There is a tax credit worth up to $8,046 that the federal government created specifically for people who work and do not earn a lot. It is called the earned income tax credit, and it has been on the books since 1975. In 2024, about 24 million workers and families collected it. The average payment was $2,894. And yet, according to the IRS itself, roughly one in five people who qualify never claim it. That is about $7.3 billion in congressionally authorized money left on the table every single year, by the people it was designed to help most.

This is not a loophole. It is not a gray area. It is money the government specifically appropriated for low- and moderate-income workers, sitting uncollected because the system that delivers it is complicated, intimidating, and largely unexplained to the people who need it.

This article is going to change that. Here is exactly how the earned income tax credit works, who qualifies, how much you can get, and the parts nobody talks about, including the ones that can work against you if you are not prepared.

What the Earned Income Tax Credit Actually Is

A tax credit is different from a tax deduction. A deduction reduces the amount of income the IRS uses to calculate what you owe. A credit reduces the actual tax bill itself, dollar for dollar. The earned income tax credit is even better than a standard credit because it is refundable, which means if the credit is worth more than what you owe in taxes, the IRS pays you the difference as a refund. You do not have to owe taxes to benefit from it. You just have to qualify and file.

The credit was designed as a work incentive, a way to offset the payroll taxes that come out of every paycheck for people earning low wages. Social Security and Medicare taxes, which together take about 7.65% out of every dollar you earn, hit lower-income workers harder as a percentage of their income than anyone else. The earned income tax credit was built to put some of that back.

It phases in as your income rises, reaches a peak, then phases out as income continues to climb. Families with more children get a larger credit. Workers without children get a smaller one. The key is that you have to have earned income, meaning money from a job, self-employment, or gig work. Passive income, Social Security, unemployment, and child support do not count as earned income for this purpose. Whether you qualify comes down to your specific income, your family situation, and a few rules that the next section lays out plainly.

Who Qualifies and How Much They Can Get

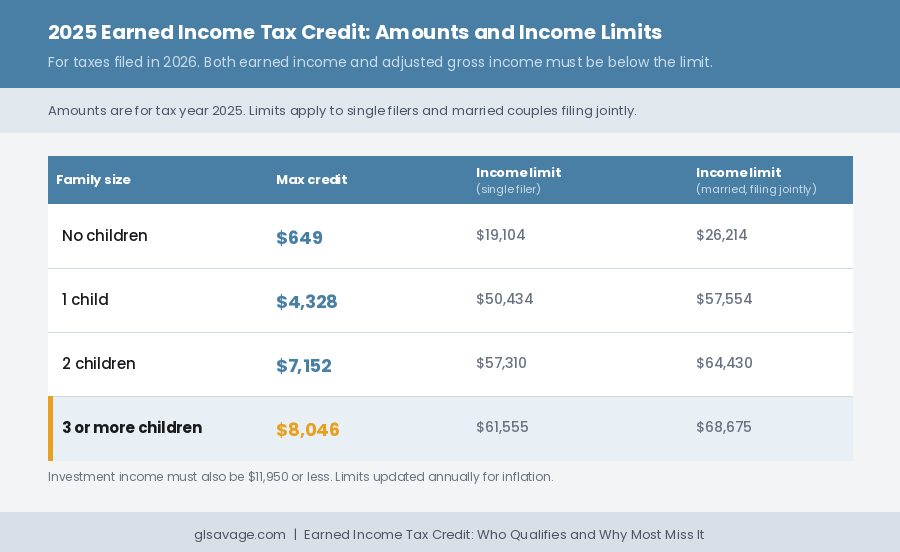

The income limits and credit amounts are updated every year for inflation. For the 2025 tax year, the credit maxes out at $8,046 for a family with three or more qualifying children. With two children the maximum is $7,152. With one child it is $4,328. For workers without qualifying children the maximum is $649. The amounts are smaller without children, but the credit still exists and is still worth claiming if you qualify.

Here is how the IRS determines whether you qualify.

Income is the first thing. For the 2025 tax year, single filers can earn up to roughly $19,104 with no children, $50,434 with one child, $57,310 with two children, and $61,555 with three or more. Married couples filing jointly get higher limits: roughly $26,214 with no children up to $68,675 with three or more. Both your earned income and your adjusted gross income, which is your total income after certain deductions are factored in, have to fall below these numbers. If either one goes over, you are out regardless of how the other looks.

Investment income is capped at $11,950 for 2025. That means money from interest, dividends, rents, or selling assets. Most people who qualify for this credit do not have much investment income, but a small amount of interest from a savings account you forgot about can quietly disqualify you if it pushes you over the limit.

Everyone on the return needs a valid Social Security number. You, your spouse if you are filing jointly, and every child you claim all need one, issued before the return’s due date. Missing or invalid Social Security numbers are one of the most common reasons EITC claims get rejected outright.

If you are married, you have to file jointly. Married filing separately does not work for this credit. There is a narrow exception if you and your spouse lived apart for the last six months of the year and you have a qualifying child, but the default rule is joint return or no credit.

If you are claiming the credit without a qualifying child, you have to be between age 25 and 64. No age limits apply if you have a qualifying child on the return.

What Makes a Child a Qualifying Child

This is where more claims go wrong than anywhere else, and where audits are triggered most often. The IRS definition of a qualifying child for the earned income tax credit is specific, and it is not the same as just having a child or claiming a dependent.

The child has to meet four tests. The relationship test: the child must be your biological child, stepchild, adopted child, foster child, sibling, half-sibling, step-sibling, or a descendant of any of those, such as a grandchild or niece. The age test: the child must be under 19 at the end of the year, or under 24 if a full-time student, or any age if permanently and totally disabled. The residency test: the child must have lived with you in the United States for more than half the year. The joint return test: the child cannot have filed a joint return with their own spouse for the year, unless the only reason they filed was to claim a refund of withheld taxes.

The residency test is the most commonly challenged one in audits. If the child lives with you more than half the year but you cannot document it, the claim can be denied. Utility bills, school records, medical records, and letters from childcare providers are all forms of documentation that can help establish residency if you are ever asked.

Only one person can claim a child for the earned income tax credit in a given year. If two people attempt to claim the same child, the IRS uses tiebreaker rules. Between a parent and a non-parent, the parent wins. Between two parents who both lived with the child, the one who lived with the child longer during the year wins. Between two people who lived with the child the same amount of time, the one with the higher adjusted gross income wins. This matters for separated families and multi-generational households where more than one adult might technically qualify.

The Angles Nobody Covers

The eligibility rules above are what every other article on this topic covers. Here is what they leave out.

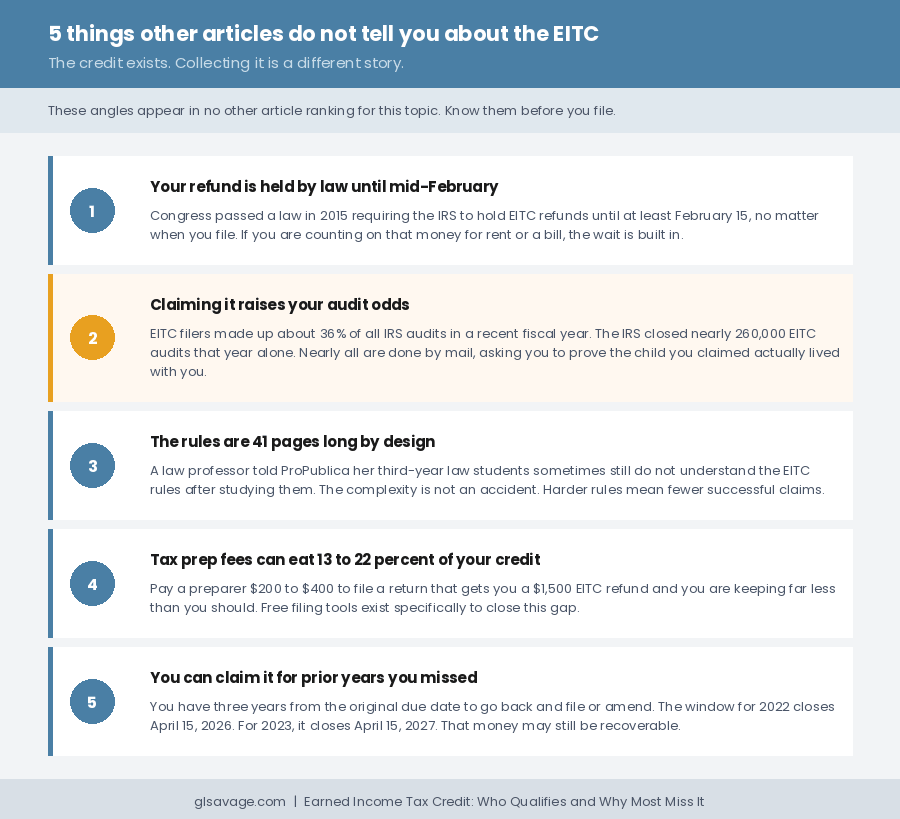

The IRS holds your refund by law if you claim the earned income tax credit. Congress passed a law in 2015 requiring the IRS to hold all refunds that include the earned income tax credit until at least February 15, regardless of when you file. The stated reason was fraud prevention. The practical effect is that people who file in January and expect their refund in a few weeks will wait until at least mid-February or later for any refund that includes this credit. If you are counting on that money for rent, a bill, or an emergency, factor that in. Filing as early as possible and choosing direct deposit gets you the money as fast as the law allows, but the minimum wait is baked in.

Claiming the earned income tax credit raises your audit odds. A study conducted by Stanford University with economists from the U.S. Treasury found that EITC claimants are audited at higher rates than most other taxpayers. In one recent fiscal year the IRS closed nearly 260,000 EITC audits. For context, EITC filers made up about 36% of all IRS audits that year, despite representing a much smaller share of all returns. Nearly all of these audits are done by mail, not in person. You receive a letter asking you to prove you qualified, typically by documenting that the child you claimed actually lived with you. The process can drag on for months, and the IRS will ask for records you may not have thought to keep. Read How Payday Loans Are Legal and What to Do Instead to understand why delays in income like a held refund can trigger a cascade of financial problems when your margin is already thin.

The rules are complicated. Not a little complicated. A law professor at Washington and Lee University who has studied the EITC told ProPublica that her third-year law students sit down and study the EITC materials and sometimes still do not get it. The IRS instructions for claiming the credit run to 41 pages. This is not an accident. A system that is hard to get through produces fewer successful claims, which costs the government less money. The complexity is a feature of the design, not a bug in it.

Tax prep fees can eat a significant chunk of what you receive. Research cited in the American Prospect found that tax preparation fees eat up between 13 and 22 percent of EITC benefits for some filers. If you pay a tax preparer $200 to $400 to file a return that produces a $1,500 EITC refund, you are keeping far less than you should. The section below on how to claim it covers the free options that exist specifically to prevent this.

You can claim it for prior years you missed. If you qualified for the earned income tax credit in past years but did not claim it, you have three years from the original due date of the return to go back and file or amend. For the 2022 tax year, that window closes April 15, 2026. For 2023, it closes April 15, 2027. Money you left on the table in prior years may still be recoverable. See Why Your Tax Refund Is Not Free Money for context on why recovering money you were owed matters more than it might seem when it arrives as a lump sum.

The Groups Most Likely to Miss It

The IRS has identified the groups that leave this money unclaimed most often, and the reasons are worth understanding because they are structural, not personal.

Workers without children are the biggest missed group. The credit for childless workers is smaller, topping out at $649 for 2025, but it is still real money and it goes unclaimed constantly because most people assume this credit requires children. It does not. If you are between 25 and 64, worked during the year, and earned below roughly $19,104 as a single filer, you likely qualify and most people in this situation have no idea.

People whose income changed during the year often do not realize they suddenly qualify. If you had a job loss, a divorce, or any other event that dropped your income below the threshold partway through the year, you may qualify for the first time even if you did not in prior years. Eligibility is determined by what happened in that tax year, not what happened the year before.

Gig workers and self-employed people frequently undercount this credit or miss it entirely. Net earnings from self-employment count as earned income. If you drove rideshare, did freelance work, or ran any kind of side business, that income counts toward eligibility. The calculation is slightly different because you are paying both the employee and employer sides of Social Security and Medicare taxes, which affects how the credit is computed, but the credit is still available.

People in nontraditional living situations, including grandparents raising grandchildren or aunts and uncles raising nieces and nephews, often do not realize they may qualify. If the child lives with you for more than half the year and meets the relationship and age tests, you may be eligible even if you are not the biological parent.

Veterans and people who receive disability payments before retirement age may also qualify and frequently miss the credit. Certain disability payments count as earned income for EITC purposes.

If any of these situations describe you, run your numbers through the free IRS EITC Assistant at irs.gov before you assume you do not qualify. The tool takes about ten minutes and tells you directly whether you are eligible and how much you can expect.

How to Claim It Without Paying Someone a Chunk of It

The IRS Free File program allows anyone with an adjusted gross income of $84,000 or less to file their federal taxes for free using name-brand tax software. If you qualify for the earned income tax credit, you almost certainly fall under this income threshold. Go to irs.gov/freefile to access it. The software walks you through eligibility automatically and files Schedule EIC, the additional form required when you are claiming a qualifying child, as part of the process.

VITA, which stands for Volunteer Income Tax Assistance, is an IRS-certified program that provides free in-person tax preparation for people who generally earn $67,000 or less. Trained and certified volunteers prepare your return at no charge and are specifically trained on credits like the earned income tax credit. To find a location near you, use the VITA locator tool at irs.gov. This is worth using if the complexity of the rules makes you nervous or if your situation involves a qualifying child, self-employment income, or a household arrangement that does not fit the standard mold.

If you use tax software, it will ask you the questions needed to determine eligibility and calculate the credit. The IRS also has a free EITC Assistant tool at irs.gov that walks through eligibility step by step without requiring you to file anything. Run your numbers through it before filing so you know what to expect.

When you file, claim the credit on your Form 1040. If you have a qualifying child, you also file Schedule EIC, which asks for information about the child including their Social Security number, birth year, and the relationship. Standard tax software handles this automatically. Do not skip it or leave it blank.

What to Do If You Are Audited

If you claim the earned income tax credit and receive an audit letter, do not panic and do not ignore it. Ignoring it will result in the IRS disallowing the credit and you owing the money back, plus interest. Responding matters.

EITC audits are almost entirely done by mail. The letter will explain what documentation the IRS needs and give you a deadline to respond. The most common request is proof that the child you claimed lived with you for more than half the year. School enrollment records, medical records, letters from teachers or childcare providers, and utility bills at your address during the relevant period can all serve as documentation.

If you qualify for the credit and can document it, respond with everything you have. If you cannot gather all the requested documentation before the deadline, call or write to the IRS and ask for more time. The deadline is real and missing it closes your options.

If you need help responding to an audit and cannot afford a tax attorney, the Low-Income Taxpayer Clinic program provides free or low-cost legal assistance for tax matters to people who earn below 250% of the federal poverty level. You can find a clinic near you through the Taxpayer Advocate Service at taxpayeradvocate.irs.gov. The Taxpayer Advocate Service itself is a free, independent IRS program that helps people work through problems with the IRS, and it is worth knowing about if the process becomes difficult.

The Honest Takeaway

The earned income tax credit is the largest anti-poverty program for working-age people in the United States. In 2024 it lifted about 4.4 million people above the poverty line, including 2.3 million children. It is funded, it is legal, and it was specifically designed for people in your income range. The government set this money aside. The only question is whether you are going to collect what you are owed.

One in five eligible people does not. Not because they chose not to. Because the system made it hard enough, complicated enough, and frightening enough, between the audit risk and the 41-page instruction manual, that they quietly walked away from it. That is the system working exactly as it was designed.

File. Use the free tools. Document your child’s residency if you have one. And if you missed it in prior years, go back and get it. The window is still open.

Frequently Asked Questions

What is the earned income tax credit?

The earned income tax credit is a refundable federal tax credit for people who work and earn low to moderate incomes. Refundable means that if the credit is worth more than what you owe in taxes, the IRS pays you the difference as a cash refund. For the 2025 tax year it is worth up to $8,046 for families with three or more children, and up to $649 for workers without children.

Who qualifies for the earned income tax credit?

You need earned income from a job or self-employment, a valid Social Security number, and income below the IRS threshold for your filing status and number of children. For 2025, single filers without children must earn below roughly $19,104. With children the limit ranges from about $50,434 to $61,555 depending on how many children you have. Married couples filing jointly have higher limits. You also cannot have more than $11,950 in investment income and cannot file as married filing separately.

Do I need children to claim the earned income tax credit?

No. Workers without qualifying children can still claim the credit if they are between ages 25 and 64 and their income falls below the limit. The credit is smaller without children, topping out at $649 for 2025, but it is real money that most childless eligible workers never claim because they assume this credit requires children.

How do I claim the earned income tax credit?

Claim it on your Form 1040 when you file your federal tax return. If you have a qualifying child you also need to file Schedule EIC with the return. Standard tax software handles both automatically. If you cannot afford tax preparation, use the IRS Free File program at irs.gov or find a free VITA tax preparation site near you through the IRS locator tool.

Why is my refund delayed if I claim the earned income tax credit?

Federal law requires the IRS to hold all refunds that include the earned income tax credit until at least February 15. This applies regardless of when you file. The law was passed in 2015 as a fraud prevention measure. Filing electronically and choosing direct deposit is the fastest way to receive the refund once the hold period ends.

Can claiming the earned income tax credit trigger an audit?

Yes, at higher rates than most other credits. EITC claimants make up a disproportionate share of IRS audits, and nearly all of those audits are done by mail. The most common issue is the IRS questioning whether a claimed child actually meets the residency requirement. Keep records that document where your child lived, such as school records and medical records, in case you are asked to provide them.

Can I claim the earned income tax credit for prior years I missed?

Yes. You have three years from the original due date of the return to file or amend and claim the credit. For 2022 that window closes April 15, 2026. For 2023 it closes April 15, 2027. If you filed a return but forgot to claim the credit, file an amended return using Form 1040-X.

Does the earned income tax credit count as income for other benefits like food stamps or Medicaid?

No. The earned income tax credit is not counted as income for most federal benefit programs including SNAP food benefits, Medicaid, Supplemental Security Income, and public housing. Receiving it will not reduce your eligibility for other assistance programs.

What is the EITC income limit for 2025?

For the 2025 tax year, single filers must earn below roughly $19,104 with no children, $50,434 with one child, $57,310 with two children, or $61,555 with three or more children. Married couples filing jointly have limits roughly $6,000 to $7,000 higher in each category. Both your earned income and your adjusted gross income, meaning your income after certain deductions, must fall below the limit.