Every year, millions of people get a tax refund and feel good about it. A few hundred dollars. Sometimes a few thousand. It feels like a bonus. Like the government did something nice. It did not. Your tax refund is not free money. It is your own money, returned to you without interest, after the government held it for up to twelve months. You gave them an interest-free loan. They kept it all year. And now they are giving it back like it is a gift.

In 2025, about 104 million Americans received a tax refund. The average was $3,167. That is $3,167 that sat with the IRS instead of in your bank account, your emergency fund, or going toward a high-interest debt. You did not earn a single cent on it while it was gone. The IRS does not pay you interest for the privilege of holding your money. That is the deal, and most people never stop to think about what it actually costs them.

This article is going to pull back the curtain on exactly why this happens, who profits from it, and what you can do to stop it.

Why You Get a Refund in the First Place

When you start a job, you fill out a form called a W-4. That form tells your employer how much federal income tax to pull from every paycheck. That money goes straight to the IRS throughout the year. When you file your return in the spring, the IRS totals up what you actually owed. If more came out of your checks than you owed, you get a refund. If less came out, you owe the difference.

The refund is not a reward. It is a correction. The withholding was off. Too much left your paychecks all year, and now the math is being settled. The IRS calls this overwithholding, which just means more tax was taken from your pay than your actual bill required. This is the whole reason your tax refund is not free money. It was yours from the start. They are just giving it back.

According to the U.S. Treasury, nearly three-quarters of all taxpayers are overwithholded. That is not a coincidence. The system defaults toward taking more, not less. Most people fill out a W-4 once on their first day at a job and never touch it again. The form is set up so that doing the minimum almost always results in too much coming out. That is by design.

The Part the Industry Does Not Want You to Think About

Here is what nobody in the tax preparation business has any interest in making obvious: every dollar sitting with the IRS is a dollar not working for you.

If you got a $3,000 refund, that money was leaving your checks at roughly $250 a month. Think about what $250 a month could have done. It could have gone toward a credit card charging you 22% interest. It could have sat in a high-yield savings account earning real money. It could have covered the utility bill that went to collections in October. It could have kept you out of a payday loan in November.

Instead, the IRS had it. And they paid you nothing.

The tax preparation industry profits directly from the refund cycle. When your refund is large, people get excited. That excitement drives filing volume. It also drives a product called a Refund Anticipation Check, or RAC, where you pay a fee of $25 to $55 just to have your refund deposited into a temporary account so you can pay the tax preparer’s fee out of the refund instead of upfront. According to a 2024 Treasury Inspector General report, about 21.9 million tax returns in a single year used one of these products. Taxpayers paid an estimated $842 million in fees to receive their own money back. More than $842 million. In one year. To get a refund that only existed because they overwithholded in the first place.

Then there are Refund Anticipation Loans, or RALs, where the preparer advances you the refund before the IRS sends it. Fees run from $34 to over $130 depending on the provider, and when all the add-on charges are stacked, some taxpayers end up paying more than 10% of their refund just to access it a few days sooner. You loaned the government your money for free all year. Then you paid a company to give it back to you faster. That is the loop the industry is built on.

Some major providers like H&R Block and TurboTax now offer no-fee refund advance products, which is a real improvement. But the underlying problem is still the overwithholding that created the large refund in the first place. A no-fee advance on money that was already yours is still a worse outcome than having that money in your check every month.

There Is One Case Where a Big Refund Makes Sense

Before going further, the full picture means acknowledging this: for some people, overwithholding is deliberate, and it is not automatically wrong.

If you have historically struggled to save, a refund works like a forced savings account you cannot touch until spring. You do not earn interest on it, but you also cannot spend it. For people who would otherwise blow every dollar as it came in, the refund is the only lump sum they put together all year. That is real. Personal finance has to work in the conditions of someone’s actual life, not a spreadsheet. See Build an Emergency Fund Living Paycheck to Paycheck for how to build a real cushion without relying on your refund to do it for you.

But for most people already stretched thin, carrying high-interest debt, or dealing with bills that come faster than the money does, giving the government a free loan costs real money every month. The question to ask yourself honestly is this: if that $250 hit your account each month, would you use it well, or would it disappear? Your answer determines whether adjusting your withholding is the right move for you.

The Real Math. Not an Estimate. The Actual Numbers.

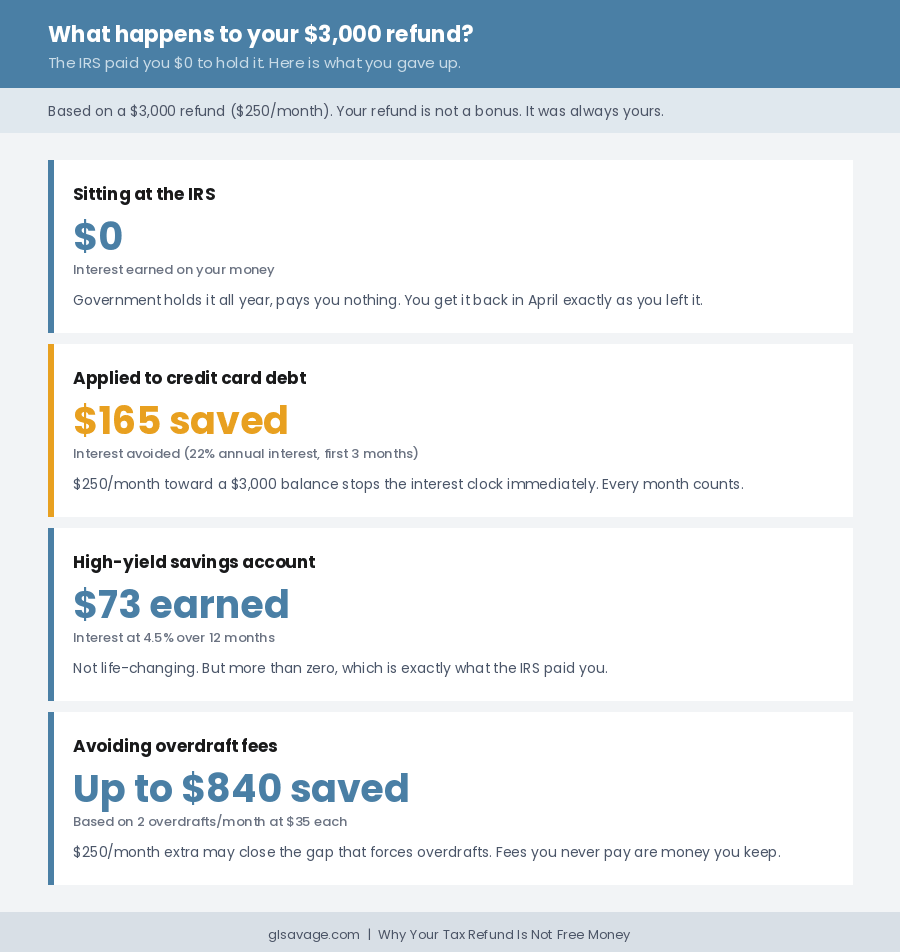

Take a $3,000 refund. That is $250 a month leaving your paycheck and sitting at the IRS.

Scenario one: you carry a $3,000 credit card balance at 22% APR, meaning 22% annual interest. If you apply that $250 a month starting in January instead of waiting for the April lump sum, you eliminate the balance in twelve months and stop the interest clock the entire time. In the first three months alone, a $3,000 balance at 22% generates roughly $165 in interest charges. That is $165 you paid a credit card company on money that the IRS was holding for free at the same time. See Minimum Payments Keep You in Debt. That Is Not an Accident. to understand exactly how that interest calculation works against you.

Scenario two: you put $250 a month into a high-yield savings account earning 4.5% annually. Over twelve months that comes to about $73 in interest. That is not a lot. But it is more than zero, which is exactly what the IRS paid you for holding the same $3,000 all year.

Scenario three: you are living paycheck to paycheck and an occasional gap between a bill’s due date and your next check forces you to overdraft. An extra $250 a month might close that gap entirely. The average overdraft fee runs around $35 per incident. Two a month is $840 a year. That is $840 in fees on money that was technically yours the whole time, sitting at the IRS. Read How Banks Make Money From Overdraft Fees and Everything Else They Are Not Telling You for the full picture on how that system is designed to trap you.

Scenario four, and the one nobody plans for: the refund does not arrive when you expect it. The IRS processes most e-filed returns within 21 days. But returns flagged for additional review, those claiming the Earned Income Tax Credit or Child Tax Credit, amended returns, and returns with errors can all take much longer. Sometimes weeks. Sometimes months. If you were counting on that April check to pay a bill, and the IRS is still reviewing your return in June, you are now in a hole you built by overpaying all year. The IRS Where’s My Refund tool exists because delays are common enough that they needed one.

How the W-4 Actually Works and Why Most People Get It Wrong

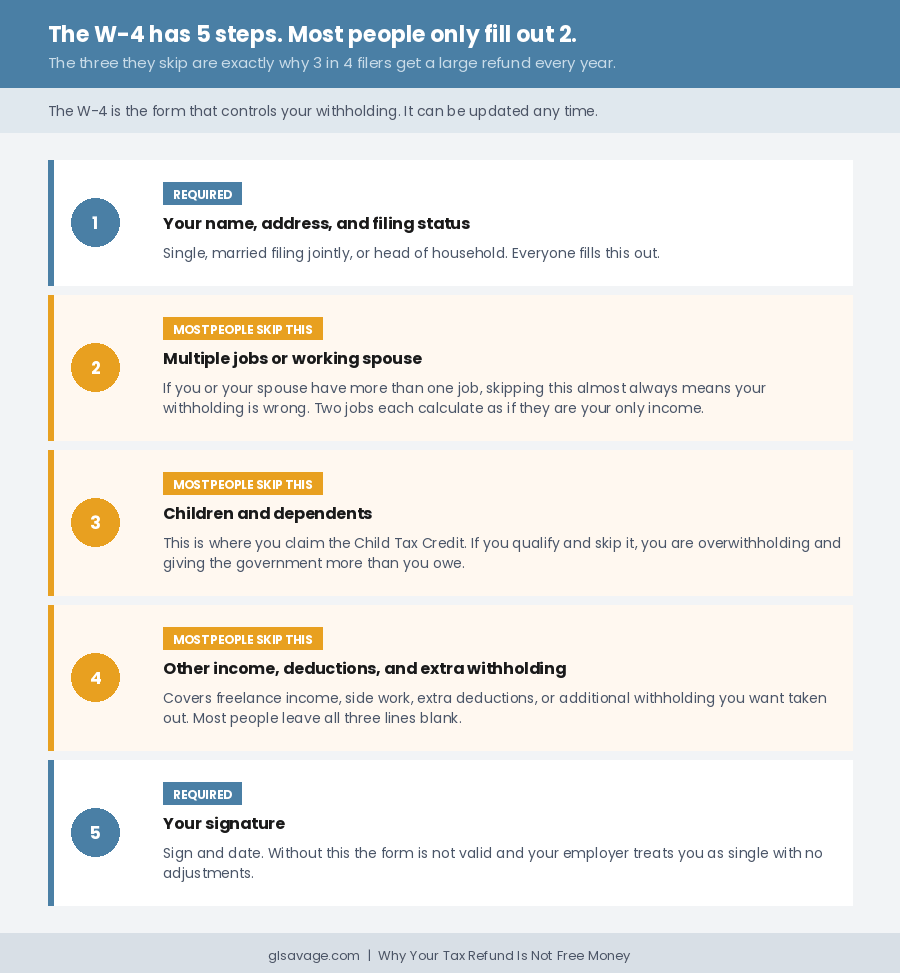

The W-4 is the form that controls all of this. It is called the Employee’s Withholding Certificate. Most people fill it out on day one of a new job, check a few boxes without really understanding them, and never look at it again. What they do not realize is that the default settings almost always produce overwithholding. That is why three-quarters of filers get a refund every year.

The current W-4 has five steps. Steps 1 and 5 are required for everyone. Steps 2 through 4 are where the precision lives, and most people skip all of them.

Step 2 applies if you have more than one job or a spouse who also works. This is where withholding breaks down for a lot of people. Two jobs mean two separate withholding calculations, each running as if it is the only income you have. The result is often either way too much taken out in total, or not nearly enough, leading to a surprise bill in April. Read Why a Second Job Often Costs More Than It Pays to see how a second income can cost you more than you think when the withholding is not handled correctly.

Step 3 is for people with children or other dependents. This is where you claim credits that reduce how much is withheld each pay period. If you qualify and skip this step, you are overwithholding without knowing it.

Step 4 lets you account for other income with no withholding attached, like freelance or gig work. It also lets you claim deductions beyond the standard or request additional withholding if you want more taken out. Most people leave all three lines blank.

The default outcome of filling out only steps 1 and 5 is almost always overwithholding. That is not a mistake in the design. That is the point. The form defaults toward protecting the IRS from underpayment, not toward keeping more money in your pocket. And that default is exactly why your tax refund is not free money for most of the people who receive one.

How to Fix It

You do not have to wait for a new year or a new job. You can start today.

Go to the IRS Tax Withholding Estimator at irs.gov. It is free. Have your most recent pay stub and last year’s tax return in front of you. The tool walks through your income, deductions, and credits, and tells you exactly whether your withholding is on track. If it is not, it tells you precisely what to change on your W-4.

Once you have the numbers, fill out a new W-4 and hand it to your employer’s HR or payroll department. You do not need permission. You do not need to explain yourself. You can do this any time during the year. The change takes effect on the next payroll cycle after it is processed.

The goal is not to owe a large amount in April. The goal is to get as close to breaking even as reasonably possible. A small refund is fine. A large refund is money that could have been in your checks all year. A large balance due means too little came out, and depending on the amount, you may owe an underpayment penalty on top of what you owe.

There is a rule that protects you from that penalty. If you withhold at least 90% of your current year’s actual tax, or 100% of what you owed last year, the penalty does not apply. For prior year adjusted gross income, meaning your total taxable income before deductions, above $150,000, the threshold is 110% of last year’s bill. You do not have to land exactly on zero. You just need to be close enough that the IRS is not charging you extra for the gap. The Withholding Estimator is built to keep you inside that range.

When Your Life Changes, Update the W-4

Your withholding should not stay frozen at whatever you set on your first day at a job. Any change that touches your taxes should trigger a W-4 review.

Getting married changes your filing status and usually your combined household income. Having a child opens up credits on the W-4. Getting divorced removes the married filing jointly status and shifts the whole picture. Taking on a second job or gig work brings in income with no withholding attached. Any of these situations left unaddressed almost certainly means your withholding is off. Read What Happens to Your Benefits When You Get a Raise for a breakdown of how an income change hits your taxes and your benefits at the same time.

Review your W-4 once a year. The right time is right after you file, when last year is fresh and you can see exactly what happened and what you would change.

What to Do If You Are Self-Employed or Have Gig Income

If you work for yourself, drive rideshare, freelance, or have any income without an employer pulling taxes out, nobody is withholding on your behalf. The W-4 does not cover that income. You are responsible for making quarterly estimated tax payments directly to the IRS, four times a year. The due dates typically fall in April, June, September, and January.

The form is IRS Form 1040-ES. The amounts are based on what you expect to owe. Skip these payments or pay too little, and you may face an underpayment penalty at filing even if you pay the full balance by April 15.

If you have both a W-2 job, meaning a regular job where taxes are withheld from your paycheck, and self-employment income, one option is to use the IRS Withholding Estimator to calculate how much extra to add to your W-4 at the regular job to cover the self-employment tax as well. This skips the quarterly payment process if you prefer to handle it through your paycheck.

The Honest Takeaway

Getting a big refund is not a sign you paid less in taxes. Owing in April is not a sign you paid more. Both are just the result of whether your withholding hit the mark or missed it. Your actual tax bill is the same either way.

Your tax refund is not free money. It never was. It is your money, held without interest, returned on the government’s schedule, not yours. If you want it back monthly instead of in a lump sum in April, the W-4 is the lever. The IRS even built the tool to tell you exactly how to pull it.

The government does not need your interest-free loan. Your high-interest debt definitely cannot afford to wait until April.

Frequently Asked Questions

Is a tax refund really not free money?

That is correct. A tax refund is your own money returned to you after your employer withheld more than your actual tax bill throughout the year. The IRS does not pay you interest for holding it. You are getting back what was always yours, minus the months it could have been working for you instead.

How do I stop getting a large tax refund every year?

Adjust your W-4 withholding. Use the free IRS Tax Withholding Estimator at irs.gov, run your numbers, then submit an updated W-4 to your employer. No waiting period. The change takes effect on the next payroll cycle after they process it.

What is overwithholding and why does it happen?

Overwithholding means more income tax came out of your paychecks than your actual tax bill required. It happens because the W-4 defaults toward taking more, not less, and most people fill it out once and never revisit it. Nearly three-quarters of U.S. taxpayers are overwithholded, according to the U.S. Treasury.

Can I change my W-4 at any time during the year?

Yes. You can submit a new W-4 to your employer’s HR or payroll department at any time. No waiting for January. No permission required. The change takes effect after your employer processes it.

What happens if I adjust my withholding too low and end up owing?

If you underwithold significantly, you may owe an underpayment penalty at filing. You avoid it by withholding at least 90% of your current year’s actual tax bill, or 100% of what you owed last year. The IRS Tax Withholding Estimator is built to keep you safely inside that range.

Is it ever smart to get a large tax refund?

For some people, intentional overwithholding is the only consistent way they save money. If that describes you, the cost is the interest you did not earn and the cash flow flexibility you did not have all year. For people carrying high-interest debt, having the money monthly almost always makes more financial sense than waiting for the lump sum.

What are refund anticipation loans and are they worth it?

A refund anticipation loan is an advance on your expected refund that a tax preparer gives you before the IRS sends the actual money. Fees run from $34 to over $130, and when all the add-on charges are included, some taxpayers pay more than 10% of their refund just to get it a few days sooner. You spent all year giving the government a free loan. Then you paid a company to return it faster. No-fee advance products from major software companies are a better deal, but the real fix is eliminating the large refund through correct withholding in the first place.

Does adjusting my W-4 change how much total tax I owe?

No. The total tax you owe is set by your income, deductions, and credits. Adjusting your W-4 only changes when you pay it: spread across your checks versus settled at filing. The bill at the end of the year is exactly the same either way.

Why might my tax refund be delayed by the IRS?

The IRS processes most e-filed returns within 21 days, but returns flagged for additional review, those claiming the Earned Income Tax Credit or Child Tax Credit, amended returns, and returns with errors or mismatched information can take much longer. Use the IRS Where’s My Refund tool at irs.gov to check status. Filing electronically and choosing direct deposit is the fastest path to getting your money once it is processed.