Three private companies you never chose, never agreed to work with, and have almost no leverage over are maintaining files on your financial behavior right now. Those files get turned into a number. That number determines whether you can rent an apartment, what interest rate you pay on a car, whether certain employers will hire you, and what you pay for insurance. You did not consent to this system. You were born into it. And the people who profit from it have a financial interest in keeping it as confusing as possible. This is credit scores explained, including the parts they count on you not knowing.

What the Credit Score System Actually Is and Who It Serves

A credit score is a number, usually between 300 and 850, built from data in your credit report. Most people think of it as a financial grade. That is not quite right. It is a product. FICO, the company behind the most widely used scoring model, sells its scores to lenders. The lenders are the customer. You are the subject. That distinction matters because the system was designed to serve lenders’ need to assess risk, not to help you understand your own financial picture or give you a fair path to rebuild after hardship.

Your credit report is maintained by three separate private companies: Equifax, Experian, and TransUnion. They are not government agencies. They are not regulated the way banks are. They collect data about you from lenders and sell access to that data. They each operate independently, which means your file at each bureau can be different, your scores from each can be different, and errors in one bureau’s file do not automatically get corrected at the others. This is the same basic structure as how banks make money from overdraft fees: a system built around your financial life that you did not design, did not choose, and largely cannot opt out of.

VantageScore is the other major scoring model, built by the three bureaus as a competitor to FICO. Different formula, same underlying data. Lenders choose which model to use. You usually do not know which one they pulled until after the decision is made. As of July 2025, Fannie Mae and Freddie Mac now permit lenders to use VantageScore 4.0 alongside FICO for conforming mortgage loans. That is a significant shift and most people applying for mortgages have no idea it happened.

Your credit report is not the same as your credit score. The report is the raw file. The score is calculated from it. You are entitled to one free report from each bureau every year at AnnualCreditReport.com. That is the official federally mandated site. Any other site offering free credit reports is either tied to a paid monitoring service or trying to capture your information for marketing purposes.

Credit Scores Explained: The Five Factors and What They Actually Mean

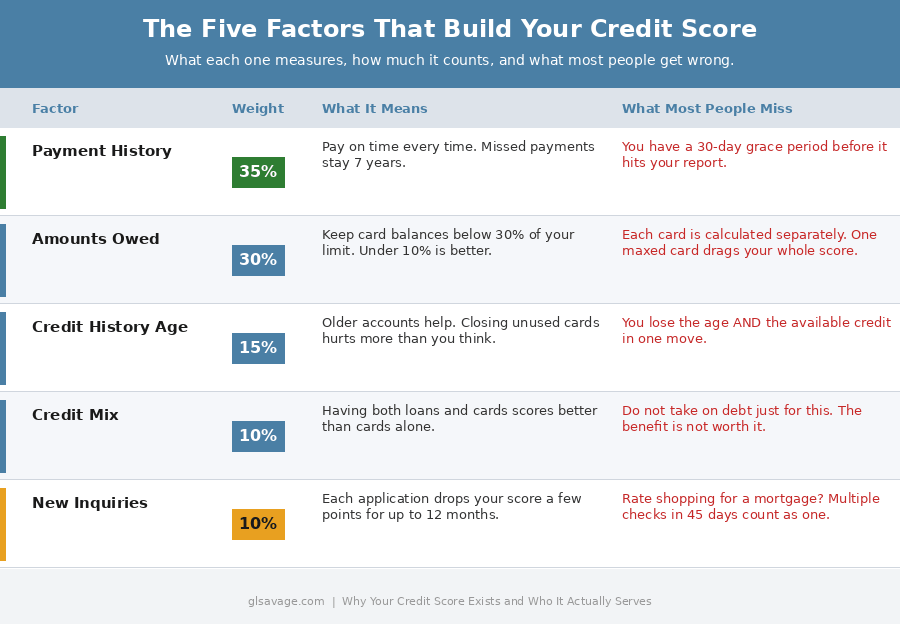

FICO breaks the score into five weighted categories. The industry presents these as a neutral, objective formula. They are not neutral. Each one reflects a value judgment about what kind of borrower is trustworthy, and some of those judgments actively work against people who never had the luxury of building credit early.

Payment history is 35 percent of your score. The single biggest factor. Pay on time, every time, and this part largely takes care of itself. Miss one and the damage can be significant, especially if your record was clean before. A payment is not reported as late until it is 30 days past due. If you missed a due date but catch it within that window, it does not appear on your report. After 30 days it does, and it stays for seven years. A miss from two years ago hurts less than one from last month, but neither disappears quickly.

Amounts owed is 30 percent. Specifically, how much of your available credit you are using at any given time. This is called your credit utilization ratio. A $500 balance on a $1,000 limit card is 50 percent utilization. Keep it below 30 percent. Under 10 percent scores even better. Utilization can move faster than any other factor. Pay down balances and your score responds at the next reporting cycle. Something most articles skip: utilization is calculated per card, not just overall. You can have a low average across all your cards, but if one card is nearly maxed out, that card is dragging your score on its own regardless of what the others look like.

Length of credit history is 15 percent. Older accounts help your score. This is why closing a credit card you never use can hurt you even though it feels like the responsible thing to do. You lose both the available credit it represented and the age it added to your average account history. Two hits from one decision. This factor also quietly punishes people who came to credit late: immigrants, people who grew up in cash-only households, people who avoided debt on principle. The system treats “never needed to borrow” the same as “borrowed and failed.” That is a design choice, not a law of nature.

Credit mix is 10 percent. Having both loans, like a car or student loan, and credit cards signals to lenders that you can manage different kinds of debt. Do not take on debt you do not need just to improve your mix. The benefit does not justify the cost. But this factor is why someone with only credit cards can score lower than someone with a card and a car loan, even with an identical payment history.

New credit inquiries are 10 percent. Applying for credit triggers a hard inquiry that temporarily drops your score by a few points. Hard inquiries stay on your report for two years but only affect your score for one. The exception: shopping for a mortgage or auto loan. Multiple inquiries for the same loan type within a 14 to 45-day window are typically counted as one. The scoring models recognize rate shopping. That same courtesy does not apply to credit card applications.

What Does Not Move Your Score and the Myths That Cost People Real Money

Getting credit scores explained properly means covering what the system ignores, not just what it measures. These myths cost people real money every year.

Your income does not affect your credit score. Not one point. A person earning $200,000 a year who misses payments can have a terrible score. A person earning $30,000 who never misses one can have an excellent score. The system measures behavior, not earnings. It also does not account for why you missed a payment. Job loss, medical emergency, a month where the math did not work. None of that registers in the formula.

Checking your own credit score does not hurt it. Looking at your own file is a soft inquiry. Zero effect on your score. The myth that it hurts has kept people from monitoring their own credit for years. That is good for the bureaus and bad for you. Check it as often as you want.

Carrying a balance on your credit card does not help your score. This is one of the most expensive myths in personal finance. A lot of people believe they need to carry a balance to show they are using credit. They do not. They are paying interest for nothing. Utilization is measured at your statement closing date, before your payment is due. The spending shows up. The balance you carry forward does not need to exist. Pay your card in full every month. Carrying a balance costs you money and does absolutely nothing for your score.

Closing a paid-off credit card does not help your score. It usually hurts it. Unless the card has an annual fee you cannot justify, leave it open. Make a small purchase on it every few months to keep it active. That is it.

The Score You See Is Probably Not the Score That Matters

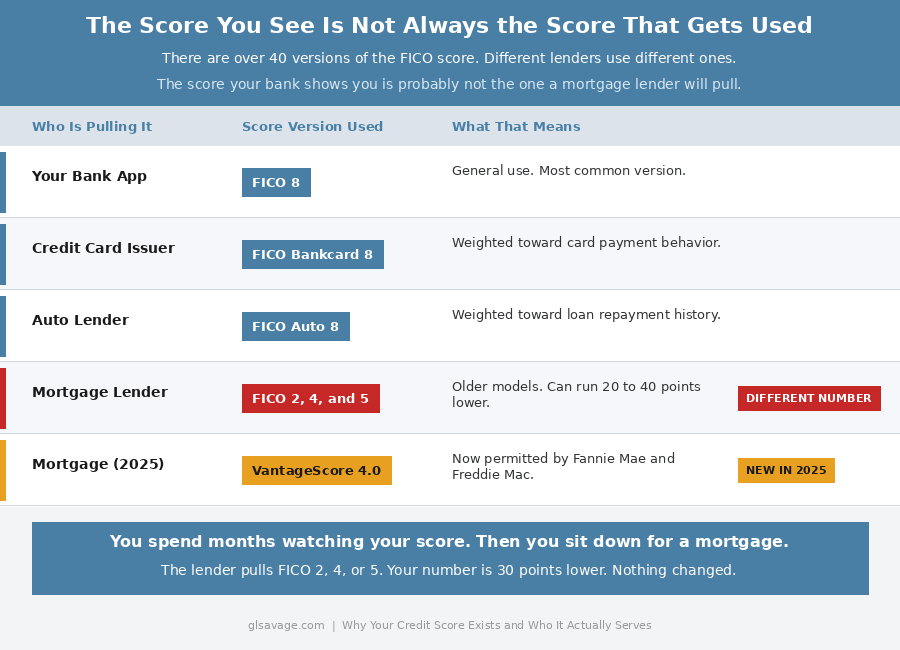

There is no single FICO score. There are over 40 versions of it. This is the part of credit scores explained that catches people the hardest, because it means the number you have been watching may not be the number that gets used when it matters most. The score your bank or credit card app is showing you is likely FICO 8, the most common general version. But mortgage lenders use older models, FICO 2, 4, and 5, that can produce meaningfully different numbers from the exact same credit file. Auto lenders use their own version. Credit card issuers use another. These are not the same number. They weight the same information differently.

What this means in practice: you spend months watching your score, it looks strong, you feel prepared, and then you sit down to apply for a mortgage and the lender pulls a number that is 30 or 40 points lower. Not because anything changed. Because they used a different version of the formula. The score you were watching the whole time was never the one they were going to use.

There is no easy fix for this. But knowing it exists means you stop walking into major financial applications assuming the number you see is the number a lender will see. If you are preparing for a mortgage, ask the lender specifically which FICO versions they pull. Some will tell you. Most will not volunteer it.

The Timing Move That Almost Nobody Knows About

Your utilization is not measured continuously. It is captured at one specific moment each month: the day your credit card statement closes. Whatever your balance is on that day is what gets reported to the bureaus. That is the number that affects your score.

Which means you can control what that number looks like. Pay your balance down to near zero a few days before your statement closes, and that low balance is what gets reported, even if you spent normally throughout the rest of the month. Your score sees responsible utilization. Then your actual due date comes, you pay whatever small amount is left, and you have paid no extra interest.

Most people pay on the due date and never think about the statement close date. Those are two different dates and only one of them affects your score. Find out when your statement closes. That is the date that matters for your score, not the one printed on your bill.

What the Credit Industry Does Not Want You to Know

One in five consumers has at least one error on a credit report, according to a Federal Trade Commission study. One in twenty has an error significant enough to result in denied credit or a higher interest rate. These are not rare edge cases. Errors are common, they cost people money, and the burden of finding and fixing them falls entirely on you. That is the part of credit scores explained that no bureau is going to walk you through.

Medical debt has changed. The CFPB finalized a rule in January 2025 to remove medical debt from credit reports entirely. That rule is facing legal challenges and its final status may still shift. What is already in place: paid medical collections have been excluded by the major bureaus since 2023, and medical debt under $500 is no longer factored into scores. A $300 emergency room bill that went to collections used to be able to damage your credit for years. Check your reports now. If you have medical debt showing, check whether it should still be there under current rules and dispute anything that should not.

A pay-for-delete agreement is a real thing and most people do not know to ask for it. If you have a collection account, you can try to negotiate with the collector to pay the debt in exchange for them removing the item from your report entirely, not just marking it paid. Not every collector will agree. Nothing is guaranteed. But if you pay a collection account without asking first, you have already surrendered your leverage. The standard outcome is the item stays on your report marked paid, which is better than unpaid but still sitting there for years. Ask before you pay. Get any agreement in writing before a dollar changes hands.

Credit repair companies cannot do anything for you that you cannot do yourself for free. If the negative information is accurate, no one can legally remove it before the reporting window expires, typically seven years. If it is inaccurate, you can dispute it directly with the bureaus at no cost. Companies charging monthly fees and promising fast removals are selling something that does not legally exist. The FTC has taken enforcement action against many of them. Their customers still lost the money they paid.

The bureaus are not on your side when you dispute an error. The investigation is typically run through a system called e-OSCAR, which is operated by the bureaus themselves. When you submit a dispute, the bureau does not read your letter and investigate. They send a two-digit code to the original creditor. The creditor clicks confirm. That is the entire investigation in most cases. If the creditor confirms what they originally reported, the item stays on your file, even if it is wrong. Getting a real human review takes persistence, written documentation, and often a formal complaint to the CFPB. That complaint changes the equation in ways that an online dispute rarely does.

How to Actually Build or Rebuild Credit

If your score is low or you have no credit history yet, these are the fastest legitimate paths.

A secured credit card requires a cash deposit that becomes your credit limit. Use it for small purchases, pay the balance in full each month, and the issuer reports your activity to the bureaus. After six to twelve months of on-time payments your score will start moving. Confirm the issuer reports to all three bureaus. Not all do. If they only report to one, you are building history at one bureau and leaving the others empty.

Becoming an authorized user on someone else’s account is another path. If a family member or close friend with solid credit adds you to their card, their positive history on that account can show up on your report and lift your score. You do not need to use the actual card. The account holder takes on the risk, so this requires real trust. Make sure the card issuer reports authorized users to the bureaus before assuming it will help.

Credit builder loans work by lending you money that goes into a savings account while you make monthly payments. At the end you get the money. The point is the payment history, not the cash. Some credit unions offer these. Self, Inc. is an online option if local credit unions are not available to you. If you are also trying to build an emergency fund living paycheck to paycheck, a credit builder loan can do both jobs at once: it builds your score and puts money aside.

Paying down existing balances is often the single fastest lever for someone who already has credit. Utilization recalculates every billing cycle. Prioritize the card closest to its limit first. That near-maxed card is doing disproportionate damage on its own. Paying it down moves your score faster than spreading the same dollars across multiple cards with room to spare. This connects directly to how minimum payments keep you in debt. The same balance that is hurting your utilization is also growing if you are only making minimum payments.

How to Fight Back on Errors

Pull all three reports at AnnualCreditReport.com. Review each one separately, line by line. Look for accounts you do not recognize, late payments you know you made on time, wrong balances, or collection accounts that do not belong to you. Identity theft usually shows up here before it shows up anywhere else.

Dispute errors in writing, not just online. The online portals are convenient for the bureaus because automated systems cost less than human reviews. A written dispute sent by certified mail creates a paper trail that is harder to dismiss. Include copies of any documentation: a bank statement showing you paid on time, a letter from the creditor confirming a debt was settled. The bureau is required to investigate and respond within 30 days.

If a dispute is rejected and you still believe the information is wrong, file a complaint with the CFPB at consumerfinance.gov/complaint and with your state attorney general. You can also add a 100-word consumer statement to your credit report explaining the disputed item. It does not change your score, but lenders who pull your full report will see it. It is your right to put your side of the story on record.

How collection accounts affect your credit report is its own subject and worth understanding fully, especially if you have older debts showing up that may be past their reporting window.

The Number Does Not Define You. But It Does Cost You.

A credit score does not measure your worth or your character or how hard you have worked. It measures one specific thing: how consistently you have repaid borrowed money, according to a formula built by a private company to serve lenders. That formula can improve. It improves through boring, consistent action. Pay on time. Keep balances low, especially on cards that are close to their limits. Pay attention to your statement close date, not just the due date. Do not close old accounts. Do not apply for credit you do not need. Pull your reports, find the errors, and fight them.

That is credit scores explained without anyone trying to sell you something. The myths cost real money every year. People paying interest on balances they never needed to carry. People closing accounts that were quietly helping them. People paying credit repair companies for services they could have done themselves for free. People walking into a mortgage application trusting a score a lender was never going to use. The system is complicated by design. Now you know how it actually works.

Frequently Asked Questions About Credit Scores Explained

670 and above is generally considered good. 740 and above is very good. 800 and above is excellent. The practical difference is real: better interest rates on loans and mortgages, easier apartment approvals, lower car insurance premiums in most states, and better credit card terms. How much lower on car insurance specifically is worth understanding. Car insurance is a rigged game and your credit score is one of the levers they use against you. The gap between a fair score and an excellent one can translate to thousands of dollars over the life of a mortgage or car loan.

Most people can establish a scoreable credit file within three to six months of opening their first account. Getting above 700 typically takes one to two years of consistent on-time payments and low utilization. Getting into the excellent range generally requires several years of clean history. There are no legitimate shortcuts. Anyone promising otherwise is selling something.

Not automatically. A paid collection stays on your report marked paid, which is less damaging than unpaid. Before you pay anything, attempt a pay-for-delete negotiation where the collector agrees to remove the item entirely in exchange for payment. Get that agreement in writing before a dollar changes hands. Once you pay without the agreement, your leverage is gone.

More than most people expect. For someone with a high score and clean history, one missed payment can drop their score 60 to 100 points or more. For someone with an already lower score, the impact is typically smaller. The key is the 30-day window: catch a missed payment within 30 days and it does not appear on your report. After that it stays for seven years.

A hard inquiry drops your score a few points temporarily, typically 5 to 10. The impact fades over 12 months. The more lasting effect is that a new account lowers your average account age. Avoid opening new accounts in the months before applying for a mortgage or major loan. That is when a few points in either direction can change your rate.

Because Equifax, Experian, and TransUnion operate independently and not all creditors report to all three. Different data produces different scores. An error at one bureau does not automatically appear at the others, and a correction you make at one does not automatically carry over either. This is why reviewing all three reports separately every year matters.

Not successfully. The bureaus are only required to remove inaccurate information. Accurate negative items stay for their full reporting window, typically seven years. Anyone claiming they can remove accurate negative information for a fee is misleading you. You can add a 100-word consumer statement explaining the circumstances. It does not change your score but lenders who pull your full report will see it.

Paying down credit card balances is typically the fastest lever because utilization recalculates every billing cycle. Prioritize the card closest to its limit. You can speed things up further by paying your balance down before your statement close date, since that is when your balance gets reported to the bureaus, not the payment due date.

A pay-for-delete is a negotiation where you offer to pay a collection account in exchange for the collector removing the negative item from your credit report entirely. Not all collectors will agree. But it is worth attempting before you pay any collection account, because once you pay without that agreement the item stays on your report as paid. Get any agreement in writing first. If they will not put it in writing, do not pay.

The CFPB finalized a rule in January 2025 to remove medical debt from credit reports entirely. That rule faces legal challenges. What is already in place: paid medical collections have been excluded by the major bureaus since 2023 and medical debt under $500 is no longer factored into scores. Check your reports and dispute any medical debt that should not be there under current guidelines.

No. They cannot legally do anything you cannot do yourself for free. If negative information is accurate, no one can remove it before the reporting window expires. If it is inaccurate, you can dispute it directly with the bureaus at no cost. Monthly fees and promises of fast results are charging you for the illusion of control. Use that money on your actual balances instead.

Because there are over 40 versions of the FICO score and different lenders use different ones. The score in your bank app is likely FICO 8. Mortgage lenders have traditionally used FICO 2, 4, and 5, which can produce numbers 20 to 40 points lower from the exact same credit file. As of July 2025, Fannie Mae and Freddie Mac also permit VantageScore 4.0 for conforming mortgages. Ask your lender which version they pull before you apply.

Not at all. Income is not a factor in any major credit scoring model. Your score measures how you have managed borrowed money, not how much you earn. A high earner who misses payments will score lower than a modest earner who never does.

Credit utilization is the percentage of your available credit you are currently using. It makes up 30 percent of your FICO score and moves fast in both directions. Keep it below 30 percent across all cards and below 30 percent on each individual card. Under 10 percent is better. A single card near its limit drags your score down on its own regardless of what your other cards look like. Pay that one down first.