There is a conversation the personal finance industry has been having for years about how to pay off debt. Snowball method. Avalanche method. Which one fits your personality. What they are not talking about is the question that actually matters for anyone who is stretched thin and trying to survive inside an expensive system. That question is not which debt costs the most in interest. It is which debt, if you fall behind on it, takes down your ability to earn the money you need to pay off everything else. Get the debt payoff order wrong and you are not just paying more in interest. You are potentially losing the car that gets you to work, which means losing the income that pays every debt you have. That is not a math problem. That is a survival problem. And no snowball or avalanche method is going to save you from it.

The Advice You Keep Hearing Is Answering the Wrong Question

Every major financial website frames the debt payoff conversation the same way. Do you want quick wins to stay motivated? Use the snowball method: pay the smallest balance first. Are you analytical and patient? Use the avalanche method: pay the highest interest rate first. Pick the one that fits your personality and get started.

Both strategies are built around the same assumption: that all your debt is basically the same kind of problem. Collection calls if you fall behind. Credit score damage. Bad but manageable. That assumption works fine if every debt you have is a credit card or a personal loan. It falls apart the moment a financed car or a mortgage is in the mix. Because those debts do not just damage your credit score if you fall behind. They remove something from your life that you need to function.

Your car is not just a car. For most people in most of this country, it is the infrastructure that makes everything else possible. It gets you to work. It gets your kids to school. It gets you to the grocery store, the doctor, the second job you picked up to pay down the debt you are trying to organize right now. If you are have or are considering getting a second job, read Why A Second Job Often Costs More than it Pays to decide if this is the correct move for you. Lose that car and you do not just lose transportation. You lose access to your income. You lose the very thing that was going to pay off every debt on your list. That chain of consequences is the one piece of this conversation that almost nobody in the personal finance space wants to say out loud.

Your Car Payment Is Not the Only Bill That Keeps Your Car

This is the part that gets people. They know the car payment matters. What they do not always know is that the car payment is not the only thing standing between them and a repossession.

Every financed car requires full coverage insurance as a condition of the loan. That is in the loan agreement you signed. If your car insurance lapses, even for a single day, your lender has the right to step in and purchase what is called force-placed insurance on your behalf. They will charge you for it. Force-placed insurance costs two to ten times more than a standard policy and it only protects the lender, not you. It does not cover your liability if you hit someone. In some states, it does not even fulfill the minimum legal insurance requirement, meaning you could be driving a car that is force-insured by your lender and still technically uninsured under state law. And the cost of that force-placed policy gets added directly to your loan balance, accruing interest every month you carry it.

If the added cost of force-placed insurance pushes your payment obligations beyond what you can manage, the next step for the lender is repossession. So letting your car insurance lapse to save money is not saving money. It is a trip wire that can set off a chain of consequences that ends with you losing the car anyway, owing more on the loan than when you started, and paying higher insurance rates for years because you now have a lapse on your record. For more information on how to get the best insurance rates for your specific situation read Car Insurance Is a Rigged Game, Here’s How to Play It.

Registration matters too. A car with expired registration can be ticketed and in some states impounded. Driving an impounded car to work is not possible. A car that needs a repair to stay road-legal or road-safe needs to stay on the priority list for the same reason. Your car is a system of costs, not a single bill. Every piece of that system has to stay current or the whole thing fails.

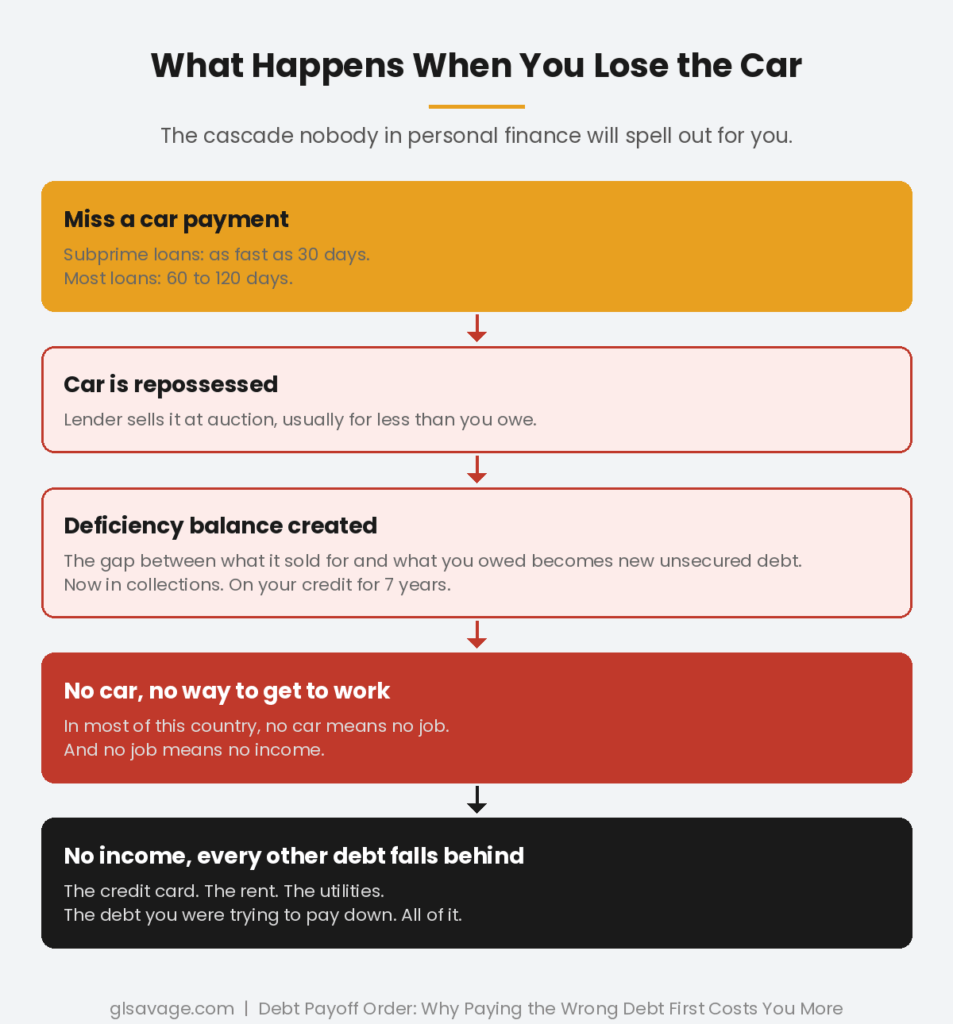

What Happens When the Car Goes

More than 2.2 million vehicles were repossessed in the United States in a recent year, the highest number since 2009. The people who lose cars are not primarily people who stopped caring about their finances. They are people who ran out of options in an economy where the car payment, the insurance, the registration and the repairs together often consume a devastating percentage of a paycheck that is already being stretched across rent, groceries, utilities and debt.

When a car is repossessed, the lender takes the vehicle and sells it, usually at auction for far less than what it is worth. Whatever gap exists between what the car sold for and what you still owed on the loan becomes a deficiency balance. A deficiency balance is new unsecured debt that can be sent to collections, reported on your credit, and pursued in court. You lose the car and you still owe money on it. The repossession stays on your credit report for seven years. And you are now trying to pay off all your other debts without the transportation you were using to earn the income to pay them.

There is a saying that captures what happens next: you can sleep in your car but you cannot drive your house to work. When the car goes, people often lose jobs because they cannot get there. Job loss then accelerates every other debt problem. The cascade is real. Protecting the car is not about sentiment. It is about protecting the income that makes debt payoff possible at all.

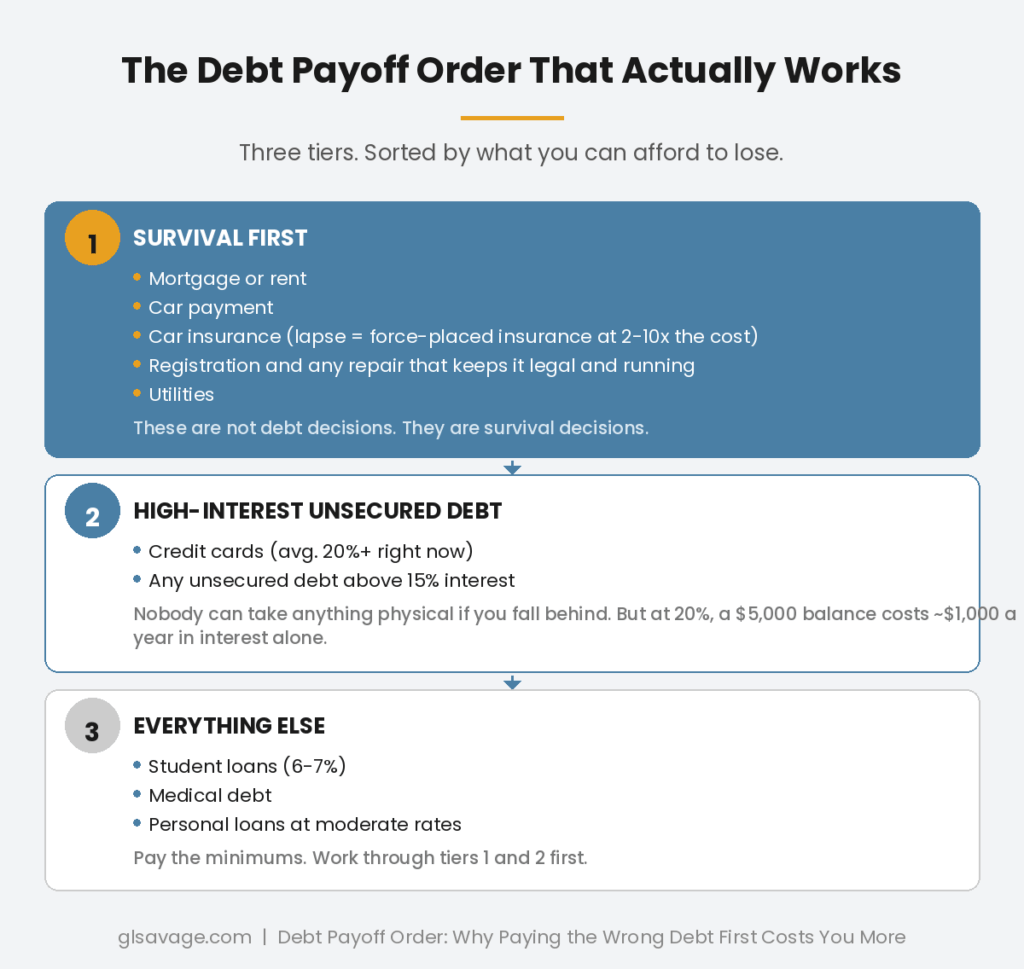

The Real Debt Payoff Order: Triage First, Strategy Second

Here is how to actually think about debt payoff order. Not as a personality test. As a triage system based on consequences.

The first priority is everything that keeps you employed and housed. Mortgage or rent. Car payment. Car insurance. Registration and any repair that keeps the car legal and running. Utilities that keep your home functional. These are not even really debt payoff decisions. They are survival decisions. Every other debt on your list gets its minimum payment and nothing more until these are current and protected.

The second priority is high-interest unsecured debt that is actively growing against you. The average credit card interest rate is more than 20 percent right now, according to Federal Reserve data. A $5,000 balance at 20 percent costs you roughly $1,000 in interest every year you carry it. Left alone, it does not stay at $5,000. It compounds daily and it grows. Once the first tier is secured, this is where your extra money goes. Not because a credit card collector can take something from you, but because that rate of growth is working against everything else you are trying to do.

The third priority is lower-interest debt with no collateral and no immediate physical consequence. Student loans at 6 or 7 percent. Medical debt. A personal loan at a reasonable rate. These need to be paid. But they are not growing at 20 percent, and falling behind on them does not remove the car that gets you to the income that pays everything else. They come last in the debt payoff order. Pay the minimums while you work through the tiers above them.

Where Snowball and Avalanche Actually Fit

Once your first tier is current and protected, the snowball versus avalanche debate actually matters. Here is how to have it without getting misled.

The debt snowball, paying the smallest balance first regardless of interest rate, works for some people because the psychology is real. Eliminating a bill and freeing up a monthly payment is a genuine win that can keep you moving. Dave Ramsey built an empire on this idea and the people who have used it successfully are not wrong about what worked for them.

What it gets wrong is treating all unsecured debt as equally consequential. Paying off a $500 medical bill to get a quick win while a 24 percent credit card compounds against you every day is not strategy. It is the wrong priority dressed up as motivation. The mathematical cost of ignoring your highest-rate debt in favor of a smaller balance can be hundreds or thousands of dollars depending on how long it takes to work back around to the high-rate card.

The debt avalanche, paying the highest interest rate first, is mathematically correct. If you have a 20 percent credit card and a 6 percent car loan and both are current, the extra money goes toward the credit card every time. That is not a personality preference. That is the rate at which money is being taken from you. Paying the lower-rate debt first because the balance is smaller is an expensive choice that the snowball framing makes feel like wisdom.

Use the avalanche method within your unsecured debt once your secured and essential obligations are current. If a small balance can be cleared quickly without meaningfully slowing your attack on the highest-rate debt, clearing it is fine. But do not mistake the psychological comfort of checking off a box for actual financial progress if the box you checked was costing you 8 percent and the one you left sitting is costing you 22.

The Conversation Nobody Has When Money Is Actually Too Short

Every snowball and avalanche article assumes you have enough money to make minimum payments on everything and put extra toward one debt at a time. Most people reading this do not have that. And nobody in the personal finance space wants to write the article for those people.

When money is actually short, when there is not enough coming in to cover everything, the debt payoff order question is not which debt to eliminate fastest. It is which debt to protect and which to let slide. That is a different and harder question. And the answer, stated plainly, is this: let unsecured debt slide before you let secured debt fall behind.

A credit card that goes to collections will damage your credit score and generate calls and letters for months. That is a real problem. It is not the same problem as losing your car, which means losing your job, which means losing the income that was going to pay everything including that credit card. The credit card company does not want you to know this. They want their minimum payment every month and they want you to let everything else sort itself out. Their interest and your survival are not aligned and nobody in the industry is going to say that directly. Minimum payments keep you in debt and that is not an accident.

If you are in a position where you cannot cover every bill, call your unsecured creditors before you miss payments and ask about hardship programs. Many of them exist. Credit card companies, medical providers, student loan servicers often have deferment or reduced payment options available to people who ask. You have to ask. Meanwhile, protect the things that keep you earning and housed, because losing those makes every other debt problem worse and harder to recover from.

Getting Current Comes Before Paying Extra

If any debt is past due right now, getting it current is more important than the entire payoff order conversation. A debt that is 30 days past due is already costing you late fees and credit score damage. A debt at 60 or 90 days is heading toward collections, repossession, or legal action depending on the type. No amount of extra payments on another account fixes any of that.

Get current first. Then apply the triage system. Minimum payments on everything, extra money flowing into the first tier until it is stable, then into the highest-rate unsecured debt, then working down. That sequence is the actual answer to the debt payoff question. Not because it is the most motivating. Because it is the one that protects your income, protects your housing, and costs you the least when you run it all the way out.

The debt industry wants you focused on interest rates and balance sizes because that keeps you in the frame of the financial product they sold you. The frame that actually serves you starts with one question: which of these debts, if I fall behind, makes all the others harder or impossible to pay? Answer that question first. Everything else follows from it.

Frequently Asked Questions

Which debt should I pay off first?

Protect what keeps you employed and housed before anything else. Car payment, car insurance, mortgage or rent, utilities. Once those are current, put extra money toward your highest-interest unsecured debt, typically credit cards at more than 20 percent on average right now. Lower-interest debt with no collateral comes last. If any debt is past due, getting it current takes priority over paying extra on anything.

Is the debt snowball or debt avalanche method better?

The avalanche method, paying the highest interest rate first, saves you more money. The snowball method, paying the smallest balance first, works better for some people psychologically. Neither addresses the most important variable: whether falling behind on a given debt can remove your transportation or housing. Sort by consequences before you sort by interest rate or balance size.

What happens if I fall behind on my car loan?

Your car can be repossessed as soon as 30 to 120 days after a missed payment depending on your loan terms, your lender, and your state. Subprime and buy-here-pay-here loans can move as fast as 30 days. Most standard loans fall in the 60 to 120 day range. The lender sells the car at auction, usually for less than you owe, and you are responsible for the difference. That remaining balance is called a deficiency balance and becomes new debt that can be sent to collections. The repossession stays on your credit report for seven years.

What is force-placed insurance and why does it matter?

If your car insurance lapses, your lender can purchase insurance on your behalf and charge you for it. That is force-placed insurance. It costs two to ten times more than a standard policy, protects the lender not you, and gets added directly to your loan balance. Letting car insurance lapse to save money on a financed car does not save money. It can trigger a cascade that makes the payment much more expensive or results in repossession.

What if I cannot afford to pay all my debts?

Prioritize in this order: housing, the car and everything that keeps it running and insured, utilities, then everything else. Let unsecured debt slide before you let secured debt fall behind. Call unsecured creditors before you miss payments and ask about hardship programs. A credit card in collections is a credit problem. Losing the car that gets you to work is an income problem that makes every debt harder to pay.

What is the difference between secured and unsecured debt?

Secured debt is backed by something the lender can take if you stop paying. Mortgages and car loans are secured by the home and car. Unsecured debt has no collateral behind it. Credit cards, medical bills, and most personal loans are unsecured. If you fall behind on unsecured debt, the lender can damage your credit, send the account to collections, and eventually sue. They cannot show up and take a physical thing from you the way a secured lender can.

Should I pay off a small balance or a high-interest balance first?

High interest first, within your unsecured debt category, once your secured and essential obligations are current. A 20 percent credit card costs you money every day you carry it. A 6 percent personal loan with a smaller balance costs you far less per dollar. The interest rate is the daily cost of that debt. Prioritize the most expensive debt to carry, not the smallest number on the page.

How does high-interest debt compound over time?

Credit card interest accrues daily based on your average balance. At 20 percent, a $5,000 balance costs roughly $1,000 in interest over a year if you only make minimum payments. The balance does not stay at $5,000. It grows. Over three to five years of minimum payments, the interest paid can exceed the original balance. High-interest unsecured debt that is not being aggressively paid down works against every other financial goal you have at the same time.

If collection accounts are already on your credit report while you work through your debt payoff order, read How Collection Accounts Affect Your Credit Report for what they actually do and how long they stay. And if minimum payments are part of why the balances never seem to move, Minimum Payments Keep You in Debt. That Is Not an Accident. explains the math behind why they were designed that way. For free one-on-one help building a repayment plan, the National Foundation for Credit Counseling connects you with nonprofit counselors who do not sell you anything.