A bill you barely remember. A medical charge from two years ago. A utility account from an apartment you left. A credit card balance that slipped during a hard month. You did not think much of it at the time. Then you applied for something, a car loan, an apartment, a credit card, and the answer came back wrong. That is usually when people find out a collection account has been sitting on their credit report, sometimes for years, doing damage they did not know was happening. Understanding how collection accounts affect your credit report means understanding not just what the score does but why, and what your actual options are, which are more than most people realize.

What a Collection Account Actually Is

When you stop paying a bill, the original creditor waits. They send letters. They call. They try internally for several months, sometimes up to 180 days. When that fails, one of two things happens: they hand the account to an in-house or third-party collection department, or they sell the debt outright to a debt buyer.

Here is the part the industry does not explain clearly. When a debt is sold, the buyer pays pennies on the dollar for it. A $1,500 debt might sell for $75 or $100. The collection agency’s entire business model depends on collecting more than they paid. That is why the contact is aggressive from the moment it starts. It is not personal. It is math. They bought a discounted asset and need to convert it into profit.

Once a collection agency takes over, a new entry typically appears on your credit report under their name. The original account may still be there too, marked as a charge-off, which means the original creditor wrote it off as a loss. That is why the same debt can show up twice on your report as two separate negative entries. Both tied to the same failure to pay. Both affecting your score. This is one of the more confusing parts of how collection accounts affect your credit report and most people do not realize it until they pull their file.

Why the Credit System Treats Collections So Harshly

Credit scoring models are built to measure one thing: how likely you are to repay future debt. Every entry on your report is a data point in that calculation.

A collection account sends a specific signal. It tells the system that a previous creditor waited months for payment, gave up, and sold the debt to someone whose entire job is recovering money people stopped paying. From the model’s perspective, that is one of the strongest risk signals available. It does not matter that the original debt was $200. The signal is the same.

Payment history is the largest single factor in most credit scores, at roughly 35 percent. Collection accounts sit directly inside that category. This is fundamentally how collection accounts affect your credit report: they land inside the biggest factor the scoring model tracks, and once one appears, the score can drop sharply. How much depends on what the rest of the file looks like. Someone with a thick file and years of clean history absorbs the hit differently than someone with a thin file and not much else to offset it. But the direction is always the same and it is never up.

For people with strong scores, a single collection can pull the number down 50 to 100 points or more. That is the difference between qualifying for a loan and not qualifying. Between a reasonable interest rate and a punishing one. Between getting the apartment and being told to look elsewhere.

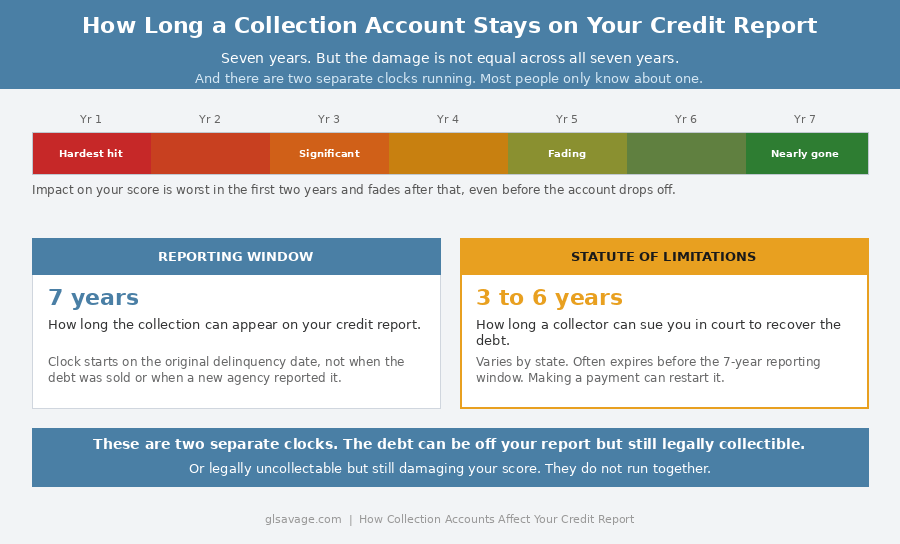

How Long Collection Accounts Stay on Your Credit Report

Seven years. The clock starts from the original delinquency date with the original creditor, not from when the collection agency reported it, not from when the debt was sold, not from the last time anyone contacted you about it.

That distinction matters more than most people know. Collectors sometimes imply that the timeline resets when they acquire the debt or when you make contact. It does not. The seven-year window is anchored to the moment the account first went seriously delinquent with the original creditor. The debt can change hands ten times and that original date stays fixed.

There is also a difference between the reporting window and the statute of limitations on legal action. The reporting window is how long the collection can appear on your credit report. The statute of limitations is how long a collector can sue you to recover the debt. These are two separate clocks and they do not run together. In most states the statute of limitations is three to six years, which means a collector may lose the legal right to sue you before the account drops off your report. This matters in one specific and important situation covered below.

The damage is worst early and fades as the account gets older. That is worth understanding about how collection accounts affect your credit report over time: a collection from six years ago carries less weight than one from six months ago, assuming the rest of the file has improved. The impact decreases even before the account drops off entirely.

What Paying a Collection Actually Does

This is where most people get misled, and the answer is more complicated than most articles make it.

Paying a collection account does not automatically remove it from your credit report. The status changes from unpaid to paid. The entry stays until the seven-year window closes. That is the default outcome if you simply pay without negotiating anything first.

Whether paying helps your score depends entirely on which scoring model the lender is using. FICO 9 and FICO 10 ignore paid collections entirely. VantageScore 3.0 and 4.0 also treat paid collections more favorably. But many lenders, especially mortgage lenders, still use older scoring models that treat paid and unpaid collections the same way. You could pay the debt, see no score improvement, and still have the entry sitting on your report for years. This is not explained clearly anywhere in the collection process and it costs people real money.

The exception is pay-for-delete. Some collection agencies will agree in writing to remove the account from your credit report entirely in exchange for payment. Not every agency offers this. Not every agency that agrees to it actually follows through. Which is why the agreement must be in writing, specifically stating they will request deletion from all three bureaus, before any money changes hands. A verbal agreement in debt collection is worth nothing. If they will not put it in writing, do not pay.

Zombie Debt: The Clock That Collectors Hope You Do Not Know Is Running

Zombie debt is old debt that collectors attempt to resurrect after the statute of limitations on legal action has expired. They buy portfolios of aged, uncollectable debts for almost nothing and contact people hoping they will pay voluntarily or, critically, do something that restarts the clock.

In many states, making a payment on an old debt, even a small one, can restart the statute of limitations and give the collector the legal right to sue you again. The same can happen if you make a written promise to pay. You do not need to sign a new agreement. In some states, simply acknowledging the debt in writing is enough.

This is why the advice to pay old debts without thinking it through can backfire badly. If a collector contacts you about a debt you do not remember or that seems very old, find out when the original delinquency date was before you do anything. If the statute of limitations has expired, you may have no legal obligation to pay and paying could create a new one. Check your state’s statute of limitations on debt. It varies significantly.

Zombie debt also sometimes reappears on credit reports illegally. Some collection agencies re-report old accounts as new debts to make them appear more recent and extend the damage. This is called re-aging and it violates the Fair Credit Reporting Act. If you see a collection account on your report with a date that does not match the original delinquency, dispute it immediately with the bureau and file a complaint with the CFPB at consumerfinance.gov/complaint.

Medical Debt and Your Credit Report Right Now

Medical debt has been in legal and regulatory flux and the current status is important to get right because it has changed significantly in 2025.

The three major credit bureaus, Equifax, Experian, and TransUnion, voluntarily stopped reporting paid medical collections in 2022 and stopped reporting medical collections under $500 in 2023. Those changes are still in effect and came from the bureaus directly, not from a government rule.

The CFPB finalized a broader rule in January 2025 that would have removed all medical debt from credit reports entirely. In July 2025, a federal judge blocked that rule, ruling that the CFPB exceeded its authority under the Fair Credit Reporting Act. The rule is not currently in effect.

What this means practically: paid medical collections are still being excluded by the bureaus voluntarily, and medical debt under $500 is still excluded. But unpaid medical debt over $500 can still appear on your credit report. If you have medical collections on your report, check each entry carefully against these thresholds. Paid medical collections and those under $500 should not be there. If they are, dispute them.

When a Collection Account on Your Report Is Wrong

Collection accounts are not always accurate, and this is one of the most important things to know about how collection accounts affect your credit report: inaccurate ones can often be removed. Debts get sold between agencies repeatedly. Records become incomplete. Account information gets attached to the wrong person. Balances get reported incorrectly. The original delinquency date gets mis-reported to make the account appear newer than it is.

The industry is not careful about this because the error is rarely their problem. It becomes yours.

When a collector contacts you, federal law gives you the right to request debt validation in writing within 30 days of first contact. Debt validation means documentation proving the debt is real, the amount is correct, the account belongs to you, and the agency has legal authority to collect it. Send the request by certified mail with return receipt. Keep the copy.

Here is what to write: “I am requesting written validation of this debt pursuant to the Fair Debt Collection Practices Act. Please provide the name of the original creditor, the original account number, the amount owed and how it was calculated, and documentation showing your authority to collect this debt. Until this debt is validated, please cease collection activities.”

If they cannot produce that documentation, they cannot legally continue collection efforts. The account can be disputed with the credit bureaus and removed. Disputing an inaccurate account is a process most people do not know exists, but the bureaus are required to investigate and remove accounts that cannot be verified. That step has cleared legitimate-looking collection accounts off people’s reports that had no business being there.

Disputes should be submitted in writing by certified mail, not just through the online portal. The online portal is convenient for the bureaus because automated systems cost less than human reviews. A written dispute creates a paper trail that is harder to dismiss. Include copies of any documentation that supports your case. The bureau has 30 days to respond.

Here is what to write to the bureau: “I am disputing the following account on my credit report: [creditor name, account number]. This account is inaccurate because [state the specific reason: not mine, incorrect balance, wrong date, already paid, past reporting window, etc.]. I am requesting that this account be investigated and removed from my credit report. I have enclosed [list any supporting documents]. Please provide written confirmation of the results of your investigation.”

Understanding the full picture of how credit scores work is useful here because collections do not exist in isolation. The same file that has a collection on it also has utilization, payment history on other accounts, and account age all working together.

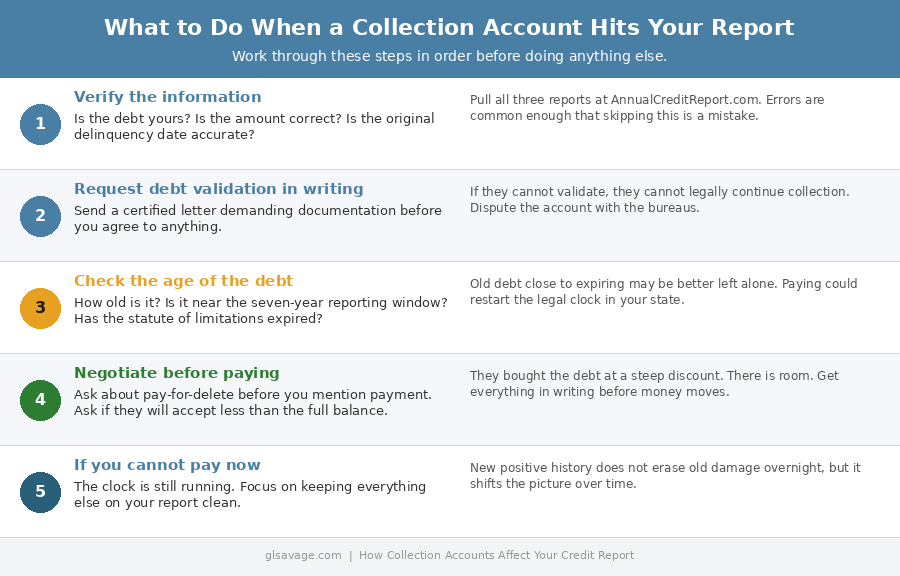

The Playbook When a Collection Account Hits Your Report

When a collection account shows up on your report, work through it in this order before doing anything else.

Verify the information first. Check that the debt is actually yours, the amount is correct, and the original delinquency date is accurate. Errors are common enough that skipping this step is a mistake. Pull your free reports at AnnualCreditReport.com.

Request validation from the collector before agreeing to anything. Do it in writing by certified mail. Use the language above. If they cannot validate, dispute the account with all three bureaus.

Check the age of the debt. If it is approaching the end of the seven-year reporting window, the tradeoff of paying may not be worth it, especially if paying could restart the statute of limitations for legal action in your state. Old debt close to expiring from the report is often better left alone.

If the debt is valid and recent enough to matter, negotiate before paying anything. Ask whether the agency will accept less than the full balance. They bought the debt at a steep discount. There is room. Ask specifically about pay-for-delete before mentioning payment. Once they know you will pay, your leverage drops. Get any settlement agreement in writing before money moves.

If you cannot pay anything right now, understand that the clock is still running. The account will age off. Focus on keeping everything else on your report clean. New positive history does not erase old damage overnight, but it shifts the overall picture over time. Understanding how minimum payments keep you in debt is relevant here too. The same financial pressure that produces collections also keeps people trapped in revolving balances, and both problems come from the same system.

If the debt is overwhelming and you have multiple collections, a nonprofit credit counselor can help you see the full picture before you make decisions that cannot be undone. The National Foundation for Credit Counseling at nfcc.org is the place to start. Not a debt settlement company. A nonprofit. The difference between those two options costs people serious money and the confusion between them is not accidental.

What the System Is Built to Count On

Collection accounts affect your credit report with disproportionate force relative to the original debt because the system was not designed to be proportionate. It was designed to measure risk for lenders. A $200 unpaid bill signals the same behavioral pattern as a $2,000 one. The score does not know why you did not pay. It does not know if it was a billing error, a medical emergency, or a month where the math did not work. It registers the outcome and applies the penalty. The poverty premium works in credit just as it does everywhere else: the less financial cushion you have, the more the system costs you when something slips.

The collection industry counts on you not knowing your rights under the Fair Debt Collection Practices Act. It counts on you not knowing that debt validation is a federal right. It counts on you not knowing about zombie debt and re-aging. It counts on you paying immediately without asking about pay-for-delete, without checking whether the account is accurate, without checking how old the debt is or what paying it might trigger. A collection on your report does not just affect loan applications. It affects your car insurance rate in most states and can affect whether certain employers will hire you.

How collection accounts affect your credit report is a documented process with specific rules, specific timelines, and specific consumer protections. Most people find out about those protections after they have already made the expensive mistake of ignoring them. Now you know before that happens.

Frequently Asked Questions About How Collection Accounts Affect Your Credit Report

How much does a collection account lower your credit score?

For people with strong credit, a single collection account can drop their score 50 to 100 points or more. The higher the score going in, the steeper the drop. For someone with an already damaged file, the impact is smaller because the score has less room to fall. There is no single number because the model weighs the collection against everything else on the report.

How long do collection accounts stay on your credit report?

Seven years from the original delinquency date with the original creditor. Not from when the debt was sold. Not from when the collection agency first reported it. Not from the last payment. The clock is anchored to the moment the account first went seriously delinquent. The debt changing hands does not reset it.

Can the same debt appear twice on my credit report?

Yes. The original creditor may report a charge-off while the collection agency reports the account separately. Both entries can exist simultaneously and both affect the score. If the same debt appears under multiple collection agency names as if it is a new debt each time, that may be illegal re-aging and is worth disputing with the bureaus and reporting to the CFPB.

Does paying a collection account improve your credit score?

It depends on which scoring model the lender uses. FICO 9, FICO 10, and VantageScore 3.0 and 4.0 ignore paid collections or treat them more favorably. But many lenders still use older models that treat paid and unpaid collections the same. Paying does not guarantee a score improvement. Before paying any collection, ask about pay-for-delete. If the agency agrees in writing to remove the account entirely, paying makes sense. If they will not agree to that, paying may change nothing on your report.

What is pay-for-delete and does it work?

Pay-for-delete is a negotiation where you offer to pay the collection account in exchange for the agency removing it from your credit report entirely rather than just marking it paid. Not every agency will agree. Those that do must put it in writing specifically stating they will request deletion from all three bureaus before you send any money. A verbal agreement is worth nothing. Once you pay without that agreement, your leverage is gone and the entry stays.

What is debt validation and how do I request it?

Debt validation is your federal right under the Fair Debt Collection Practices Act to demand written documentation proving the debt is real, the amount is correct, the account is yours, and the agency has legal authority to collect it. Send the request by certified mail within 30 days of first contact. If they cannot validate the debt, they cannot legally continue collection efforts and the account can be disputed with the bureaus. Use the sample language provided in this article.

What is zombie debt?

Zombie debt is old debt, often past the statute of limitations for legal action, that collectors try to revive by contacting you and hoping you will pay voluntarily or do something that restarts the clock. In many states, making even a small payment on an old debt or acknowledging it in writing can restart the statute of limitations and give the collector the right to sue again. If a collector contacts you about a debt that seems very old, check the original delinquency date and your state’s statute of limitations before doing anything.

Does medical debt affect your credit report the same way?

Not exactly, under current rules. The three major bureaus voluntarily stopped reporting paid medical collections in 2022 and medical debt under $500 in 2023. Those voluntary exclusions are still in effect. The CFPB rule that would have removed all medical debt was blocked by a federal judge in July 2025. Unpaid medical debt over $500 can still appear on your credit report. If you have paid medical collections or medical collections under $500 on your report, they should not be there under current bureau guidelines. Dispute them.

Can I remove a collection account from my credit report?

Yes, in certain situations. If the information is inaccurate, dispute it and it must be removed. If the collector cannot validate the debt, dispute it and it must be removed. If you negotiate a pay-for-delete agreement in writing, it can be removed upon payment. If the seven-year reporting window has closed, it must come off regardless. The account does not have to stay just because it is there.

What should I do when a collector first contacts me?

Do not pay immediately. Request written debt validation within 30 days. Check the original delinquency date. Pull your credit reports to see how the account is being reported. If the debt is old, check the statute of limitations in your state before making any payment or written acknowledgment. If the debt is valid, recent, and significant enough to address, negotiate for pay-for-delete in writing before sending money.

What is re-aging and is it illegal?

Re-aging is when a collection agency reports an old account as if it were a new debt, extending how long it appears on your credit report beyond the legal seven-year window. It violates the Fair Credit Reporting Act. If you see a collection account on your report with a delinquency date that seems more recent than your records indicate, dispute it immediately with the bureau and file a complaint with the CFPB at consumerfinance.gov/complaint.