There is a version of the cheap car story that nobody tells you at the point of sale. You buy the car because it is what you can afford. It runs. For a while. Then the repairs start, not all at once, which would at least be honest, but in drips. Fifty dollars here. Four hundred there. A tow. A missed shift. A loan you took out in a panic because the alternative was losing your job. If you have been asking yourself why your car keeps breaking down and costing more than you can manage, the answer is rarely the car itself. By the time most people do the math on what their unreliable car has actually cost them, the number is two or three times what they paid. And that is before you find out about the hidden markup your car dealer almost certainly added to your loan, or the way certain financing options are deliberately set up to make sure your credit never improves no matter how faithfully you pay. The cycle is not bad luck. It is architecture. This is how it actually works, and how to get out.

What an Unreliable Car Really Costs

Most people calculate the cost of a car by its purchase price. That number is almost entirely misleading when the car keeps breaking down. The real cost is the purchase price plus everything the car demands from you in the months and years that follow. And those hidden costs are almost always larger than the visible one.

A $2,500 car does not cost $2,500. It costs $2,500 plus repairs, towing, emergency rides, missed work, and the interest on whatever loan you needed when something major went. In the first year alone, that same $2,500 car frequently lands between $5,000 and $7,000 once everything is added up. At the end of that year, you still have an unreliable car. The second year starts the same way.

Here is what a single year with a problem vehicle actually looks like when you write it down:

- Repairs: $900

- Towing: $400

- Emergency rides to work: $300

- Two missed workdays at $18/hour: $288

That is $1,888 on top of the purchase price in one year. In year two, the total crosses $7,000 and you are still driving the same unreliable car.

The Unreliable Car Cost Nobody Puts in the Brochure: Lost Wages

Repair bills are visible. You get an invoice. Lost income is invisible, and it is consistently the largest real cost of unreliable transportation.

Missing one shift per month at $18 an hour costs roughly $1,700 a year. That is more than most single repair bills. Missing two shifts a month pushes past $3,400. And this does not account for what happens when the missed shifts affect your standing at work, when the car breaks down on the way to a job interview, or when you arrive late enough times that your hours get cut. The unreliable car does not just cost money when it breaks. It threatens the paycheck that every other part of your financial life depends on.

When you are deciding whether to keep repairing or start planning a replacement, lost wages belong in that math. Most people leave them out, and then the repair option keeps looking cheaper than it actually is.

How the Dealer Likely Added to Your Loan Without Telling You

This is the part of the unreliable car story that most people have never heard, and the industry would very much like to keep it that way.

When you finance a car through a dealership, here is what actually happens behind the scenes. The dealer contacts a lender, the lender looks at your credit and tells the dealer the interest rate they will accept, and the dealer presents you with a rate. That rate is almost never the one the lender quoted. Dealers are legally allowed to add percentage points on top of the rate you actually qualified for and keep the difference as their own profit. The government agency that oversees lending, the Consumer Financial Protection Bureau, has confirmed this practice and written about it publicly. They call it a dealer markup, and they note that the dealer has no obligation to tell you it is happening.

What this means in plain terms: you qualified for, say, 7 percent. The dealer shows you 9.5 percent. You sign. The dealer just made hundreds of dollars off the gap between what you were quoted and what you actually qualified for, and you have no idea it happened.

According to one analysis of auto loan data, the average dealer markup costs buyers roughly $1,700 over the life of the loan. For buyers with damaged credit who have fewer alternatives and less negotiating power, the markups tend to be larger, not smaller.

The protection is straightforward. Before you walk into any dealership, get a loan offer in writing from a credit union or your bank. Bring it with you. When the finance office shows you their rate, you have a number to compare it against. If their rate is higher, tell them you have a competing offer. They can match it or lose the financing. Either way, you win.

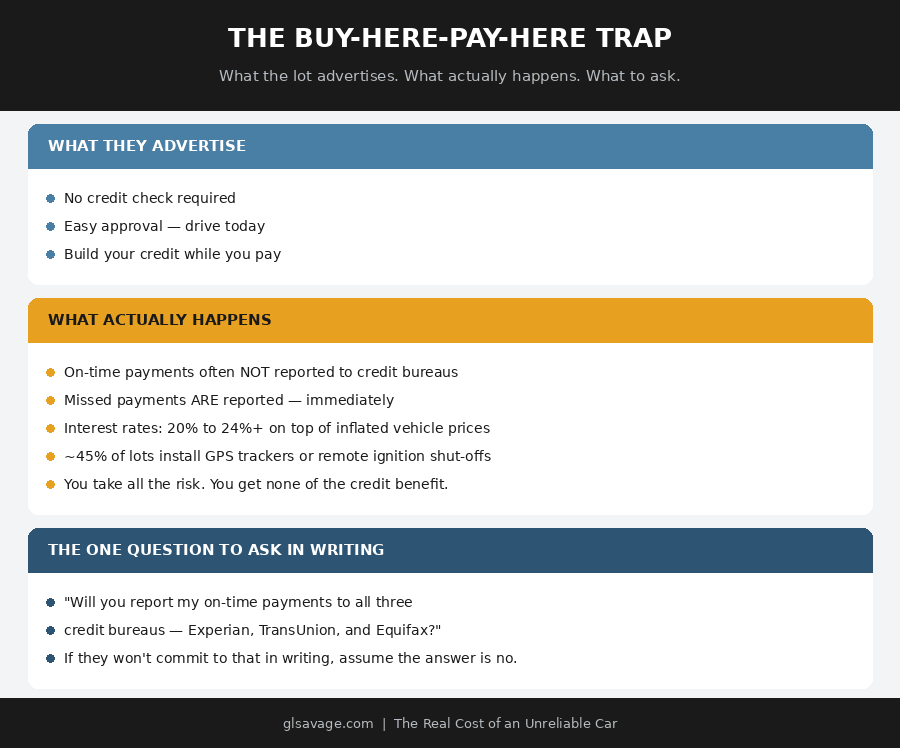

The Buy-Here-Pay-Here Trap Inside the Trap

When credit is damaged and the car died yesterday, a lot with a sign that says “No Credit? No Problem!” can feel like the only option. For some people in some situations it is. But there is something about how these lots operate that they do not put on the sign, and understanding it changes everything about how to use them.

Most buy-here-pay-here dealerships, the ones where the dealer is also the lender and you make your payments directly to the lot, do not report your on-time payments to the credit bureaus. This is confirmed by the Consumer Financial Protection Bureau. What this means is that you can make every single payment, on time, for three years, and your credit score does not move. The thing you are supposed to be building, the credit score that would eventually get you a better interest rate and out of this situation, is not being built. The lot that sold itself as a way to rebuild your credit is, by design, not rebuilding your credit.

But here is the part that makes it a genuine trap. While most of these dealers do not report your good payments, they do report the bad ones. Miss a payment and it goes to the bureaus immediately. Your on-time streak: invisible. Your one missed payment: on your record for years.

There is also a detail that about 45 percent of buy-here-pay-here dealers do not advertise: GPS trackers and remote ignition shut-off devices installed in the vehicle. If you fall behind on payments, the dealer can prevent your car from starting. The Consumer Financial Protection Bureau has documented this practice. You are not just making payments on a car. You are making payments on a car that can be turned off from a desk across town.

If a buy-here-pay-here lot is your only real option right now, that is a workable situation, not a judgment. But before you sign, ask in writing whether they report on-time payments to all three credit bureaus. If they will not commit to that in writing, they are almost certainly not doing it. And treat the arrangement as a temporary bridge while you work on the credit score that gets you out of it, not a long-term solution.

The Repair Shop Financing Counter Has a Loan Shark in It

When a repair bill comes in that you cannot cover in cash, the shop often has a solution right there at the counter. Financing. Fast approval. Sometimes zero interest for 90 days. It sounds like a lifeline.

The National Consumer Law Center investigated this and found that major national chains including Jiffy Lube, Meineke, Midas, and AAMCO were directing customers toward a product called EasyPay Finance with annual interest rates reaching 189 percent. The zero-interest promotional period, which most customers assumed they qualified for, required near-perfect payment conditions that most borrowers never met. One missed payment, one day late, and the full interest rate kicked in retroactively. Consumer Reports confirmed the same findings independently.

When the story became public, Jiffy Lube’s parent company stated its locations are independently operated franchises and it had no knowledge of franchisees working with EasyPay. Midas said the same. The loans were happening anyway.

This is not a small operation running a scam. These are recognizable national brands operating at scale, with financing products specifically designed for people who cannot pay cash for a repair. The people who need the financing most are the ones being handed the worst terms.

The rule here is the same as with the dealer: before you sign anything at a repair counter, ask for the APR in writing. Not the promotional rate. The actual rate if you do not meet every single condition. If they cannot or will not give you that number clearly, call your credit union before you agree to anything. A personal loan from a credit union, even a small one, will almost always cost less than what is sitting on that counter. If you are already carrying balances on top of this, read this next.

Your Credit Score Is the Multiplier on All of It

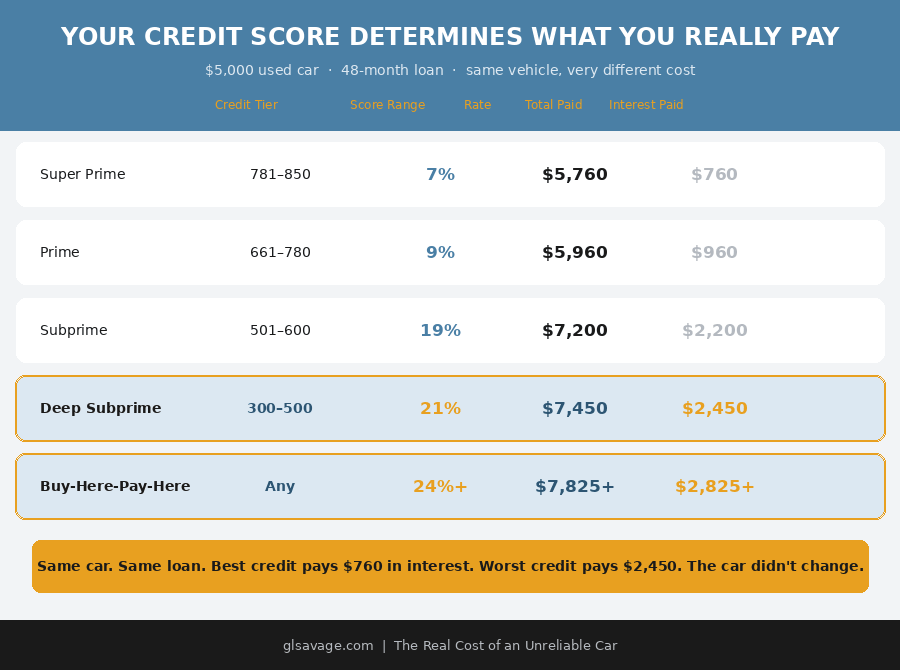

Here is the part of the unreliable car cycle that makes it self-reinforcing. The financial stress that comes with constant repairs, the missed payments on other bills, the collections account from the last emergency, all of it is actively damaging the credit score that determines what every future loan costs you. And the worse that score gets, the more expensive every car purchase, every repair loan, every financing arrangement becomes.

On a $5,000 used car financed over 48 months, the difference between the best and worst credit tier is $1,690 in interest. Same car. Same loan amount. Same 48 months. One person pays $760 in interest. Another pays $2,450. The only difference is the credit score, and the credit score is being damaged by the same cycle that requires them to take the loan.

This is not a personal failing. It is a mechanism. The system charges the most to the people with the least margin, which reduces their margin further, which keeps them dependent on high-interest financing. Understanding that it is a mechanism, not bad luck, is the first step to working against it deliberately.

How to Calculate Your Real Monthly Unreliable Car Cost

Before any decision gets made about keeping or replacing your current vehicle, you need one number: what the car actually costs you each month.

Go back six to twelve months. Add up everything. Repairs. Towing. Emergency rides. Your best estimate of lost wages from missed shifts. Insurance. Fuel. Divide by the number of months. That is your real monthly cost.

Most people who do this for the first time are surprised by the number. It is frequently high enough to support a payment on a significantly more reliable vehicle. The problem was never that a better car was unaffordable. The costs were just scattered and unpredictable, so they never looked like a number. Once you see the number, the math on a replacement usually changes.

Protect Your Income While You Work the Problem

An unreliable car’s most dangerous capability is reaching your paycheck. Everything else in this plan depends on income staying intact while you work toward a better situation. Which means the first move is not fixing the car. It is making sure the car cannot cost you your job.

Identify one coworker who lives near you. One neighbor. One friend. One paid option, a rideshare account already set up, a cab number already saved. Do not wait until the car dies at 6 AM to think about this. Do it now, while it is still running. Then start a small ride fund, ten to twenty-five dollars per paycheck, kept separately, used only for emergency transportation to work. Even a hundred dollars in that fund is the difference between a rough morning and a missed shift.

This is not optimism. It is the recognition that with an unreliable car, something will go wrong. The question is whether you have already solved it when it does.

Build a Transportation Buffer in Stages

The repair-and-scramble cycle runs on the absence of any cushion. Every breakdown forces a panic decision because there is nothing between the problem and the consequence. Rebuilding that cushion is what interrupts the cycle.

The target is three stages: $300, then $500, then $1,000. These numbers are not arbitrary. Three hundred covers most minor repairs without a credit card. Five hundred handles most towing scenarios plus a moderate fix. A thousand dollars is the margin that prevents a breakdown from becoming a high-interest loan. Each stage makes the next crisis survivable without the financial damage that keeps the cycle going.

Keep this money separate from everything else and name it specifically. It is a transportation fund. That specificity makes it harder to spend on other things and easier to rebuild after you use it.

Research the Replacement Before the Unreliable Car Dies

The worst possible time to buy a replacement vehicle is when you need one immediately. Desperation eliminates negotiating power, compresses every decision, and produces exactly the kind of panicked purchase that starts the cycle over. The goal is to already know what you are buying and what it should cost before the current car stops running.

For most people in this situation, the target vehicles are not exciting. They are boring, proven, and cheap to fix. The models that appear consistently in reliability data for under $5,000:

- Honda Civic, 1998 to 2011

- Toyota Corolla, 1998 to 2013

- Honda Accord, 2003 to 2012

- Toyota Camry, 2002 to 2011

- Mazda3, 2010 to 2013

Parts for all of these are widely available. Mechanics know them well. Insurance tends to be lower than average. None of them are exciting. All of them are stable, and stable is the whole point.

Once you have a target, watch local listings for several weeks before you need to buy. Get familiar with what specific years and mileage ranges actually sell for in your area. When you already know the real price before you walk in, no one can pressure you into paying more because you needed a car yesterday.

And before you buy anything, pay for a pre-purchase inspection from an independent mechanic. Not the seller’s mechanic. One you choose. It costs $100 to $150 and will catch problems neither you nor the seller can spot in a test drive. This is the single most effective hundred dollars in this entire process and nearly nobody does it. Do it.

When You Are Ready to Replace: How to Not Get Taken Again

When the buffer is built and the replacement is researched, the execution matters as much as the plan.

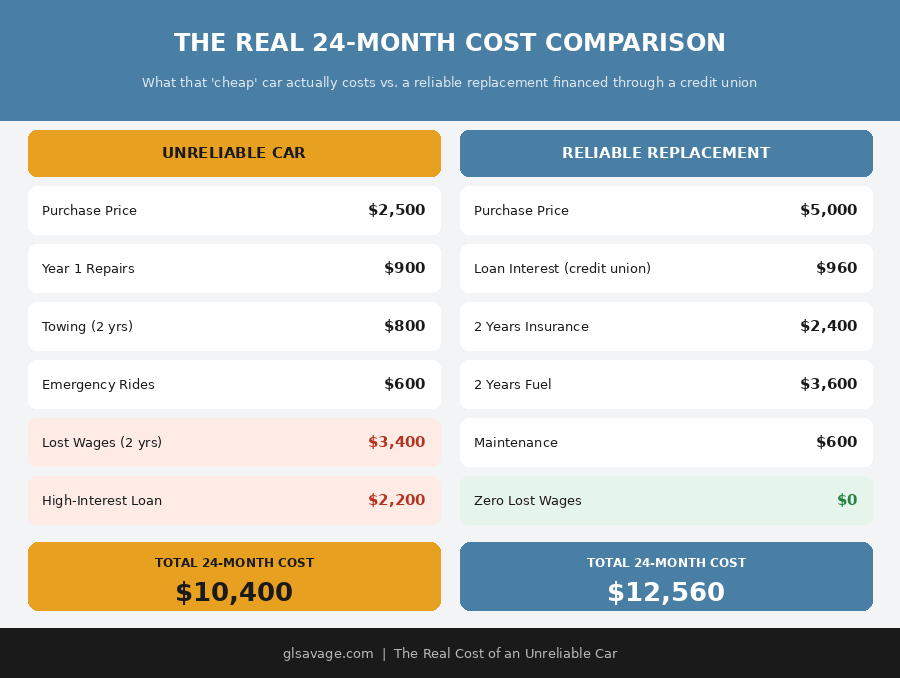

Most people frame this as a cheap car versus a reliable car and assume the cheap car wins on cost. It does not. The cheap car vs reliable car comparison only makes sense when you include every cost, not just the sticker price. A slightly higher monthly payment on a vehicle with a strong reliability record is almost always cheaper over the full picture than a low purchase price plus the repair cycle that follows it. The graphic below shows exactly why.

Get your financing from a credit union before you talk to any dealer. Credit unions consistently offer lower interest rates than dealer financing, and walking in with an approval in hand eliminates the markup entirely. The dealer’s finance office can still try to beat the credit union’s rate, which occasionally works in your favor, but they cannot mark up a rate you have already locked.

Shop insurance from at least three companies before you buy. The difference between the highest and lowest quote on the same vehicle is frequently $300 to $800 per year. Annual insurance cost belongs in your decision about which vehicle to buy, not as an afterthought once you have already committed.

If a buy-here-pay-here lot is the only real option, use it as a bridge. Make every payment. While you are making payments, build the credit score through other means: a secured credit card used lightly and paid in full every month, a credit builder loan from a credit union, every bill paid on time. The goal is to refinance the BHPH loan as soon as you have enough credit history to qualify for something with a real lender, which typically takes 12 to 18 months of consistent payment behavior. One word of caution: before refinancing anything, verify that the vehicle meets the requirements. Most traditional lenders will not refinance a car older than 10 to 12 years or with more than 125,000 miles.

When the Numbers Still Do Not Work

Sometimes even the plan above is out of reach. The repairs are coming too fast, the income is too constrained, or the credit damage is deep enough that reasonable financing is not yet accessible. There are more aggressive options.

If two adults share a home and both have vehicles, selling the less reliable one and sharing the better one eliminates an entire set of costs at once. Insurance, registration, fuel, and maintenance on one vehicle instead of two is a significant monthly difference. Those savings can build the replacement fund faster than anything on this list.

A transfer to a job location closer to home, or taking a position that sits on a bus line, can eliminate the transportation dependency while the financial situation stabilizes. A modest pay cut can be worth considerably more than it appears when it eliminates several hundred dollars per month in transportation costs.

And where public transit, carpooling, or proximity to work makes it genuinely possible: going car-free for twelve months can generate $4,000 to $6,000 in savings. That is enough to buy a reliable vehicle outright, which eliminates the loan, the interest, and the dealer entirely. The trade is a year of inconvenience for a permanent exit from the cycle. It is not for everyone. But it is worth calculating before dismissing it.

The Unreliable Car Cycle Is Not About Your Choices

The system that makes cheap cars expensive to own, that lets dealers secretly mark up your loan, that sells buy-here-pay-here financing as a credit-building tool while quietly not reporting your payments, that puts 189 percent interest products on the counter at national repair chains for people who cannot pay cash, did not end up this way by accident. It is built to extract more from people with less margin, because people with less margin have fewer places to go. That is not a character flaw. That is a structure. When you understand the specific mechanisms, you stop blaming yourself for being in the cycle and start working the exact levers that get you out. That is what this article is for.

Frequently Asked Questions

The real cost includes the purchase price plus all repairs, towing, emergency rides, lost wages, and interest on any loans taken out to cover breakdowns. A $3,000 car can cost $7,000 or more in the first two years when all of these factors are included. The costs feel manageable because they arrive unpredictably and separately rather than as a single visible number, but they add up to the same place.

When you finance through a dealer, the lender tells the dealer what rate they will accept for your credit profile. The dealer is legally allowed to charge you a higher rate and keep the difference as profit. The Consumer Financial Protection Bureau has confirmed this practice and states the dealer has no obligation to disclose it. The protection is to get a loan offer in writing from a credit union before you visit any dealer, so you have a real number to compare against whatever the finance office shows you.

Most do not report on-time payments, according to the Consumer Financial Protection Bureau. This means making every payment perfectly for years may not improve your credit score at all. At the same time, most will report missed payments and repossessions, which do damage your credit. Before agreeing to any buy-here-pay-here arrangement, ask in writing whether they report on-time payments to all three major bureaus. If they will not commit to that in writing, assume they are not doing it.

The National Consumer Law Center found that major national chains including Jiffy Lube, Meineke, Midas, and AAMCO were directing customers to financing products with annual interest rates reaching 189 percent. Promotional zero-interest periods in these products typically have conditions most borrowers do not meet. Before signing any financing at a repair counter, ask for the actual APR in writing, not the promotional rate. If they cannot produce that number clearly, call a credit union before you sign anything.

Calculate your real monthly cost first. Add all repairs, towing, emergency rides, lost wages, insurance, and fuel over the last six to twelve months and divide by the number of months. If that number is approaching what a payment would be on a more reliable vehicle, replacement is almost certainly the better financial decision over time, even when the sticker price feels higher. The key difference is that a reliable car’s costs are predictable. You can budget for predictable. You cannot budget for chaos.

Honda Civic, Toyota Corolla, Honda Accord, Toyota Camry, and Mazda3 from the late 1990s to early 2010s appear consistently in reliability data for this price range. These vehicles have widely available parts, are familiar to most mechanics, and typically cost less to insure and maintain than alternatives at similar prices. Always get a pre-purchase inspection from an independent mechanic before buying, regardless of make or model. The inspection costs $100 to $150 and is the most effective way to avoid buying another problem vehicle.

When you arrange financing through a dealer, the dealer is legally allowed to mark up the interest rate above what you actually qualified for and keep the difference. Credit unions do not do this. A credit union gives you their rate and that is the rate you pay. Getting a loan offer from a credit union before you visit any dealership also gives you a real number to compare against whatever the dealer’s finance office shows you, which means you cannot be charged more than your credit union rate without knowing it is happening.

The cycle runs on the absence of a financial cushion between a breakdown and its consequences. Breaking it requires three things happening at the same time: building a transportation-specific emergency fund in stages ($300, then $500, then $1,000), calculating the real monthly cost of the current vehicle so the replacement math becomes clear, and researching the replacement before the current car fails so the decision is never made under pressure. The goal is to move from unpredictable repair costs to a predictable monthly cost on a vehicle with a strong reliability record, and to get there without a panic-driven purchase that starts the cycle over.

Use it as a bridge, not a destination. Make every payment. Simultaneously build credit through other means: a secured credit card used lightly and paid in full each month, a credit builder loan from a credit union. Target refinancing the loan with a traditional lender after 12 to 18 months of consistent payment history. Before refinancing, verify the vehicle meets the lender’s age and mileage requirements. Many traditional lenders will not refinance vehicles older than 10 to 12 years or over 125,000 miles. And before signing anything at the lot, ask in writing whether they report on-time payments to all three credit bureaus.

For people where real alternatives exist, yes. If public transit, carpooling, or proximity to work makes car-free living genuinely workable for a period of time, eliminating car costs for twelve months can produce $4,000 to $6,000 in savings. That is enough to buy a reliable vehicle outright, which eliminates the loan, the interest, and the dealer markup entirely. It requires a year of inconvenience. In exchange, you permanently exit the financing cycle instead of just replacing one bad loan with a slightly less bad one.