When money gets tight, one piece of advice shows up almost immediately: get a second job. It is treated like the obvious adult answer. Work more, earn more, problem solved. That advice is built on a fantasy version of the math, and the people who repeat it are almost never the ones who have to run it. A second job that pays $15 an hour sounds clear. But the moment you add the transportation, the taxes, the childcare, the benefits you quietly lose, the sleep you stop getting, and the spending that only happens because your schedule is now too compressed to do anything the cheaper way, the math looks very different from the posted wage. For some people running this honestly, the number that survives is smaller than expected. For some, it is negative. Here is what the slogan version leaves out.

The Hourly Wage Is the Marketing Number, Not the Real One

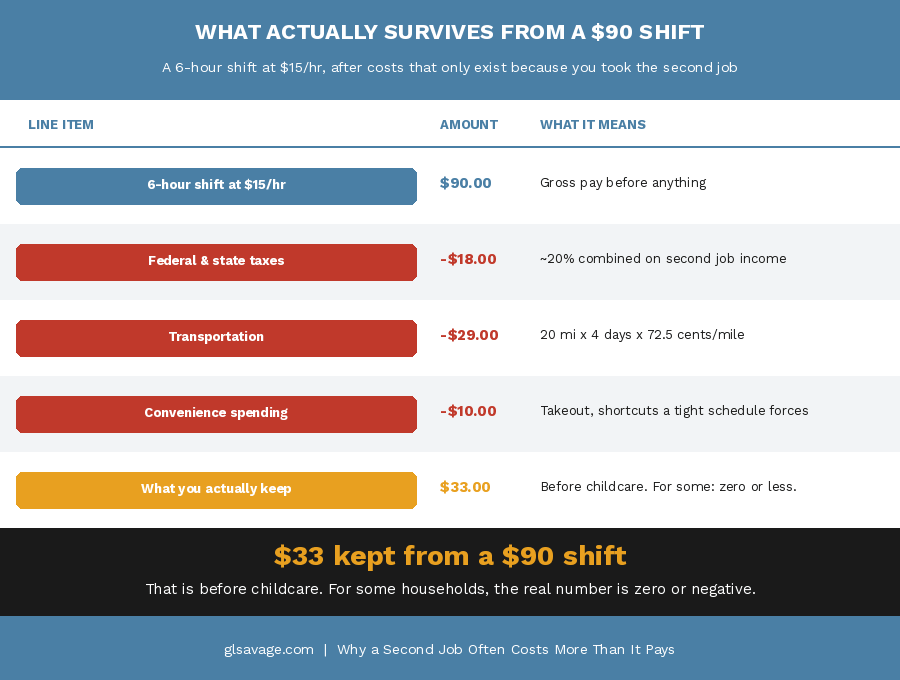

A second job that posts $15 an hour is not offering you $15 an hour. It is offering you $15 an hour before every cost that exists only because you are working that job gets subtracted from it. Transportation. Meals you cannot cook because the shift runs through dinner. Wear on your car. None of that appears in the listing. The IRS standard mileage rate for 2026 is 72.5 cents per mile, not because the government is being generous but because that is what it actually costs to operate a vehicle when you factor in fuel, maintenance, tire wear, and depreciation. If the second job adds 20 miles round trip four times a week, that is roughly $58 a week in vehicle costs before anything else takes a cut. On a $15-an-hour job, a six-hour shift earns $90 before taxes. Subtract $58 for transportation and you are already down to $32 before taxes, before childcare, before anything else. That is the math most second job advice skips entirely.

Taxes Do Not Care That It Is Your Extra Job

A second job is still income. It gets taxed the same way everything else does, and multiple-job withholding is one of the most reliable ways people end up surprised in April. Here is why it happens. Each employer withholds taxes based on what that job looks like in isolation, as if it were your only source of income. Neither employer knows about the other. When you file, all the income from both jobs gets added together, and your actual tax liability is based on the combined total, which may land in a higher bracket than either job alone would have suggested. The result is a gap between what was withheld during the year and what you actually owe. A job that felt like relief in July can produce a tax bill in April. The fix is straightforward but nobody does it automatically for you. When you start the second job, use the IRS Tax Withholding Estimator at irs.gov/individuals/tax-withholding-estimator before your first paycheck. It runs the full picture of both incomes and tells you exactly what to enter on Line 4(c) of your W-4 to cover the gap. Enter that number on the W-4 for your highest-paying job. If you wait until April to find out the withholding was off, the money has already been spent and the bill is real.

Child Care Can Erase the Entire Point in a Single Calculation

If taking a second job requires someone else to watch your child, the math can collapse immediately. The shift is not competing with transportation and taxes alone. It is competing with babysitting, extended daycare hours, weekend care, or whatever arrangement fills the gap the second job creates. Average childcare costs in the United States run between $200 and $400 a week depending on location and type of care. A part-time second job earning $200 a week has already broken even before a single other cost is counted. And even in cases where the second job does produce some net income, it can trigger a separate problem: higher earnings can change eligibility or copays for childcare assistance. That means you earn more and the subsidy that made working possible shrinks at the same time. The gain gets eaten before it can do anything.

The Benefit Cliff: The Part Nobody Warned You About

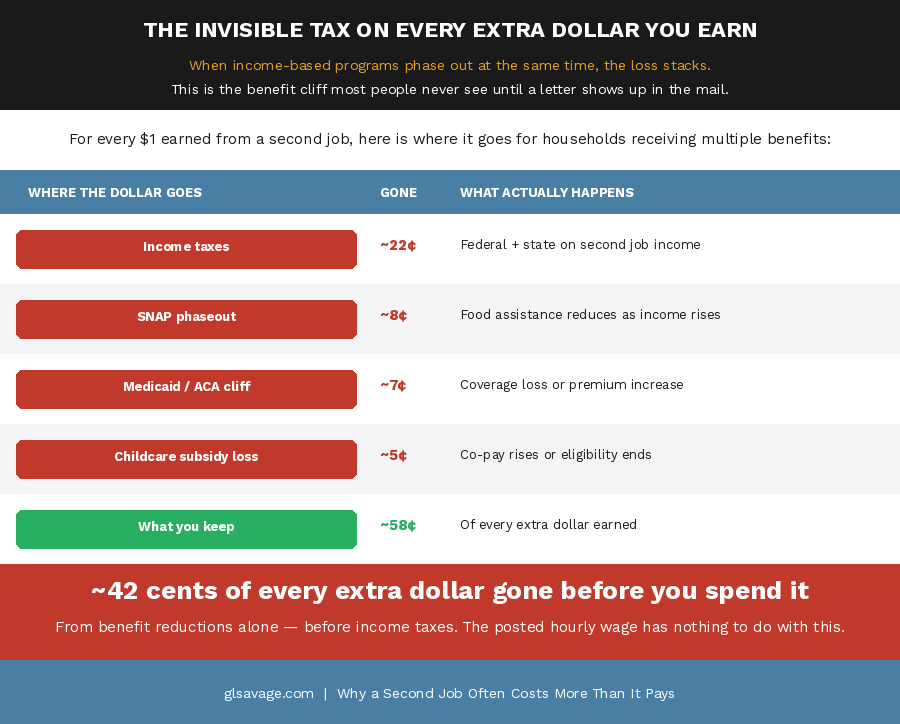

This is the curtain most people deserve to see before they take any job that raises their income, and it almost never gets discussed plainly. A significant portion of people who are working and financially stretched are also receiving some combination of SNAP, Medicaid, ACA Marketplace premium tax credits, childcare subsidies, or other income-based assistance. Those programs phase out or cut off as income rises. When a second job pushes income over a threshold, the benefits reduction starts. Sometimes gradually. Sometimes all at once. Either way, the effective cost of earning that extra money becomes much higher than the tax rate alone would suggest.

Researchers call the worst version of this a benefit cliff: a point where earning one more dollar triggers a loss of benefits that exceeds the dollar gained. The stacking effect makes this worse. Households receiving multiple programs simultaneously face steeper effective rates as the phaseout from each individual program stacks on top of the others. Think of it as an invisible tax on every extra dollar you earn, not from the IRS, but from the benefit programs themselves reducing what they send you. Research has found that approximately 3 million households receiving SNAP, EITC, Child Tax Credits, and Medicaid together face a median rate of 42 percent from benefit reductions alone, before income taxes. Add actual income taxes on top of that and the effective rate on additional earnings can exceed 60 or 70 percent for some households. The posted hourly wage has almost nothing to do with what you actually keep.

The Atlanta Federal Reserve has built a free suite of tools called CLIFF, which stands for Career Ladder Identifier and Financial Forecaster, specifically to model this problem. The tools show exactly where your benefit thresholds are and what income level would actually improve your overall financial position. Demo versions of the CLIFF Snapshot and Dashboard are publicly viewable at atlantafed.org/cliff-tool. Several states have also launched their own public versions through local workforce agencies, including Florida, Colorado, Arizona, and others, so searching for a CLIFF benefits cliff calculator in your state may find you a tool you can use directly. If you receive any income-based benefits, understanding where your cliffs are before taking a second job is not optional math. It is the math.

The Checking Account Trap Nobody Mentions at the Interview

Many second jobs, particularly retail and service positions, do not offer the same direct deposit timing as a primary employer. Pay schedules differ. Some smaller employers pay by check rather than direct deposit. If your primary job’s deposit lands on a different schedule than your second job’s paycheck, you may find yourself in a timing gap where you have earned the money but it has not cleared yet. This is how small overdrafts happen in households that are otherwise managing carefully. The second paycheck is in transit. A bill hits. A $35 overdraft fee erases a shift’s worth of net earnings instantly. It is not irresponsibility. It is schedule friction created by operating across two employers with different payment systems. Building a one-week cash buffer before the job starts is the cleanest way to avoid it, though that advice is easy to give and hard to act on when the reason you are taking the second job is that there is no buffer. How Banks Make Money From Overdraft Fees and Everything Else They Are Not Telling You explains exactly how banks profit from that moment, which is worth understanding before it happens to you.

The Schedule Damage Is Bigger Than the Hours Suggest

A four-hour shift is never really four hours. It is getting ready, commuting there, working, commuting back, and then trying to reassemble the rest of your life around the gap it created. If the shift falls at night or on weekends, it cuts into the time that recovery, family, errands, and cooking used to occupy. Those things do not stop needing to happen. They get compressed or they get expensive. Research consistently links long work hours and irregular shift schedules to shorter sleep, poorer sleep quality, and reduced cognitive performance the following day. That cost does not appear on a pay stub. But when the primary job takes the hit because the second job is depleting recovery time, the stakes are much higher. The primary job is the one carrying health insurance, seniority, and most of the income. Protecting it matters more than the second job’s hourly rate in almost every comparison.

The Convenience Spending Nobody Counts Until the End of the Month

When schedules get compressed, people start buying time back. More takeout. More gas station food. More convenience purchases that would not happen if there were an extra two hours in the day to cook and plan. This is not a character flaw. It is what happens when structure tightens and the cheaper, slower options stop fitting the schedule. The extra spending belongs in the calculation. A household that adds $200 a month in food convenience spending because the second job eliminated cooking time has not kept $200 from that second job. It has paid it back out in a different form. The net position is worse than the paycheck suggests.

The Real Math: Run It Before You Say Yes

Before accepting any second job, run the honest version of the math. Not the hourly wage times the hours. The actual number. Start with the gross weekly pay. Subtract estimated taxes using the IRS withholding estimator to get a real number rather than a guess. Subtract transportation costs at the full IRS mileage rate of 72.5 cents per mile, not just fuel. Subtract childcare if it applies. Check your current benefits situation and find out whether the added income reduces anything you currently receive. Estimate the additional convenience spending the schedule change will create. What is left is the actual value of the second job. For many people running this math honestly, the number that survives is smaller than expected. For some, it is negative. That is not a reason to give up. It is information. Information that points toward where to look instead.

What Usually Works Better Than a Random Second Job

The goal is more net money with less damage to everything else in your life. A second job at a random employer is often the most expensive way to get it, and it rarely gets compared honestly against the alternatives.

Overtime or additional hours at the primary job, when available, is almost always the better choice. No commute. No second employer relationship to manage. No tax withholding complication from a new W-4. No schedule conflict. The same skills, the same location, potentially time-and-a-half pay. It also just got more attractive: the tax legislation passed in July 2025 introduced a deduction of up to $12,500 for overtime pay for individual filers, which means overtime income is now taxed at a lower effective rate than a second job’s income is. If your primary employer offers overtime, this is the first question to ask before looking anywhere else.

Selling a skill directly, without a fixed employer, is the second option worth a serious look. A skill that earns $20 an hour at a second job earns $20 an hour. The same skill offered as freelance work, tutoring, repair, bookkeeping, photography, or any other direct service can price itself based on value rather than what an employer decides to offer, with no commute requirement and schedule flexibility that protects the primary job. The income is taxed as self-employment, meaning you pay both the employee and employer share of Social Security and Medicare taxes yourself, roughly 15 percent on top of regular income tax. Quarterly estimated payments are required. But the net economics are often better than a W-2 second job even after accounting for that.

Fixing withholding at the primary job is one of the most overlooked ways to put more money in each paycheck without working a single additional hour. If your primary job is over-withholding, a corrected W-4 produces immediate results. This is not a loan or a trick. It is your money that was being held until April. Run the IRS estimator, correct the W-4, and the increase shows up in the next paycheck.

Reducing one large recurring bill is often more efficient than earning more. Lowering a car insurance premium by $50 a month produces $600 a year in permanent after-tax income improvement. No commute, no schedule disruption, no benefits cliff exposure, no childcare arrangement. Car Insurance Is a Rigged Game. Here Is How to Play It. lays out exactly how to do that. The same logic applies to renegotiating a phone plan, refinancing high-rate debt, or accessing an assistance program you currently qualify for but are not using. These are not glamorous moves. But compared to a second job that nets $80 a week after costs, finding $80 a month in existing expenses is often the cleaner path.

If none of those work fast enough, understanding what is actually driving the gap matters. The Poverty Premium Explained: How to Fight Back covers why the same dollar goes further for some people than others, and where the real structural levers are.

If You Do Need a Second Job, Structure It to Limit the Damage

Sometimes the answer really is a second job. The emergency is real, the timeline is short, and the other options are not available. In that case, the goal is to minimize collateral damage while using it. Look for work that can be done remotely, on your own schedule, or in blocks that protect your primary job’s recovery time. Delivery work, remote customer service, freelance writing, and data entry are all structurally less damaging than a standard second shift job with a fixed commute. Update your W-4 before the first paycheck, not after. Set a specific end date or income target rather than an open-ended commitment. And check your benefit situation before you start so you know where the cliffs are and can plan around them instead of being surprised by a letter in the mail.

A Second Job Is Not a Character Test. It Is a Financial Decision.

People who take second jobs are not doing something wrong. They are responding rationally to a situation where income does not cover expenses. The advice to get a second job is not wrong in principle either. It just gets delivered without the full picture, by people who are not going to be the ones managing the transportation, the taxes, the childcare, the sleep debt, or the benefits letter. The full picture is what you just read. The decision is still yours. But at least now it is actually a decision.

Frequently Asked Questions About Second Job Costs

Is getting a second job worth it financially?

Sometimes, but only after running the real math. A second job can make sense for a short-term gap or a specific savings target, but once you subtract taxes at the combined income rate, transportation at the full IRS mileage cost of 72.5 cents per mile, any childcare required, potential benefit reductions, and the convenience spending that tight schedules create, the net gain is often much smaller than the posted wage suggests. For some households in specific benefit situations, taking a second job that pushes income over a program threshold can actually reduce overall financial position. Run the numbers specifically before committing.

Why does a second job cause tax problems?

Each employer withholds taxes based on that job alone, as if it were your only income. When both incomes are combined at filing time, the total may fall in a higher tax bracket than either job individually, creating a gap between what was withheld and what is actually owed. The fix is to use the IRS Tax Withholding Estimator at irs.gov/individuals/tax-withholding-estimator when starting the second job and enter the recommended additional amount on Line 4(c) of your W-4 for the highest-paying job. Do this before the first paycheck.

Can a second job cause you to lose benefits like SNAP or Medicaid?

Yes. Extra income can reduce or eliminate eligibility for SNAP, Medicaid, ACA premium tax credits, childcare subsidies, and other income-based programs. In the worst cases, the loss of benefits can exceed the earnings gained, a situation called a benefit cliff. Research has found that households receiving multiple programs simultaneously can face a combined reduction rate of 42 percent or more from benefit losses alone, before income taxes, meaning 42 cents of every extra dollar earned disappears before the IRS takes its share. The Atlanta Fed’s CLIFF tool, accessible through partner organizations at atlantafed.org/cliff-tool, can model your specific situation and show exactly where your thresholds are.

How do I calculate the real cost of a second job commute?

Use the IRS standard mileage rate, which is 72.5 cents per mile for 2026, not just the cost of gas. That rate reflects the full cost of driving including fuel, oil, tire wear, maintenance, and depreciation. Multiply your round-trip miles by 72.5 cents, then multiply by the number of shifts per week to get a weekly transportation cost. Subtract that from the shift’s gross earnings before taxes to get a more honest starting number for the second job math.

What is a benefit cliff and how does it affect taking a second job?

A benefit cliff is the point at which earning more money triggers a loss of assistance that exceeds the gain. It happens because income-based programs like SNAP, Medicaid, childcare subsidies, and ACA tax credits all have income thresholds. When a second job pushes income over one of those lines, the benefit reduces or cuts off. When multiple programs phase out around the same income level, the combined reduction can be larger than the raise itself. Many people do not know their income is close to a cliff until they receive a letter notifying them of a benefit change they did not anticipate.

What are better alternatives to getting a second job?

The most effective alternatives share one feature: they produce net income with less collateral damage than a second employer. Overtime at the primary job eliminates the commute, the new W-4 complication, and the schedule fragmentation. Freelance or direct service work using an existing skill can price higher than an employer would offer and allows schedule flexibility. Correcting over-withholding at the primary job puts money in every paycheck immediately with no extra hours worked. Reducing one major recurring bill creates permanent after-tax savings without any of the second job’s side costs. Accessing an assistance program you currently qualify for but are not using reduces the need for the extra income in the first place.

Does a second job affect your performance at your main job?

Research consistently links irregular schedules and extended work hours to shorter and lower-quality sleep, which affects concentration, memory, reaction time, and mood the following day. The primary job is almost always the higher-value one, carrying more income, benefits, seniority, and long-term stability. If a second job is degrading performance at the primary job, the financial risk is much larger than the second job’s hourly rate. Structuring a second income source around schedule flexibility, rather than a fixed shift at a second employer, is one way to reduce this risk.

How do I fill out a W-4 correctly when I have two jobs?

Use the IRS Tax Withholding Estimator at irs.gov/individuals/tax-withholding-estimator with the income from both jobs entered. The estimator will calculate how much additional withholding is needed to cover the combined tax liability and tell you the specific dollar amount to enter on Line 4(c) of your W-4. Enter that amount on the W-4 for your highest-paying job and leave the other W-4 at its standard setting. Do this before your first paycheck from the second job, not at tax time. The estimator does not collect or store personal information.

Can I make extra money without getting a second job?

Yes, and for many people the net result is better than a second employer would offer. Options include overtime or additional shifts at the primary employer, freelance or gig work using an existing skill on a flexible schedule, renegotiating or reducing a major recurring bill, correcting tax over-withholding to increase take-home pay immediately, or accessing income-based assistance programs that reduce expenses without adding income. None of these are guaranteed or universal, but the comparison should be honest: a second job that nets $60 a week after all costs is not automatically better than a $60-a-month insurance savings that requires one phone call.