.

Look up your state’s statute of limitations for the specific type of debt: credit card, personal loan, medical debt, auto loan. These are different categories that may carry different limitation periods even within the same state. Your state attorney general’s website is a reliable source, as is the CFPB at consumerfinance.gov.

Check the agreement for a choice of law clause if the debt is a credit card. If the agreement designates another state’s laws, look up that state’s limitation period as well.

If a collector contacts you about a debt that may be time-barred, do not acknowledge the debt, do not make any payment, and do not sign anything before you know where you stand. Ask the collector in writing for debt validation under the FDCPA. They must provide the original creditor’s name, the amount owed, and written confirmation of your right to dispute the debt. That information will help you trace the date of delinquency and determine which clock is running. For more on using debt validation to protect yourself, read The Debt Collector Is Not Who You Think It Is.

Frequently Asked Questions

How long does a debt collector have to sue me?

Most states set the statute of limitations on debt between three and six years. Some states allow longer. The clock typically starts from your last payment or the date the account first went delinquent. Federal student loans have no statute of limitations. Court judgments already entered against you have their own separate window, often ten years or longer, and can often be renewed. Check your state’s specific rules for the type of debt you have.

What happens when the statute of limitations expires on a debt?

The debt still exists and you still technically owe it. The collector loses the legal right to sue you to collect it. They can still contact you and attempt to collect in most states, but they cannot threaten or file a lawsuit. If they file a lawsuit anyway, you must show up in court and raise the statute of limitations as a defense. If you do not respond to the lawsuit, the court will enter a default judgment against you regardless of whether the debt is time-barred.

Can I still be sued for a time-barred debt?

Yes. Suing on a time-barred debt is illegal under the FDCPA, but collectors do it and win when the defendant does not show up. The statute of limitations is an affirmative defense, which means you must raise it in court. A default judgment entered because you did not respond can lead to wage garnishment and frozen bank accounts even if the debt was legally unenforceable. Respond to every lawsuit.

Does making a payment restart the statute of limitations?

In most states, yes. A single partial payment can reset the clock and give the collector a fresh window to sue for the full balance. In many states, acknowledging the debt in writing can have the same effect. Receiving collection calls or letters does not restart the clock. Your actions restart it, not the collector’s.

How is the statute of limitations different from the seven-year credit report window?

They are completely separate. The statute of limitations governs how long a collector can sue you, typically three to six years depending on state and debt type. The seven-year credit reporting window is a federal rule governing how long most negative items stay on your credit report from the date of first delinquency. One has nothing to do with the other. A debt can be time-barred and still on your credit report. A debt can be off your report entirely and still within the statute of limitations.

What state’s statute of limitations applies to my credit card debt?

It may not be the state you live in. Many credit card agreements contain a choice of law clause designating a specific state’s laws for any disputes. If your card agreement designates Delaware or another state, that state’s limitation period may apply to your debt regardless of where you live. Check your original card agreement for a governing law or choice of law clause. The CFPB maintains a database of credit card agreements at consumerfinance.gov where you can look up the agreement for most major card issuers.

Can a debt collector contact me about a time-barred debt?

In most states, yes. Collectors can still call and write about time-barred debt as long as they do not threaten a lawsuit. A smaller number of states prohibit contact on time-barred debt entirely. If a collector threatens to sue you on a time-barred debt, that is an FDCPA violation. Document it, send a cease contact letter, and consult a consumer rights attorney. Many handle FDCPA cases on contingency, meaning you pay nothing unless you win.

What is zombie debt?

Zombie debt is old, time-barred, or otherwise uncollectable debt that collectors try to revive. They purchase these accounts for a fraction of a penny on the dollar specifically because they are nearly worthless, then contact people hoping fear or confusion produces a payment. Even a small payment can restart the statute of limitations in most states, turning legally dead debt back into something they can sue you over. Before paying anything on an old debt, determine whether the statute of limitations has already run out. If it has, that payment could cost you far more than the original balance.

If minimum payments on current debt are part of why old accounts went delinquent in the first place, Minimum Payments Keep You in Debt. That Is Not an Accident. explains the math behind why those payments were designed the way they were. And if you want to understand how the debt collection system operates from the beginning, The Debt Collector Is Not Who You Think It Is covers the full picture of who is actually calling and what power they really have. The statute of limitations on debt is a real legal protection. Using it starts with knowing it exists.